Global Fuel Cell 2026 Outlook: Why Bloom Energy, Plug Power, and Sino-Synergy Diverge on Capital Allocation Amid AI Infrastructure Demands

Date : 2026-05-21

Reading : 191

The 2025 global fuel cell reporting cycle reveals a brutal bifurcation. While legacy conglomerates leverage industrial cash flows to fund zero-emission transitions, pure-play hydrogen manufacturers face severe working capital destruction driven by delayed subsidies and crushing accounts receivable bloat. Institutional LPs must pivot: the era of speculative mobility commercialization faces severe headwinds. The immediate alpha resides in Solid Oxide Fuel Cells (SOFC) provisioning off-grid baseload power for AI data centers, effectively insulating operators from macroeconomic volatility and municipal grid constraints.

Profitability Quality and Sector-Wide Capital Bleed

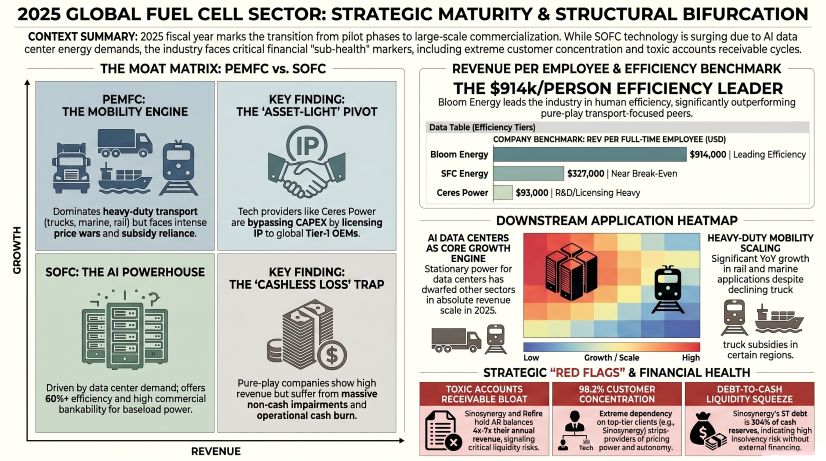

The transition from R&D to commercialization has triggered extreme operating leverage disparities across the sector. A forensic audit of the 2025 filings exposes a divide between companies exhibiting self-sustaining free cash flow (FCF) conversion and those trapped in impairment-driven liquidity crises.

Figure 2025 GLOBAL FUEL CELL SECTOR: STRATEGIC MATURITY & STRUCTURAL BIFURCATION

Unit Economics and Segmental Inventory Breakdown:

Unit Economics and Segmental Inventory Breakdown:

1. Self-Sustaining Conglomerates & Niche Monopolies:

* Weichai Power (HKG: 2338): Generated a net profit of $1,520.8M on $32,251.7M total revenue. Crucially, FCF stands at a massive $3,044.87M. Its strategic 51/49 joint venture with NASDAQ: BLDP (Ballard Power Systems) delivered a 260kW powertrain, targeting a 20% share of China’s heavy-duty hydrogen corridor.

* SFC Energy (FRA: F3C): Posted $161.35M in revenue with a sector-leading 40.8% gross margin ($66.0M gross profit), minimizing its net loss to just $1.0M. Generating 54% of its revenue in Europe, it secured high-margin defense contracts including $1.7M from NATO and $3.62M from the Indian Ministry of Defence.

2. The AI Data Center Beneficiaries (SOFC):

* Bloom Energy (NYSE: BE): Dominated the stationary power segment with $2,023.99M in revenue ($1,639.43M from the US). Despite a net loss of $187.9M, Bloom achieved a 29% gross margin. The company is actively exploiting the AI power bottleneck, underscored by a $5.0B financing framework with Brookfield and a 1 GW off-take agreement with AEP, driving Q1 2026 revenue guidance up 130%.

* Ceres Power (LSE: CWR): Operating an asset-light IP licensing model, it recognized $43.06M in revenue (85% from Asia) and $30.0M in gross profit. Capital allocation is highly efficient, leveraging partner CAPEX—such as Delta Electronics' $224.26M SOFC factory and Doosan's $1.09B 50MW plant.

3. The "Cashless Loss" & Sub-Health Cohort:

* Plug Power (NASDAQ: PLUG): Despite recognizing $709.92M in revenue (including 184 units of 1MW electrolyzers generating $187M), the company suffered a $242.0M gross loss (-34.1% margin) and a catastrophic $1,631.6M net loss. Severe inventory devaluation drove a $785.4M impairment charge.

* FuelCell Energy (NASDAQ: FCEL): Logged $158.16M in revenue against a $191.37M net loss. Customer concentration is a critical risk, with its top three utility clients accounting for 68% of total revenue.

