Alibaba Group: Full-Stack AI Pivot Near Hangzhou Headquarters as Negative Free Cash Flow Signals Peak Infrastructure Reinvestment Phase

Date : 2026-05-22

Reading : 267

Alibaba’s Fiscal 2026 disclosures reveal a decisive structural transition, characterized by a $17.54 billion capital expenditure surge that drove free cash flow negative ($6.48 billion). This aggressive capital reallocation toward proprietary T-Head GPUs and Model-as-a-Service infrastructure is a direct strategic countermeasure to stringent U.S. semiconductor export controls. For institutional LPs, this signals a near-term margin compression cycle but establishes a fortified, self-reliant technological moat designed to capture next-generation enterprise AI demand across the Asia-Pacific and broader emerging markets.

Figure Alibaba Group FY2026: Strategic Pivot to an Al-Native Ecosystem

Forensic Analysis of Fiscal 2026 Segmental Leverage and Profitability Contraction

Forensic Analysis of Fiscal 2026 Segmental Leverage and Profitability Contraction

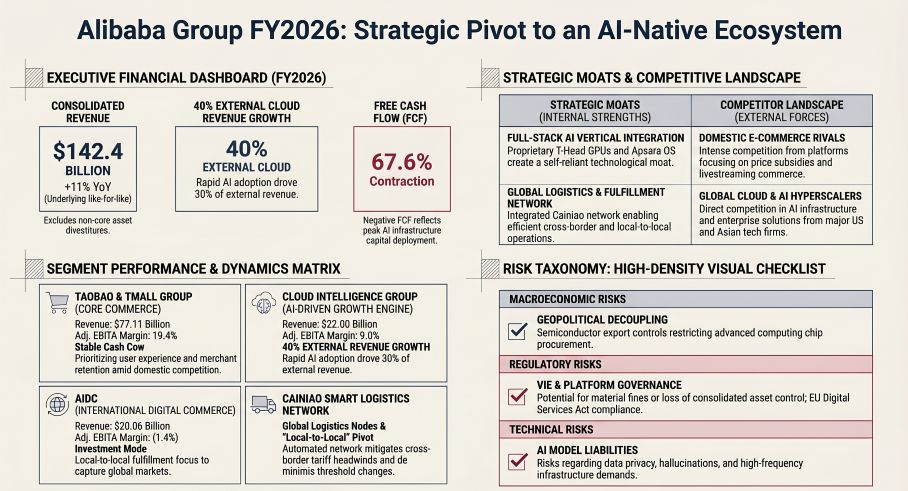

The FY2026 reorganization simplifies NYSE: BABA (also HKEX: 9988) into core pillars, reflecting a severe but deliberate margin compression as the firm prioritizes technological dominance over near-term profitability. Consolidated revenue reached $142,423.65 million (+3% YoY, +11% on a like-for-like basis excluding divested non-core assets), but operating margins collapsed from 14% to 5%.

Segmental Inventory & Quantitative Metrics:

* Alibaba China E-commerce Group: Revenue hit $77,108.45 million (+9% YoY), capturing 54% of total revenue. Adjusted EBITA fell 44% to $14,957.77 million (19.4% margin), diluted by intense reinvestment into Taobao Instant Commerce (which surged 47%) and the September 2024 implementation of a new GMV-based software service fee framework.

* Cloud Intelligence Group: The fastest-growing segment generated $22,000.97 million (+34% YoY) with an Adjusted EBITA of $1,984.70 million (9.0% margin). External cloud revenue growth accelerated to 40% in Q4 FY2026, with AI-related products (driven by the Qwen model family and Wukong B2B agents) driving 30% of this expansion.

* AIDC (International Commerce): Revenue grew 9% to $20,058.43 million. Adjusted EBITA losses narrowed by 86% to $(285.36) million, driven by operational efficiencies at AliExpress.

* Capital Allocation & Cash Flow Variance: Free Cash Flow (FCF) inverted from a positive $10,277.56 million in FY2025 to an outflow of $(6,484.73) million. This operational cash burn funded a 47% YoY surge in CAPEX to $17,539.20 million. Concurrently, share repurchases were drastically curtailed to $1,062.68 million (down from $12,057.32 million in FY2025), while dividends stood at $4,693.15 million.

