Space Exploration Technologies Corp. (SpaceX): Hyperscale Pivot Near Memphis COLOSSUS Campuses as $10.1 Billion Q1 Capital Expenditure Signals Severe 2027 Refinancing Risk

Date : 2026-05-21

Reading : 643

Space Exploration Technologies Corp. (SpaceX)'s transition from an aerospace contractor into an artificial intelligence infrastructure conglomerate is masking a severe structural capital deterioration. While the Starlink network generates $7.16 billion in segment adjusted EBITDA, this liquidity is aggressively siphoned to fund the Memphis COLOSSUS data centers and Starship development. For institutional allocators, the critical narrative isn't the 33% top-line growth; it is the $20.0 billion debt maturity wall looming in September 2027. Without an immediate, optimally valued public offering to clear this bridge loan, the enterprise faces existential capital structure friction.

Figure SpaceX Historic S-1 lPO Deconstruction: Capital Architecture, Market Dominance, and Multi-Industry Risks

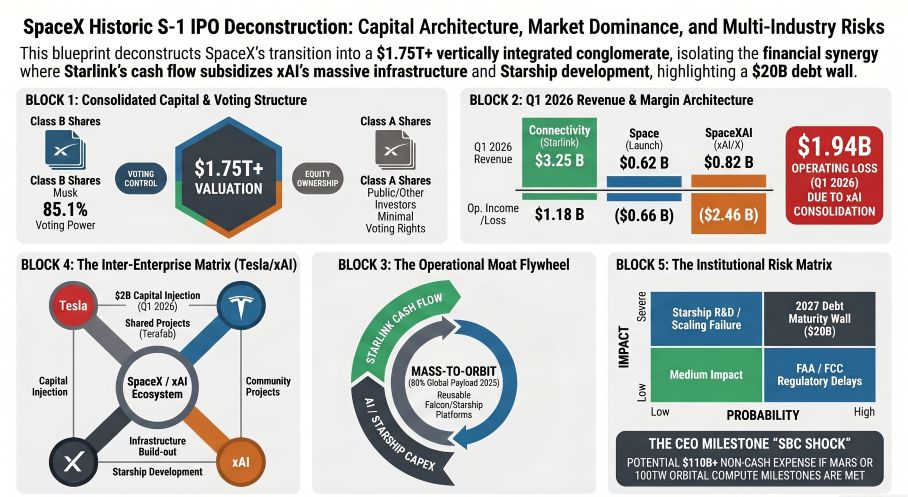

Segmental Profitability Variance & Solvency Metrics Audit

Segmental Profitability Variance & Solvency Metrics Audit

A forensic analysis of the FY 2025 and Q1 2026 financial disclosures reveals explosive revenue scaling fundamentally offset by an unprecedented capital intensity profile. Operating leverage is entirely skewed by the internal cross-subsidization of the AI and Space segments.

* Consolidated Top-Line & Gross Margins: FY 2025 total revenue reached $18.67 billion (+33.2% YoY) with an expanded gross margin of 49.4%. Q1 2026 revenue accelerated 15.4% YoY to $4.69 billion.

* Operating Margin Drag (The AI Penalty): Despite Starlink generating robust cash flows, consolidated operating losses widened to $(2.58) billion in FY 2025 and $(1.94) billion in Q1 2026. This was driven by a 149.5% surge in FY 2025 R&D ($8.64 billion total), heavily allocated to Grok compute infrastructure and Starship engineering. The AI Segment alone posted an operating loss of $(2.46) billion in Q1 2026.

* Unit Economics & Price-Mix Variance: Global weighted-average ARPU for Starlink intentionally deflated from $81/month in FY 2025 to $66/month in Q1 2026, signaling a highly aggressive, margin-dilutive pricing strategy to penetrate emerging markets.

* Free Cash Flow (FCF) Deficits: The enterprise reported positive Operating Cash Flow of $6.78 billion in FY 2025, but this was artificially buoyed by $13.2 billion in deferred revenue (upfront customer float). Real capital expenditures reached $20.7 billion in FY 2025 and a staggering $10.1 billion in Q1 2026 alone, resulting in a calculated FCF deficit of $(13.9) billion (FY 2025) and $(9.1) billion (Q1 2026).

