Evopoint Biosciences: Out-Licensing Pivot Near Suzhou Hub as Astellas Agreement Signals Organic Profitability Breakout

Date : 2026-05-21

Reading : 118

The $130 million global out-licensing of XNW27011 to Astellas (TYO: 4503) transforms Evopoint Biosciences’ financial architecture, effectively absorbing intensifying clinical burn rates. By converting clinical milestones into a $28.18 million net profit in 2025, Evopoint systematically neutralizes its escalating $95.21 million gross operating cash outflow. For institutional LPs, this validates a highly disciplined "innovation-feeding-research" framework. Evopoint’s ability to secure a non-dilutive $117 million net cash injection prior to domestic commercialization bypasses macro funding volatility, firmly establishing a capital moat ahead of its scheduled 2026 transition to an integrated biopharmaceutical model targeting Tier-3 hospitals.

Segmental Financials, Clinical Leverage, and Capital Allocation

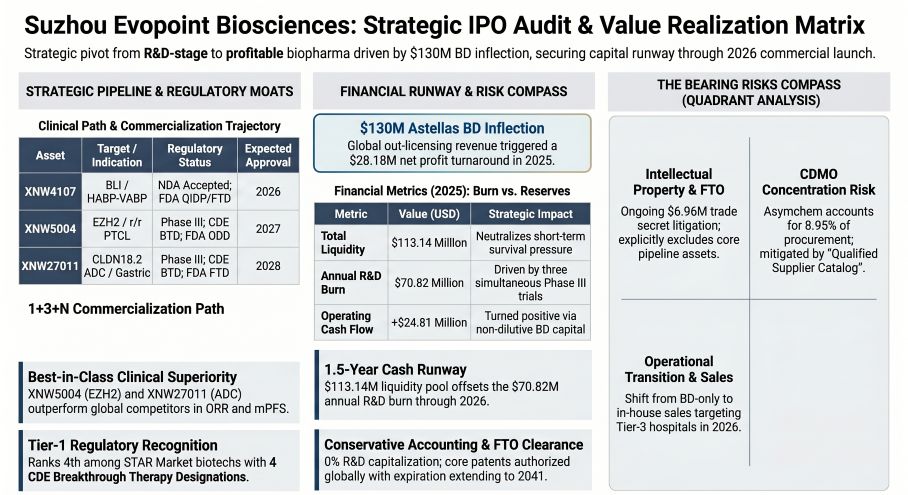

Evopoint’s financial trajectory is characterized by aggressive late-stage R&D expansion offset by highly lucrative out-licensing (BD) revenues. The company maintains a 0% R&D capitalization rate, ensuring a conservative accounting profile.

Figure Suzhou Evopoint Biosciences: Strategic IPO Audit & Value Realization Matrix

I. Segmental P&L and Cash Flow Inventory

I. Segmental P&L and Cash Flow Inventory

* Operating Revenue: Reached $130.12 million in 2025. This is overwhelmingly driven by BD out-licensing ($129.00 million, 99.14%), with minor contributions from material sales ($1.12 million, 0.86%).

* Net Profit/Loss Reversal: 2025 net profit surged to $28.18 million, erasing a history of net losses: -$59.39 million (2023) and -$53.70 million (2024), against an accumulated deficit of $201.64 million. Total assets concurrently surged 60.14% year-over-year from $151.41 million to $242.47 million.

* R&D Burn Rate: Total three-year R&D expenditure hit $175.86 million ($51.15 million in 2023; $53.89 million in 2024; $70.82 million in 2025, a +31.4% YoY increase). Management expenses spiked to $29.68 million in 2025 (up from $11.32 million in 2023 and $10.17 million in 2024), driven largely by a one-time $19.38 million share-based payment.

* Cash Flow & Liquidity Runway: Net operating cash flow flipped from -$51.56 million (2023) and -$48.62 million (2024) to +$24.81 million in 2025. Gross operating cash outflows expanded from $57.99 million to $55.48 million, settling at a new baseline of $95.21 million in 2025. Liquid assets sit at $113.14 million ($105.16 million cash + $7.98 million trading assets), providing a 14.2 to 19.5-month runway based on historical burn averages ($69.56 million to $95.21 million).

* Non-Recurring Subsidies: Government subsidies recognized in P&L were $1.19 million, $3.41 million, and $0.55 million across the three-year period, contributing a negligible 2.0%, 6.3%, and 1.9% to the baseline P&L. Deferred income remained flat at $0.33 million, $0.46 million, and $0.41 million.