* R&D to Moat Translation: Product development expenses expanded to $9,256.77 million (7% of total revenue). This funded the proprietary Apsara distributed computing operating system and an $800 million strategic equity injection into Moonshot AI Ltd (36% stake).

* Asset Rationalization: Management aggressively purged underperforming legacy assets, booking a $1,323.8 million goodwill impairment primarily in digital media and finalizing the disposal of Sun Art Retail and Intime Retail physical footprints.

Supply Chain Localization and Infrastructure Resilience

Alibaba’s physical and digital footprint is rapidly decentralizing to hedge against systemic macroeconomic and regulatory friction. The company commands 18.7 million square meters of owned gross floor area, pivoting logistics from cross-border reliance to highly capitalized "local-to-local" fulfillment.

* Global Node Control & Regulatory Mitigation: The elimination of the $169.59 (€150) duty-free threshold in the EU (effective July 1, 2026) and the proposed elimination of the U.S. $800 de minimis threshold forces a structural supply chain shift. In response, the AliExpressDirect model now localizes inventory across more than 30 countries. Furthermore, Cainiao utilizes advanced automated hardware like ZeeBot climbing robots across its European hubs to lower unit fulfillment costs.

* Data Center Footprint & Sanctions Hedging: Cloud Intelligence operates across 34 regions, spanning hubs from the United Arab Emirates and Germany to Mexico and Southeast Asia. To counter U.S. export controls and potential disruptions from the April 2025 U.S. DOJ bulk data rule, Alibaba is scaling production of its in-house T-Head GPUs. These chips are co-designed with Qwen foundation models to optimize price-performance and circumvent reliance on restricted top-tier international semiconductors.

* Contingent Liabilities & Off-Balance Sheet Exposure: The firm is anchored by $27,834.71 million in forward commitments for bandwidth and co-location, alongside $7,848.49 million in contracted, unprovided capital commitments earmarked for AI hardware. Geopolitically, the most severe tail risk stems from the EU Digital Services Act (DSA); AliExpress is under formal investigation as a Very Large Online Platform (VLOP), carrying maximum penalty exposure of up to 6% of global turnover. Additionally, a $705.53 million drawdown against an $833.80 million guarantee supports the Hong Kong Cingleot Investment Management logistics center at Hong Kong International Airport.

HDIN Institutional Perspective

While management positions the $6.48 billion free cash flow burn as a necessary transition toward an AI-driven ecosystem, forensic data suggests a defensive rather than purely offensive posture. The $27.8 billion in long-term bandwidth/co-location commitments, combined with the structural requirement to pivot to capital-intensive "local-to-local" logistics due to collapsing global de minimis tariff exemptions, indicates that NYSE: BABA is structurally absorbing higher baseline operating costs just to maintain its existing global logistics moat. The Street may be underestimating the prolonged margin dilution inherent in this geopolitical compliance cycle. However, the unrestricted liquidity pool of $72,462.47 million against total debt of $36,173.36 million confirms the balance sheet is vastly under-leveraged, providing ample runway to subsidize this multi-year "involutionary" pricing war without risking global solvency.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Alibaba Group FY2026: Strategic Pivot to an Al-Native Ecosystem

Forensic Analysis of Fiscal 2026 Segmental Leverage and Profitability ContractionThe FY2026 reorganization simplifies NYSE: BABA (also HKEX: 9988) into core pillars, reflecting a severe but deliberate margin compression as the firm prioritizes technological dominance over near-term profitability. Consolidated revenue reached $142,423.65 million (+3% YoY, +11% on a like-for-like basis excluding divested non-core assets), but operating margins collapsed from 14% to 5%.

Segmental Inventory & Quantitative Metrics:

* Alibaba China E-commerce Group: Revenue hit $77,108.45 million (+9% YoY), capturing 54% of total revenue. Adjusted EBITA fell 44% to $14,957.77 million (19.4% margin), diluted by intense reinvestment into Taobao Instant Commerce (which surged 47%) and the September 2024 implementation of a new GMV-based software service fee framework.