* Related-Party Mergers & Financial Engineering: The February 2026 integration of xAI required a 0.1433 conversion ratio and triggered $2.947 billion in cash payouts to equity holders. The Q1 2026 net loss of $(4.27) billion included a one-time $1.52 billion debt extinguishment penalty required to consolidate legacy xAI obligations into the new Space Exploration Technologies Corp. capital structure.

* The Dilution Overhang: CEO Elon Musk holds 85.1% of the total voting power and possesses unvested performance grants totaling roughly 1.3 billion Class B shares. Because these operational milestones (a Mars colony, 100 terawatts of orbital compute) are deemed "improbable" by accounting standards, zero expense is currently recognized. Triggering these milestones will result in a retroactive, non-cash P&L hit estimated to exceed $110 billion.

Industrial Capital Expenditure & Geo-Economic Infrastructure Integration

Space Exploration Technologies Corp. mandates an extreme physical footprint, shifting from aerospace manufacturing dependency to gigawatt-scale energy consumption and geopolitical regulatory constraints.

* Terrestrial AI & Compute Hubs: The $7.7 billion AI CapEx deployed in Q1 2026 is concentrated in Memphis, Tennessee, and Southaven, Mississippi. These locations host the COLOSSUS and COLOSSUS II campuses, which collectively demand 1.0 gigawatt of power. The company has secured $1.7 billion in forward commitments for natural gas turbines to bypass regional grid constraints.

* Aerospace Manufacturing & Global Logistics: Operations rely on Starbase in Cameron County, Texas (housing Starfactory and the Gigabay integration facility) and the primary propulsion testing hub in McGregor, Texas. Broadband physical assets are produced in Redmond, Washington (manufacturing ~70 satellites weekly), while Starlink Kits are assembled in Bastrop, Texas.

* The "Terafab" Semiconductor Framework: While management promotes a joint chip manufacturing initiative with NASDAQ: TSLA and NASDAQ: INTC to achieve 1 terawatt of annual compute production, the S-1 audit confirms this is currently a legally non-binding framework with zero auditable allocation of CapEx, JV equity ownership, or finalized IP cross-licensing.

* Geopolitical Blockades & Sovereign Risk: The company's operations are governed by strict ITAR export controls and OFAC sanctions, restricting global talent acquisition. Emerging market friction is acute; a precedent was set in August 2024 when Brazil's Supreme Court froze Starlink financial assets over a dispute regarding the X platform. Additionally, the European Commission recently levied a $135.67 million (EUR 120 million) fine for Digital Services Act violations.

HDIN Institutional Perspective

Challenge: While the S-1 prospectus promotes an impenetrable "shovels-to-tokens" vertical integration moat targeting a $28.5 trillion total addressable market, the $8.33 billion total cash burn in the AI segment during Q1 2026 alone suggests an unsustainable, hardware-intensive burn rate that institutional buyers have not fully priced in. The strategic narrative emphasizes deploying 100 gigawatts of orbital AI compute by 2028 via Starship V3 payloads; however, the immediate fiscal reality is a $20.0 billion unhedged bridge loan carrying a 4.58% effective interest rate, maturing in September 2027.

Space Exploration Technologies Corp. is trapped in a continuous replacement cycle—requiring the launch of over 2,000 short-lived satellites annually just to maintain baseline capacity. If tightening macroeconomic credit conditions or FAA regulatory delays stall the launch cadence, the company will be unable to generate the necessary IPO proceeds to clear the 2027 maturity wall, forcing either catastrophic debt rollover costs or unprecedented equity dilution.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

Figure SpaceX Historic S-1 lPO Deconstruction: Capital Architecture, Market Dominance, and Multi-Industry Risks

Segmental Profitability Variance & Solvency Metrics AuditA forensic analysis of the FY 2025 and Q1 2026 financial disclosures reveals explosive revenue scaling fundamentally offset by an unprecedented capital intensity profile. Operating leverage is entirely skewed by the internal cross-subsidization of the AI and Space segments.

* Consolidated Top-Line & Gross Margins: FY 2025 total revenue reached $18.67 billion (+33.2% YoY) with an expanded gross margin of 49.4%. Q1 2026 revenue accelerated 15.4% YoY to $4.69 billion.

* Operating Margin Drag (The AI Penalty): Despite Starlink generating robust cash flows, consolidated operating losses widened to $(2.58) billion in FY 2025 and $(1.94) billion in Q1 2026. This was driven by a 149.5% surge in FY 2025 R&D ($8.64 billion total), heavily allocated to Grok compute infrastructure and Starship engineering. The AI Segment alone posted an operating loss of $(2.46) billion in Q1 2026.