* Sino-Synergy (HKG: 9663) & REFIRE Group (HKG: 2570): Both face toxic asset accumulation. Sino-Synergy’s revenue fell to $41.72M while gross accounts receivable (AR) bloated to $305.04M (7x revenue), forcing $91.94M in expected credit losses (ECL). System ASPs collapsed from $611.08/kW to $388.14/kW. REFIRE similarly reported $82.81M in revenue against $395.65M in AR (4.8x revenue), with short-term debt of $149.04M dwarfing its $69.29M cash reserves.

Geopolitical Supply Chain Audit and Manufacturing Bottlenecks

The physicality of the global hydrogen economy remains highly fragile, constrained by critical raw materials and geographically concentrated assembly hubs.

* Precious Metal Dependencies & Hedging: The scarcity of Platinum Group Metals (PGMs) dictates gross margin volatility for PEM manufacturers. FRA: F3C internal modeling indicates that a 5% fluctuation in platinum prices swings annual OPEX by $163,937. To insulate against this, Cummins (NYSE: CMI) executed a $65.0M physical forward contract to hedge platinum and palladium procurement for its Accelera division.

* Physical Infrastructure & Geographic Footprints: To bypass cross-border tariffs and secure intellectual property, firms are aggressively localizing component manufacturing. FRA: F3C acquired its MEA supplier to bring production in-house at its Swindon facility in the UK. Conversely, NASDAQ: PLUG continues scaling its Rochester, New York Gigafactory but reported liquid hydrogen force majeure events that severely delayed downstream deployments. In the carbon capture space, NASDAQ: FCEL advanced its Generation 2 Technology via pilot testing at the ExxonMobil Rotterdam site and the Idaho National Laboratory (INL).

* Geopolitical Tariffs & IP Transfers: US and EU tariffs targeting Chinese components restrict the cross-border flow of fuel cell stacks. To circumvent this, PowerCell Sweden (STO: PCELL) transferred IP for its S3 stack to Robert Bosch GmbH for localized Chinese market industrialization. In China, Vision Group (SZSE: 002733) abruptly shifted $41.74M in raised capital from its Shenzhen Hydrogen Industrial Park into traditional lithium battery bases, citing immature infrastructure. Furthermore, REFIRE operates a multi-technology (ALK/PEM/AEM) test base at the Ningxia Wuzhong Taiyangshan facility, attempting to localize the electrolyzer supply chain.

HDIN Institutional Perspective

While retail consensus treats fuel cell pure-plays as a monolithic, policy-backed green energy trade, our forensic audit dictates a highly differentiated viewpoint. We challenge the viability of pure-play hydrogen mobility startups (such as HKG: 2402 SinoHytec and HKG: 9663 Sino-Synergy). Their extreme customer concentration (>77% for top 5 clients) and staggering AR-to-revenue ratios expose a fundamental inability to collect cash, signaling a commercial model that is structurally subordinate to state-owned enterprise payment cycles.

Conversely, the Street is structurally underpricing the margin expansion potential within the SOFC stationary power sector. AI data centers require 99.999% uptime, completely bypassing the localized hydrogen refueling bottleneck by utilizing natural gas/biogas pipelines. Companies like NYSE: BE and LSE: CWR that have pivoted away from speculative heavy-duty mobility toward supplying off-grid baseload power for tech hyperscalers possess the only genuinely bankable unit economics in the 2026 landscape.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Profitability Quality and Sector-Wide Capital Bleed

The transition from R&D to commercialization has triggered extreme operating leverage disparities across the sector. A forensic audit of the 2025 filings exposes a divide between companies exhibiting self-sustaining free cash flow (FCF) conversion and those trapped in impairment-driven liquidity crises.

Figure 2025 GLOBAL FUEL CELL SECTOR: STRATEGIC MATURITY & STRUCTURAL BIFURCATION

Unit Economics and Segmental Inventory Breakdown:1. Self-Sustaining Conglomerates & Niche Monopolies:

* Weichai Power (HKG: 2338): Generated a net profit of $1,520.8M on $32,251.7M total revenue. Crucially, FCF stands at a massive $3,044.87M. Its strategic 51/49 joint venture with NASDAQ: BLDP (Ballard Power Systems) delivered a 260kW powertrain, targeting a 20% share of China’s heavy-duty hydrogen corridor.

* SFC Energy (FRA: F3C): Posted $161.35M in revenue with a sector-leading 40.8% gross margin ($66.0M gross profit), minimizing its net loss to just $1.0M. Generating 54% of its revenue in Europe, it secured high-margin defense contracts including $1.7M from NATO and $3.62M from the Indian Ministry of Defence.