* Cloud Intelligence Group: The fastest-growing segment generated $22,000.97 million (+34% YoY) with an Adjusted EBITA of $1,984.70 million (9.0% margin). External cloud revenue growth accelerated to 40% in Q4 FY2026, with AI-related products (driven by the Qwen model family and Wukong B2B agents) driving 30% of this expansion.

* AIDC (International Commerce): Revenue grew 9% to $20,058.43 million. Adjusted EBITA losses narrowed by 86% to $(285.36) million, driven by operational efficiencies at AliExpress.

* Capital Allocation & Cash Flow Variance: Free Cash Flow (FCF) inverted from a positive $10,277.56 million in FY2025 to an outflow of $(6,484.73) million. This operational cash burn funded a 47% YoY surge in CAPEX to $17,539.20 million. Concurrently, share repurchases were drastically curtailed to $1,062.68 million (down from $12,057.32 million in FY2025), while dividends stood at $4,693.15 million.

* R&D to Moat Translation: Product development expenses expanded to $9,256.77 million (7% of total revenue). This funded the proprietary Apsara distributed computing operating system and an $800 million strategic equity injection into Moonshot AI Ltd (36% stake).

* Asset Rationalization: Management aggressively purged underperforming legacy assets, booking a $1,323.8 million goodwill impairment primarily in digital media and finalizing the disposal of Sun Art Retail and Intime Retail physical footprints.

Supply Chain Localization and Infrastructure Resilience

Alibaba’s physical and digital footprint is rapidly decentralizing to hedge against systemic macroeconomic and regulatory friction. The company commands 18.7 million square meters of owned gross floor area, pivoting logistics from cross-border reliance to highly capitalized "local-to-local" fulfillment.

* Global Node Control & Regulatory Mitigation: The elimination of the $169.59 (€150) duty-free threshold in the EU (effective July 1, 2026) and the proposed elimination of the U.S. $800 de minimis threshold forces a structural supply chain shift. In response, the AliExpressDirect model now localizes inventory across more than 30 countries. Furthermore, Cainiao utilizes advanced automated hardware like ZeeBot climbing robots across its European hubs to lower unit fulfillment costs.

* Data Center Footprint & Sanctions Hedging: Cloud Intelligence operates across 34 regions, spanning hubs from the United Arab Emirates and Germany to Mexico and Southeast Asia. To counter U.S. export controls and potential disruptions from the April 2025 U.S. DOJ bulk data rule, Alibaba is scaling production of its in-house T-Head GPUs. These chips are co-designed with Qwen foundation models to optimize price-performance and circumvent reliance on restricted top-tier international semiconductors.

* Contingent Liabilities & Off-Balance Sheet Exposure: The firm is anchored by $27,834.71 million in forward commitments for bandwidth and co-location, alongside $7,848.49 million in contracted, unprovided capital commitments earmarked for AI hardware. Geopolitically, the most severe tail risk stems from the EU Digital Services Act (DSA); AliExpress is under formal investigation as a Very Large Online Platform (VLOP), carrying maximum penalty exposure of up to 6% of global turnover. Additionally, a $705.53 million drawdown against an $833.80 million guarantee supports the Hong Kong Cingleot Investment Management logistics center at Hong Kong International Airport.

HDIN Institutional Perspective

While management positions the $6.48 billion free cash flow burn as a necessary transition toward an AI-driven ecosystem, forensic data suggests a defensive rather than purely offensive posture. The $27.8 billion in long-term bandwidth/co-location commitments, combined with the structural requirement to pivot to capital-intensive "local-to-local" logistics due to collapsing global de minimis tariff exemptions, indicates that NYSE: BABA is structurally absorbing higher baseline operating costs just to maintain its existing global logistics moat. The Street may be underestimating the prolonged margin dilution inherent in this geopolitical compliance cycle. However, the unrestricted liquidity pool of $72,462.47 million against total debt of $36,173.36 million confirms the balance sheet is vastly under-leveraged, providing ample runway to subsidize this multi-year "involutionary" pricing war without risking global solvency.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."