* Unit Economics & Price-Mix Variance: Global weighted-average ARPU for Starlink intentionally deflated from $81/month in FY 2025 to $66/month in Q1 2026, signaling a highly aggressive, margin-dilutive pricing strategy to penetrate emerging markets.

* Free Cash Flow (FCF) Deficits: The enterprise reported positive Operating Cash Flow of $6.78 billion in FY 2025, but this was artificially buoyed by $13.2 billion in deferred revenue (upfront customer float). Real capital expenditures reached $20.7 billion in FY 2025 and a staggering $10.1 billion in Q1 2026 alone, resulting in a calculated FCF deficit of $(13.9) billion (FY 2025) and $(9.1) billion (Q1 2026).

* Related-Party Mergers & Financial Engineering: The February 2026 integration of xAI required a 0.1433 conversion ratio and triggered $2.947 billion in cash payouts to equity holders. The Q1 2026 net loss of $(4.27) billion included a one-time $1.52 billion debt extinguishment penalty required to consolidate legacy xAI obligations into the new Space Exploration Technologies Corp. capital structure.

* The Dilution Overhang: CEO Elon Musk holds 85.1% of the total voting power and possesses unvested performance grants totaling roughly 1.3 billion Class B shares. Because these operational milestones (a Mars colony, 100 terawatts of orbital compute) are deemed "improbable" by accounting standards, zero expense is currently recognized. Triggering these milestones will result in a retroactive, non-cash P&L hit estimated to exceed $110 billion.

Industrial Capital Expenditure & Geo-Economic Infrastructure Integration

Space Exploration Technologies Corp. mandates an extreme physical footprint, shifting from aerospace manufacturing dependency to gigawatt-scale energy consumption and geopolitical regulatory constraints.

* Terrestrial AI & Compute Hubs: The $7.7 billion AI CapEx deployed in Q1 2026 is concentrated in Memphis, Tennessee, and Southaven, Mississippi. These locations host the COLOSSUS and COLOSSUS II campuses, which collectively demand 1.0 gigawatt of power. The company has secured $1.7 billion in forward commitments for natural gas turbines to bypass regional grid constraints.

* Aerospace Manufacturing & Global Logistics: Operations rely on Starbase in Cameron County, Texas (housing Starfactory and the Gigabay integration facility) and the primary propulsion testing hub in McGregor, Texas. Broadband physical assets are produced in Redmond, Washington (manufacturing ~70 satellites weekly), while Starlink Kits are assembled in Bastrop, Texas.

* The "Terafab" Semiconductor Framework: While management promotes a joint chip manufacturing initiative with NASDAQ: TSLA and NASDAQ: INTC to achieve 1 terawatt of annual compute production, the S-1 audit confirms this is currently a legally non-binding framework with zero auditable allocation of CapEx, JV equity ownership, or finalized IP cross-licensing.

* Geopolitical Blockades & Sovereign Risk: The company's operations are governed by strict ITAR export controls and OFAC sanctions, restricting global talent acquisition. Emerging market friction is acute; a precedent was set in August 2024 when Brazil's Supreme Court froze Starlink financial assets over a dispute regarding the X platform. Additionally, the European Commission recently levied a $135.67 million (EUR 120 million) fine for Digital Services Act violations.

HDIN Institutional Perspective

Challenge: While the S-1 prospectus promotes an impenetrable "shovels-to-tokens" vertical integration moat targeting a $28.5 trillion total addressable market, the $8.33 billion total cash burn in the AI segment during Q1 2026 alone suggests an unsustainable, hardware-intensive burn rate that institutional buyers have not fully priced in. The strategic narrative emphasizes deploying 100 gigawatts of orbital AI compute by 2028 via Starship V3 payloads; however, the immediate fiscal reality is a $20.0 billion unhedged bridge loan carrying a 4.58% effective interest rate, maturing in September 2027.

Space Exploration Technologies Corp. is trapped in a continuous replacement cycle—requiring the launch of over 2,000 short-lived satellites annually just to maintain baseline capacity. If tightening macroeconomic credit conditions or FAA regulatory delays stall the launch cadence, the company will be unable to generate the necessary IPO proceeds to clear the 2027 maturity wall, forcing either catastrophic debt rollover costs or unprecedented equity dilution.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*