CentryMed: R&D Pivot Near Hangzhou Clinical Hub as Asset-Light Model Signals Execution Bottlenecks Ahead of 2030 NDA Targets

Date : 2026-05-21

Reading : 73

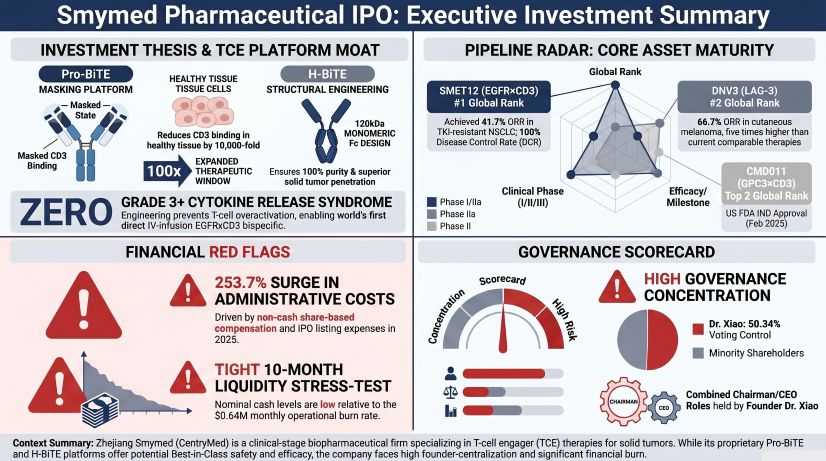

CentryMed’s 2025 filings reveal a highly leveraged, asset-light biotechnology firm prioritizing late-stage T-cell engager (TCE) therapies over operational infrastructure. While a 253.7% spike in administrative expenses appears alarming, our Forensic Analysis isolates this to pre-IPO share-based compensation. The firm is actively navigating a capital preservation mandate in Mainland China. For institutional LPs, the $441 million pre-IPO valuation prices in an aggressive intellectual property moat, yet the reliance on outsourced clinical infrastructure poses a critical execution vulnerability as the company approaches pivotal Phase III trials.

Figure Smymed Pharmaceutical (CentryMed) lPO Executive Investment Summary

Forensic Analysis of Pre-IPO Financials & Segmental R&D Capital Allocation

Forensic Analysis of Pre-IPO Financials & Segmental R&D Capital Allocation

The company’s fundamental cash-burn trajectory remains highly stable. The reported 2025 net loss widening to $11.26 million USD (80.96 million CNY) is a structural accounting artifact. Adjusting for $2.74 million USD (19.67 million CNY) in non-cash Share-Based Compensation (SBC), the operational net loss sits at a manageable $8.53 million USD.

A Forensic Analysis of segmental capital allocation reveals a deliberate clinical prioritization strategy rather than a pipeline setback:

* Operating Leverage & Liquidity: CentryMed maintains a monthly cash burn rate of just $0.64 million USD. Backed by $20.31 million USD in short-term liquidity (including $12.07 million USD in FVTPL assets) and a post-reporting $23.67 million USD Pre-IPO capital injection in early 2026, the company holds an estimated 31.7-month cash runway.

* DNV3 (LAG-3 TCM): R&D expenditure surged by 71.9% year-over-year to $2.69 million USD, driving resource-intensive Phase II combination trials. The asset demonstrates a 66.7% Objective Response Rate (ORR) in cutaneous melanoma, substantially outperforming existing comparable therapies.

* SMET12 (EGFR×CD3 TCE): R&D expenditure declined by 38.4% to $1.02 million USD. This reflects a strategic pause in combination trials to aggressively fund the Phase IIa monotherapy trial (CTR20212374), capitalizing on its 100% Disease Control Rate (DCR) and 41.7% ORR in TKI-resistant NSCLC.

* Unit Economics & Structuring: Utilizing the proprietary H-BiTE platform, assets like SMET12 maintain a low molecular weight of ~120-128kDa (versus 150kDa for traditional IgGs), directly enhancing solid tumor penetration and circumventing the systemic CRS toxicity that traditionally requires intensive inpatient care.

Supply Chain Audit & Geo-Economic Moat

The physicality of CentryMed’s business relies entirely on an outsourced Tier-1 network within Mainland China, exposing the firm to distinct structural margins and IP backlogs.

* Vendor Concentration Risk: In 2025, the top five suppliers accounted for 58.1% of total procurement ($2.17 million USD). The firm utilizes MabPlex (Yantai-based CDMO) for clinical sample manufacturing (9.8% of 2025 procurement) and Hangzhou Tigermed (CRO) for trial execution. While management claims high market substitutability, any capacity bottleneck at MabPlex poses a material threat to the Q3/Q4 2027 Phase III initiation deadlines for DNV3 and SMET12.

* Protease-Activated IP Vulnerabilities: The proprietary Pro-BiTE platform reduces off-target CD3 binding by 10,000-fold compared to unmasked competitors like JANX008 (1,000-fold). However, international patent backlogs—specifically US18/691,036 for CMD011 and EP19900194.2 for SMET12—leave the assets vulnerable to overlapping structural claims in the highly contested global biopharma bispecific sector.

* Regulatory & ESG Compliance: The historical underpayment of employee social security and housing funds ($180,870 USD across 2024-2025) has been audited as a non-material administrative shortfall. New September 2025 Chinese judicial interpretations on labor disputes do not alter the firm’s IPO viability, with GCP and hazardous waste compliance (outsourced to third parties) remaining intact.