II. The $2 Billion+ BD Monetization Matrix

* Astellas Pharma (XNW27011): $1.536 billion total value. $130 million non-refundable upfront ($117 million net of 10% withholding tax), $1.406 billion in milestones ($25 million expected in 2026), plus $20 million post-technology transfer.

* Everest Medicines (XNW1011): $561 million total value. $12 million upfront ($8 million net to Evopoint), with $549 million in milestones.

* SinoMab BioScience (XNW1011): $19.56 million total value. $5.59 million upfront, $13.97 million milestones.

* Hepagene Therapeutics (XNW23): $22 million total value. $2 million upfront, $1 million milestone received, $20 million remaining.

III. Core Pipeline Efficacy & Trial Unit Economics

Evopoint deploys a "1+3+N" strategy. Clinical metrics showcase significant best-in-class potential:

* XNW4107 (NDA 2025, Launch 2026): 3.0% all-cause mortality vs. 2.7% for standard-of-care (IMI/REL). Zero drug-related SAEs/deaths.

* XNW5004 (Phase II/III, NDA 2026, Launch 2027): 70.3% ORR and 15.74m mPFS in r/r PTCL. 63.2% ORR and 10.8m mPFS in r/r FL. Safety window reveals 60.0% $\ge$ Grade 3 TEAE and 53.3% $\ge$ Grade 3 TRAE.

* XNW27011 (Phase III, NDA 2027, Launch 2028): 65.2% ORR and 5.7m mPFS in G/GEJA (at 3.0mg/kg), highly effective in low-expression patients (IHC $\ge$ 2+, $\ge$ 20%). TRAE stands at 54.5%. Note: Trial reported 2 fatal SAEs (3.0 mg/kg and 4.8 mg/kg cohorts) in early stages, with 1 fatal SAE in XNW28012; all cleared by CDE for Phase III progression with zero patient disputes.

IV. Strategic $409 Million IPO Capital Allocation

The proposed IPO aims to raise $409 million, explicitly rejecting infrastructure expansion (0% allocated to headquarters). Funds are divided into liquidity ($83 million, 20.41%) and R&D ($326 million, 79.59%). The $327 million aggregate R&D budget is temporally dispersed across 2026 ($73.08 million), 2027 ($53.87 million), 2028 ($86.81 million), 2029 ($72.23 million), and 2030 ($41.41 million). Specific asset allocations: XNW27011 ($86.41 million), XNW28012 ($79.22 million), XNW5004 ($60.70 million), XNW29016 ($30.96 million), XNW34017 ($28.88 million), XNW26018 ($22.53 million), XNW42 ($17.20 million), and XNW4107 ($1.51 million).

CDMO Transitioning and the Suzhou Manufacturing Nexus

Evopoint’s physical operations display strategic agility, minimizing single-point failure risks while establishing a highly localized manufacturing hub. The company's internal headcount (362 employees, 86.19% R&D, >150 clinical staff) is heavily insulated by outsourced production agility.

* Manufacturing Infrastructure: The company has constructed a proprietary Phase I small-molecule facility in Suzhou, possessing a Type A Drug Production License. It handles a commercial capacity of 3 million sterile powder vials annually, perfectly scaled for the 2026 domestic launch of XNW4107.

* Tier-1 CDMO & CRO Network: Supplier concentration is low, peaking at 40.98% in 2023 due to a $10.37 million infrastructure contract with Jiangsu Jianyuan Construction Co., Ltd., before normalizing to 18.56% ($7.85 million) in 2024 and 25.07% ($12.50 million) in 2025.

* Supply Chain Fluidity: Evopoint executed a flawless technology transfer for its ADC assets (XNW27011, XNW28012). Early payload-linker development was sourced from Suzhou MediLink ($2.57 million, 5.06% in 2023; $1.39 million IP fee), before migrating late-stage/NDA production to Asymchem (SZE: 002821), the top 2025 supplier at $4.46 million (8.95%). Other key CROs include WuXi AppTec (SHA: 603259) at $1.98 million (3.90% in 2023) and Fortrea ($1.13 million, $1.56 million, and $1.62 million across the period).

* Unit Economics of Materials: The 2025 raw material spend totaled $9.51 million (API/excipients $4.18 million; clinical drugs $2.80 million; commercial drugs $0.79 million; reagents $1.75 million). 2025 clinical trial service fees equaled $15.69 million.

