Canatu Oyj: Monetization Restructuring Near Vantaa Manufacturing Hub as 1000-bps Margin Expansion Signals Asset-Light Licensing Pivot

Date : 2026-05-21

Reading : 109

Despite a 29.2% pro forma top-line contraction to $17.64 million, Canatu’s 2025 financials reveal a structural 1000-bps gross margin expansion. This dynamic exposes a deliberate operational rotation from capital-intensive equipment sales to a high-margin intellectual property licensing model anchored by the proprietary Dry Deposition™ platform. Supported by $104.13 million in liquid reserves, the enterprise is absorbing temporal adoption friction to advance its parallel manufacturing capabilities in Vantaa, Finland, ahead of the 2027 high-power 600W EUV lithography inflection point—a critical node for global semiconductor foundries.

Forensic Financials & Segmental Operating Leverage

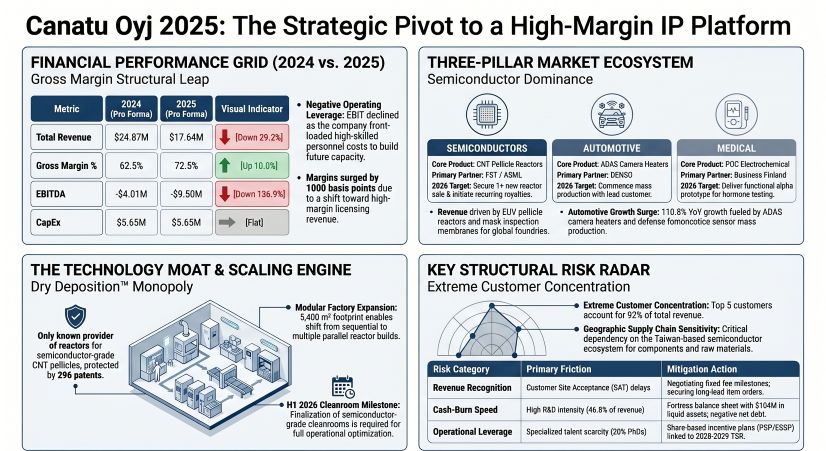

The 2025 fiscal period operated as a transitional bottleneck for Canatu Oyj. Management strategically absorbed significant operating losses to fortify human capital and infrastructure, transitioning the revenue mix toward recurring IP royalties.

Figure Canatu Oyj 2025: The Strategic Pivot to a High-Margin IP Platform

Segmental Inventory & Top-Line Contraction:

Segmental Inventory & Top-Line Contraction:

* Total Pro Forma Revenue: $17.64 million (down 29.2% YoY from $24.87 million).

* Semiconductors: $12.21 million (69.2% revenue share, contracting 45.2% YoY). The decline was driven by a temporal lack of hardware orders, as the CNT100 SEMI reactor at South Korea's Fine Semitech Corp. (FST) underwent extended Site Acceptance Testing (SAT), ultimately receiving a commercial production license in October 2025.

* Automotive: $5.43 million (30.8% revenue share, surging 110.8% YoY), propelled by deep joint development with Japan’s DENSO for ADAS camera film heaters and defense sensor mass production.

* Medical Diagnostics: $0.00 million, operating strictly in an incubation phase funded partially by an $11.31 million Business Finland grant, targeting an ultra-sensitive alpha prototype for hormone testing by 2026.

* Unit Economics & Margin Architecture: Absolute gross profit fell 17.9% to $12.78 million, yet gross margin as a percentage of revenue expanded by 1000 basis points (from 62.5% to 72.5%). This confirms a favorable unit-economic shift toward high-margin licensing rather than episodic hardware delivery.

* Operating Leverage & Capital Allocation:

* Adjusted EBIT / EBITDA: Adjusted EBIT deteriorated 110.9% to -$11.53 million (-65.3% margin). Operating loss finalized at -$12.10 million, and EBITDA dropped to -$9.50 million (-53.9% margin).

* R&D & Human Capital Friction: R&D expenditure reached $8.25 million, consuming 46.8% of total revenue. For the first time, $1.58 million of R&D payroll strictly tied to semiconductor unit development was capitalized. Average FTE headcount expanded 17.9% (from 123 to 145), driving a 22.5% increase in personnel expenses to $15.38 million.

* Liquidity & FCF Conversion: Despite the massive EBIT deterioration, cash flow from operations (CFO) was highly resilient at just -$1.24 million. The enterprise boasts a fortress balance sheet: $133.30 million in total assets, $122.10 million in equity (93.2% ratio), and a net debt profile of -$101.64 million. Total liquid reserves stand at $104.13 million ($24.99 million in cash, $79.14 million in low-risk money market funds). CapEx remained flat at $5.65 million.

Supply Chain Audit & Geo-Economic Moat

Canatu operates an increasingly localized core footprint with highly vulnerable external integration nodes, presenting an asymmetric geographic risk matrix.

* Physicality & Internal Scaling: The primary node of value creation is the Vantaa, Finland global headquarters. In 2025, Canatu expanded its physical production space here to 5,400 m², actively shifting from sequential to "parallel reactor builds." However, structural finalization relies on H1/2026 CapEx deployments, specifically an advanced cleanroom build-out and the delayed delivery of a specialized PELMIS EUV inspection system.

* Geo-Economic Dependency (Taiwan, Province of China): The company’s systemic geographic vulnerability lies in its reliance on the global semiconductor supply chain, heavily concentrated in Taiwan, Province of China. This localized chokepoint exposes Canatu to severe geopolitical and macroeconomic disruptions regarding key raw materials and terminal chip manufacturing demand.