2. The AI Data Center Beneficiaries (SOFC):

* Bloom Energy (NYSE: BE): Dominated the stationary power segment with $2,023.99M in revenue ($1,639.43M from the US). Despite a net loss of $187.9M, Bloom achieved a 29% gross margin. The company is actively exploiting the AI power bottleneck, underscored by a $5.0B financing framework with Brookfield and a 1 GW off-take agreement with AEP, driving Q1 2026 revenue guidance up 130%.

* Ceres Power (LSE: CWR): Operating an asset-light IP licensing model, it recognized $43.06M in revenue (85% from Asia) and $30.0M in gross profit. Capital allocation is highly efficient, leveraging partner CAPEX—such as Delta Electronics' $224.26M SOFC factory and Doosan's $1.09B 50MW plant.

3. The "Cashless Loss" & Sub-Health Cohort:

* Plug Power (NASDAQ: PLUG): Despite recognizing $709.92M in revenue (including 184 units of 1MW electrolyzers generating $187M), the company suffered a $242.0M gross loss (-34.1% margin) and a catastrophic $1,631.6M net loss. Severe inventory devaluation drove a $785.4M impairment charge.

* FuelCell Energy (NASDAQ: FCEL): Logged $158.16M in revenue against a $191.37M net loss. Customer concentration is a critical risk, with its top three utility clients accounting for 68% of total revenue.

* Sino-Synergy (HKG: 9663) & REFIRE Group (HKG: 2570): Both face toxic asset accumulation. Sino-Synergy’s revenue fell to $41.72M while gross accounts receivable (AR) bloated to $305.04M (7x revenue), forcing $91.94M in expected credit losses (ECL). System ASPs collapsed from $611.08/kW to $388.14/kW. REFIRE similarly reported $82.81M in revenue against $395.65M in AR (4.8x revenue), with short-term debt of $149.04M dwarfing its $69.29M cash reserves.

Geopolitical Supply Chain Audit and Manufacturing Bottlenecks

The physicality of the global hydrogen economy remains highly fragile, constrained by critical raw materials and geographically concentrated assembly hubs.

* Precious Metal Dependencies & Hedging: The scarcity of Platinum Group Metals (PGMs) dictates gross margin volatility for PEM manufacturers. FRA: F3C internal modeling indicates that a 5% fluctuation in platinum prices swings annual OPEX by $163,937. To insulate against this, Cummins (NYSE: CMI) executed a $65.0M physical forward contract to hedge platinum and palladium procurement for its Accelera division.

* Physical Infrastructure & Geographic Footprints: To bypass cross-border tariffs and secure intellectual property, firms are aggressively localizing component manufacturing. FRA: F3C acquired its MEA supplier to bring production in-house at its Swindon facility in the UK. Conversely, NASDAQ: PLUG continues scaling its Rochester, New York Gigafactory but reported liquid hydrogen force majeure events that severely delayed downstream deployments. In the carbon capture space, NASDAQ: FCEL advanced its Generation 2 Technology via pilot testing at the ExxonMobil Rotterdam site and the Idaho National Laboratory (INL).

* Geopolitical Tariffs & IP Transfers: US and EU tariffs targeting Chinese components restrict the cross-border flow of fuel cell stacks. To circumvent this, PowerCell Sweden (STO: PCELL) transferred IP for its S3 stack to Robert Bosch GmbH for localized Chinese market industrialization. In China, Vision Group (SZSE: 002733) abruptly shifted $41.74M in raised capital from its Shenzhen Hydrogen Industrial Park into traditional lithium battery bases, citing immature infrastructure. Furthermore, REFIRE operates a multi-technology (ALK/PEM/AEM) test base at the Ningxia Wuzhong Taiyangshan facility, attempting to localize the electrolyzer supply chain.

HDIN Institutional Perspective

While retail consensus treats fuel cell pure-plays as a monolithic, policy-backed green energy trade, our forensic audit dictates a highly differentiated viewpoint. We challenge the viability of pure-play hydrogen mobility startups (such as HKG: 2402 SinoHytec and HKG: 9663 Sino-Synergy). Their extreme customer concentration (>77% for top 5 clients) and staggering AR-to-revenue ratios expose a fundamental inability to collect cash, signaling a commercial model that is structurally subordinate to state-owned enterprise payment cycles.

Conversely, the Street is structurally underpricing the margin expansion potential within the SOFC stationary power sector. AI data centers require 99.999% uptime, completely bypassing the localized hydrogen refueling bottleneck by utilizing natural gas/biogas pipelines. Companies like NYSE: BE and LSE: CWR that have pivoted away from speculative heavy-duty mobility toward supplying off-grid baseload power for tech hyperscalers possess the only genuinely bankable unit economics in the 2026 landscape.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."