HDIN Institutional Perspective

While the prospectus aggressively markets Evopoint's "1+3+N" strategy as a seamless transition from biotech to an integrated biopharma entity, forensic equity analysis reveals latent execution friction unpriced by the Street. The firm holds an impenetrable IP moat (composition patents valid through 2039/2041) and faces zero material impact from an ongoing $6.96 million trade secret suit filed by Hangzhou Xin Yuansu. However, its voting structure is intensely concentrated: Actual controller Qiang Jing controls 47.0448% of voting rights (Direct 0.8218%, Lipan 21.5802%, Youyao 10.0154%, Xinkang 4.4875%, Chenghuai 0.3927%, Youxiao 0.1122%, plus 9.6350% via CEO Le Meijie).

This centralized governance minimizes activist interference but amplifies key-man risk during the critical 2026-2028 commercial rollout. Despite this, the institutional capitalization table acts as a formidable buffer. Top-tier LPs, including Tencent (5.7615%), Loyal Valley Capital (12.9965%), CICC (1.0975%), CDH (1.0274%), and Kailaiying (2.2885%), are locked in for 12 to 36 months post-IPO. We argue that Evopoint's deliberate avoidance of heavy CapEx expansion—eschewing massive biologic facility builds in favor of CDMO partnerships—represents apex capital efficiency. The firm is economically insulated; even if XNW4107's 2026 Tier-3 hospital commercial launch underperforms, the guaranteed waterfall of Astellas milestones ensures operational solvency through the end of the decade.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Segmental Financials, Clinical Leverage, and Capital Allocation

Evopoint’s financial trajectory is characterized by aggressive late-stage R&D expansion offset by highly lucrative out-licensing (BD) revenues. The company maintains a 0% R&D capitalization rate, ensuring a conservative accounting profile.

Figure Suzhou Evopoint Biosciences: Strategic IPO Audit & Value Realization Matrix

I. Segmental P&L and Cash Flow Inventory* Operating Revenue: Reached $130.12 million in 2025. This is overwhelmingly driven by BD out-licensing ($129.00 million, 99.14%), with minor contributions from material sales ($1.12 million, 0.86%).

* Net Profit/Loss Reversal: 2025 net profit surged to $28.18 million, erasing a history of net losses: -$59.39 million (2023) and -$53.70 million (2024), against an accumulated deficit of $201.64 million. Total assets concurrently surged 60.14% year-over-year from $151.41 million to $242.47 million.

* R&D Burn Rate: Total three-year R&D expenditure hit $175.86 million ($51.15 million in 2023; $53.89 million in 2024; $70.82 million in 2025, a +31.4% YoY increase). Management expenses spiked to $29.68 million in 2025 (up from $11.32 million in 2023 and $10.17 million in 2024), driven largely by a one-time $19.38 million share-based payment.

* Cash Flow & Liquidity Runway: Net operating cash flow flipped from -$51.56 million (2023) and -$48.62 million (2024) to +$24.81 million in 2025. Gross operating cash outflows expanded from $57.99 million to $55.48 million, settling at a new baseline of $95.21 million in 2025. Liquid assets sit at $113.14 million ($105.16 million cash + $7.98 million trading assets), providing a 14.2 to 19.5-month runway based on historical burn averages ($69.56 million to $95.21 million).

* Non-Recurring Subsidies: Government subsidies recognized in P&L were $1.19 million, $3.41 million, and $0.55 million across the three-year period, contributing a negligible 2.0%, 6.3%, and 1.9% to the baseline P&L. Deferred income remained flat at $0.33 million, $0.46 million, and $0.41 million.

II. The $2 Billion+ BD Monetization Matrix

* Astellas Pharma (XNW27011): $1.536 billion total value. $130 million non-refundable upfront ($117 million net of 10% withholding tax), $1.406 billion in milestones ($25 million expected in 2026), plus $20 million post-technology transfer.

* Everest Medicines (XNW1011): $561 million total value. $12 million upfront ($8 million net to Evopoint), with $549 million in milestones.

* SinoMab BioScience (XNW1011): $19.56 million total value. $5.59 million upfront, $13.97 million milestones.

* Hepagene Therapeutics (XNW23): $22 million total value. $2 million upfront, $1 million milestone received, $20 million remaining.

III. Core Pipeline Efficacy & Trial Unit Economics

Evopoint deploys a "1+3+N" strategy. Clinical metrics showcase significant best-in-class potential:

* XNW4107 (NDA 2025, Launch 2026): 3.0% all-cause mortality vs. 2.7% for standard-of-care (IMI/REL). Zero drug-related SAEs/deaths.

* XNW5004 (Phase II/III, NDA 2026, Launch 2027): 70.3% ORR and 15.74m mPFS in r/r PTCL. 63.2% ORR and 10.8m mPFS in r/r FL. Safety window reveals 60.0% $\ge$ Grade 3 TEAE and 53.3% $\ge$ Grade 3 TRAE.