* Third-Party Execution Bottlenecks: Canatu’s commercial scale-up is heavily throttled by external ecosystem dependencies. Client concentration is extreme, with the single largest customer comprising 40% of revenue, and the top five dominating 92%. Furthermore, the adoption of the company's carbon nanotube (CNT) pellicles hinges on two uncontrollable variables: mandatory safety and performance certification by ASML, and the ability of end-customers to successfully apply proprietary coatings to prevent hydrogen plasma etching.

HDIN Institutional Perspective

While retail sentiment may fixate on the 29.2% top-line contraction and the Board's withdrawal of its 2027 financial targets, institutional capital should interpret 2025 as a successful strategic de-risking phase. Management traded short-term P&L optics for structural asset-light viability. The divergence between the -$12.10 million operating loss and the mere -$1.24 million CFO cash burn indicates that the operational friction is predominantly forward-looking investment rather than structural hemorrhaging. By successfully shifting the monetization model toward licensing (validated by the October FST commercial license), Canatu is uniquely positioning its 296-patent IP portfolio to capture disproportionate value when the semiconductor industry hits the structural thermal limits of 500W+ EUV lithography, expected ahead of 2027.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Forensic Financials & Segmental Operating Leverage

The 2025 fiscal period operated as a transitional bottleneck for Canatu Oyj. Management strategically absorbed significant operating losses to fortify human capital and infrastructure, transitioning the revenue mix toward recurring IP royalties.

Figure Canatu Oyj 2025: The Strategic Pivot to a High-Margin IP Platform

Segmental Inventory & Top-Line Contraction: * Total Pro Forma Revenue: $17.64 million (down 29.2% YoY from $24.87 million).

* Semiconductors: $12.21 million (69.2% revenue share, contracting 45.2% YoY). The decline was driven by a temporal lack of hardware orders, as the CNT100 SEMI reactor at South Korea's Fine Semitech Corp. (FST) underwent extended Site Acceptance Testing (SAT), ultimately receiving a commercial production license in October 2025.

* Automotive: $5.43 million (30.8% revenue share, surging 110.8% YoY), propelled by deep joint development with Japan’s DENSO for ADAS camera film heaters and defense sensor mass production.

* Medical Diagnostics: $0.00 million, operating strictly in an incubation phase funded partially by an $11.31 million Business Finland grant, targeting an ultra-sensitive alpha prototype for hormone testing by 2026.

* Unit Economics & Margin Architecture: Absolute gross profit fell 17.9% to $12.78 million, yet gross margin as a percentage of revenue expanded by 1000 basis points (from 62.5% to 72.5%). This confirms a favorable unit-economic shift toward high-margin licensing rather than episodic hardware delivery.

* Operating Leverage & Capital Allocation:

* Adjusted EBIT / EBITDA: Adjusted EBIT deteriorated 110.9% to -$11.53 million (-65.3% margin). Operating loss finalized at -$12.10 million, and EBITDA dropped to -$9.50 million (-53.9% margin).

* R&D & Human Capital Friction: R&D expenditure reached $8.25 million, consuming 46.8% of total revenue. For the first time, $1.58 million of R&D payroll strictly tied to semiconductor unit development was capitalized. Average FTE headcount expanded 17.9% (from 123 to 145), driving a 22.5% increase in personnel expenses to $15.38 million.

* Liquidity & FCF Conversion: Despite the massive EBIT deterioration, cash flow from operations (CFO) was highly resilient at just -$1.24 million. The enterprise boasts a fortress balance sheet: $133.30 million in total assets, $122.10 million in equity (93.2% ratio), and a net debt profile of -$101.64 million. Total liquid reserves stand at $104.13 million ($24.99 million in cash, $79.14 million in low-risk money market funds). CapEx remained flat at $5.65 million.

Supply Chain Audit & Geo-Economic Moat

Canatu operates an increasingly localized core footprint with highly vulnerable external integration nodes, presenting an asymmetric geographic risk matrix.

* Physicality & Internal Scaling: The primary node of value creation is the Vantaa, Finland global headquarters. In 2025, Canatu expanded its physical production space here to 5,400 m², actively shifting from sequential to "parallel reactor builds." However, structural finalization relies on H1/2026 CapEx deployments, specifically an advanced cleanroom build-out and the delayed delivery of a specialized PELMIS EUV inspection system.

* Geo-Economic Dependency (Taiwan, Province of China): The company’s systemic geographic vulnerability lies in its reliance on the global semiconductor supply chain, heavily concentrated in Taiwan, Province of China. This localized chokepoint exposes Canatu to severe geopolitical and macroeconomic disruptions regarding key raw materials and terminal chip manufacturing demand.

* Third-Party Execution Bottlenecks: Canatu’s commercial scale-up is heavily throttled by external ecosystem dependencies. Client concentration is extreme, with the single largest customer comprising 40% of revenue, and the top five dominating 92%. Furthermore, the adoption of the company's carbon nanotube (CNT) pellicles hinges on two uncontrollable variables: mandatory safety and performance certification by ASML, and the ability of end-customers to successfully apply proprietary coatings to prevent hydrogen plasma etching.

HDIN Institutional Perspective

While retail sentiment may fixate on the 29.2% top-line contraction and the Board's withdrawal of its 2027 financial targets, institutional capital should interpret 2025 as a successful strategic de-risking phase. Management traded short-term P&L optics for structural asset-light viability. The divergence between the -$12.10 million operating loss and the mere -$1.24 million CFO cash burn indicates that the operational friction is predominantly forward-looking investment rather than structural hemorrhaging. By successfully shifting the monetization model toward licensing (validated by the October FST commercial license), Canatu is uniquely positioning its 296-patent IP portfolio to capture disproportionate value when the semiconductor industry hits the structural thermal limits of 500W+ EUV lithography, expected ahead of 2027.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."