HDIN Institutional Perspective: Valuation Anomalies & Execution Vulnerabilities

While CentryMed justifies a per-employee valuation premium of $8.65 million USD (based on a 51-person headcount and a $441.06 million USD Pre-IPO valuation), HDIN Research views this metric as operationally deceptive. The valuation accurately prices the intrinsic IP of four distinct clinical-stage assets, yet the underlying "micro-team" R&D structure presents a severe bandwidth constraint.

A 15-person clinical team acting merely as "architects" over a massive outsourced CRO network is viable for Phase IIa. However, navigating global Phase III trials and transitioning into the planned 2026-2028 domestic commercialization phase requires immediate and aggressive internal scaling. Furthermore, the absence of internal commercial-scale manufacturing permanently caps the firm’s long-term gross margins by shifting fixed CAPEX into variable, margin-diluting COGS via CDMO profit sharing. Investors should anticipate significant Selling, General, and Administrative (SG&A) inflation over the next 24 months, which will inevitably normalize this valuation anomaly back to Hong Kong Chapter 18A industry medians.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Smymed Pharmaceutical (CentryMed) lPO Executive Investment Summary

Forensic Analysis of Pre-IPO Financials & Segmental R&D Capital AllocationThe company’s fundamental cash-burn trajectory remains highly stable. The reported 2025 net loss widening to $11.26 million USD (80.96 million CNY) is a structural accounting artifact. Adjusting for $2.74 million USD (19.67 million CNY) in non-cash Share-Based Compensation (SBC), the operational net loss sits at a manageable $8.53 million USD.

A Forensic Analysis of segmental capital allocation reveals a deliberate clinical prioritization strategy rather than a pipeline setback:

* Operating Leverage & Liquidity: CentryMed maintains a monthly cash burn rate of just $0.64 million USD. Backed by $20.31 million USD in short-term liquidity (including $12.07 million USD in FVTPL assets) and a post-reporting $23.67 million USD Pre-IPO capital injection in early 2026, the company holds an estimated 31.7-month cash runway.

* DNV3 (LAG-3 TCM): R&D expenditure surged by 71.9% year-over-year to $2.69 million USD, driving resource-intensive Phase II combination trials. The asset demonstrates a 66.7% Objective Response Rate (ORR) in cutaneous melanoma, substantially outperforming existing comparable therapies.

* SMET12 (EGFR×CD3 TCE): R&D expenditure declined by 38.4% to $1.02 million USD. This reflects a strategic pause in combination trials to aggressively fund the Phase IIa monotherapy trial (CTR20212374), capitalizing on its 100% Disease Control Rate (DCR) and 41.7% ORR in TKI-resistant NSCLC.

* Unit Economics & Structuring: Utilizing the proprietary H-BiTE platform, assets like SMET12 maintain a low molecular weight of ~120-128kDa (versus 150kDa for traditional IgGs), directly enhancing solid tumor penetration and circumventing the systemic CRS toxicity that traditionally requires intensive inpatient care.

Supply Chain Audit & Geo-Economic Moat

The physicality of CentryMed’s business relies entirely on an outsourced Tier-1 network within Mainland China, exposing the firm to distinct structural margins and IP backlogs.

* Vendor Concentration Risk: In 2025, the top five suppliers accounted for 58.1% of total procurement ($2.17 million USD). The firm utilizes MabPlex (Yantai-based CDMO) for clinical sample manufacturing (9.8% of 2025 procurement) and Hangzhou Tigermed (CRO) for trial execution. While management claims high market substitutability, any capacity bottleneck at MabPlex poses a material threat to the Q3/Q4 2027 Phase III initiation deadlines for DNV3 and SMET12.

* Protease-Activated IP Vulnerabilities: The proprietary Pro-BiTE platform reduces off-target CD3 binding by 10,000-fold compared to unmasked competitors like JANX008 (1,000-fold). However, international patent backlogs—specifically US18/691,036 for CMD011 and EP19900194.2 for SMET12—leave the assets vulnerable to overlapping structural claims in the highly contested global biopharma bispecific sector.

* Regulatory & ESG Compliance: The historical underpayment of employee social security and housing funds ($180,870 USD across 2024-2025) has been audited as a non-material administrative shortfall. New September 2025 Chinese judicial interpretations on labor disputes do not alter the firm’s IPO viability, with GCP and hazardous waste compliance (outsourced to third parties) remaining intact.

HDIN Institutional Perspective: Valuation Anomalies & Execution Vulnerabilities

While CentryMed justifies a per-employee valuation premium of $8.65 million USD (based on a 51-person headcount and a $441.06 million USD Pre-IPO valuation), HDIN Research views this metric as operationally deceptive. The valuation accurately prices the intrinsic IP of four distinct clinical-stage assets, yet the underlying "micro-team" R&D structure presents a severe bandwidth constraint.

A 15-person clinical team acting merely as "architects" over a massive outsourced CRO network is viable for Phase IIa. However, navigating global Phase III trials and transitioning into the planned 2026-2028 domestic commercialization phase requires immediate and aggressive internal scaling. Furthermore, the absence of internal commercial-scale manufacturing permanently caps the firm’s long-term gross margins by shifting fixed CAPEX into variable, margin-diluting COGS via CDMO profit sharing. Investors should anticipate significant Selling, General, and Administrative (SG&A) inflation over the next 24 months, which will inevitably normalize this valuation anomaly back to Hong Kong Chapter 18A industry medians.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."