* XNW27011 (Phase III, NDA 2027, Launch 2028): 65.2% ORR and 5.7m mPFS in G/GEJA (at 3.0mg/kg), highly effective in low-expression patients (IHC $\ge$ 2+, $\ge$ 20%). TRAE stands at 54.5%. Note: Trial reported 2 fatal SAEs (3.0 mg/kg and 4.8 mg/kg cohorts) in early stages, with 1 fatal SAE in XNW28012; all cleared by CDE for Phase III progression with zero patient disputes.

IV. Strategic $409 Million IPO Capital Allocation

The proposed IPO aims to raise $409 million, explicitly rejecting infrastructure expansion (0% allocated to headquarters). Funds are divided into liquidity ($83 million, 20.41%) and R&D ($326 million, 79.59%). The $327 million aggregate R&D budget is temporally dispersed across 2026 ($73.08 million), 2027 ($53.87 million), 2028 ($86.81 million), 2029 ($72.23 million), and 2030 ($41.41 million). Specific asset allocations: XNW27011 ($86.41 million), XNW28012 ($79.22 million), XNW5004 ($60.70 million), XNW29016 ($30.96 million), XNW34017 ($28.88 million), XNW26018 ($22.53 million), XNW42 ($17.20 million), and XNW4107 ($1.51 million).

CDMO Transitioning and the Suzhou Manufacturing Nexus

Evopoint’s physical operations display strategic agility, minimizing single-point failure risks while establishing a highly localized manufacturing hub. The company's internal headcount (362 employees, 86.19% R&D, >150 clinical staff) is heavily insulated by outsourced production agility.

* Manufacturing Infrastructure: The company has constructed a proprietary Phase I small-molecule facility in Suzhou, possessing a Type A Drug Production License. It handles a commercial capacity of 3 million sterile powder vials annually, perfectly scaled for the 2026 domestic launch of XNW4107.

* Tier-1 CDMO & CRO Network: Supplier concentration is low, peaking at 40.98% in 2023 due to a $10.37 million infrastructure contract with Jiangsu Jianyuan Construction Co., Ltd., before normalizing to 18.56% ($7.85 million) in 2024 and 25.07% ($12.50 million) in 2025.

* Supply Chain Fluidity: Evopoint executed a flawless technology transfer for its ADC assets (XNW27011, XNW28012). Early payload-linker development was sourced from Suzhou MediLink ($2.57 million, 5.06% in 2023; $1.39 million IP fee), before migrating late-stage/NDA production to Asymchem (SZE: 002821), the top 2025 supplier at $4.46 million (8.95%). Other key CROs include WuXi AppTec (SHA: 603259) at $1.98 million (3.90% in 2023) and Fortrea ($1.13 million, $1.56 million, and $1.62 million across the period).

* Unit Economics of Materials: The 2025 raw material spend totaled $9.51 million (API/excipients $4.18 million; clinical drugs $2.80 million; commercial drugs $0.79 million; reagents $1.75 million). 2025 clinical trial service fees equaled $15.69 million.

HDIN Institutional Perspective

While the prospectus aggressively markets Evopoint's "1+3+N" strategy as a seamless transition from biotech to an integrated biopharma entity, forensic equity analysis reveals latent execution friction unpriced by the Street. The firm holds an impenetrable IP moat (composition patents valid through 2039/2041) and faces zero material impact from an ongoing $6.96 million trade secret suit filed by Hangzhou Xin Yuansu. However, its voting structure is intensely concentrated: Actual controller Qiang Jing controls 47.0448% of voting rights (Direct 0.8218%, Lipan 21.5802%, Youyao 10.0154%, Xinkang 4.4875%, Chenghuai 0.3927%, Youxiao 0.1122%, plus 9.6350% via CEO Le Meijie).

This centralized governance minimizes activist interference but amplifies key-man risk during the critical 2026-2028 commercial rollout. Despite this, the institutional capitalization table acts as a formidable buffer. Top-tier LPs, including Tencent (5.7615%), Loyal Valley Capital (12.9965%), CICC (1.0975%), CDH (1.0274%), and Kailaiying (2.2885%), are locked in for 12 to 36 months post-IPO. We argue that Evopoint's deliberate avoidance of heavy CapEx expansion—eschewing massive biologic facility builds in favor of CDMO partnerships—represents apex capital efficiency. The firm is economically insulated; even if XNW4107's 2026 Tier-3 hospital commercial launch underperforms, the guaranteed waterfall of Astellas milestones ensures operational solvency through the end of the decade.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."