Parabilis Medicines: Pivot to Global Phase 3 Trials Near Cambridge and Shanghai Hubs as $454 Million Liquidity Signals Aggressive Clinical Execution

Date : 2026-05-23

Reading : 718

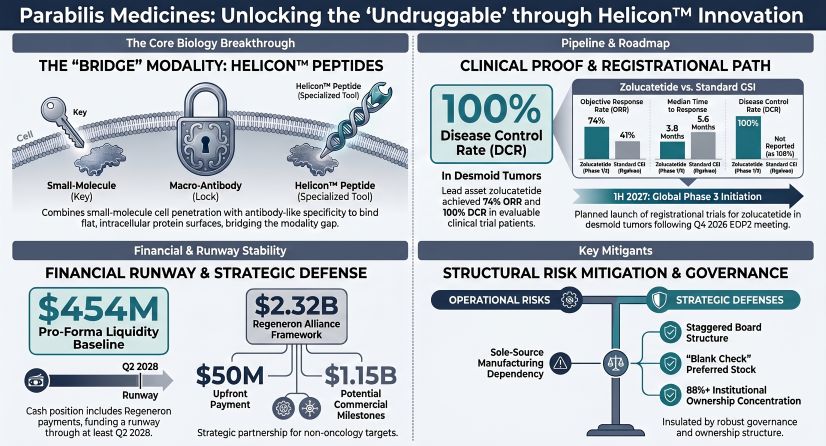

Parabilis Medicines approaches the public markets backed by a robust $454.04 million pro-forma liquidity position, fortified by a highly lucrative alliance with Regeneron (NASDAQ: REGN). However, the S-1 filing reveals acute geopolitical vulnerabilities: the company’s reliance on WuXi AppTec Co. Ltd. for active pharmaceutical ingredients exposes it directly to the U.S. BIOSECURE Act. For institutional LPs, Parabilis presents a bifurcated profile—a structurally monopolistic oncology pipeline yielding a 74% objective response rate in desmoid tumors, weighed against impending Phase 3 burn velocity and severe supply chain concentration risks ahead of its Q4 2026 FDA EOP2 meeting.

Figure Parabilis Medicines: Unlocking the Undruggable through Helicon Innovation

Capitalization Structure, Burn Velocity & Dilution Mechanics

Capitalization Structure, Burn Velocity & Dilution Mechanics

Operating as a pre-revenue biopharmaceutical entity, Parabilis Medicines exhibits an aggressive capital burn profile intrinsic to advancing a novel biologic modality. With zero product revenue, the company has amassed a $586.82 million accumulated deficit as of March 31, 2026.

Table Operating Expense Dynamics & Capital Deficit Trajectory (in $ Millions)

Structural Cost Drivers & Forward Guidance:

The 53.1% Q1 2026 G&A spike was catalyzed by $1.8 million in heightened professional fees for IPO preparations and intellectual property litigation defense, alongside $0.9 million in severance and personnel expansion. R&D acceleration remains anchored to the lead asset, zolucatetide, which drove $9.2 million in FY25 external clinical costs, supplemented by $5.5 million combined for ERG and ARON degrader preclinical programs.

Annualizing Q1 2026 data establishes a baseline burn of ~$197 million. However, factoring in public company overhead and the 1H 2027 initiation of a global Phase 3 trial, forward OCF burn is projected to expand 20% to 30%, reaching $235 million to $255 million annually. Current pro-forma liquidity provides 21 to 23 months of runway (funding operations into Q2 2028).

Dilution & Liquidity Overhang:

Incoming retail equities will absorb immediate Net Tangible Book Value (NTBV) dilution driven by two heavily discounted instruments. A $50.0 million SAFE converts at a mathematically capped price of $6.1644 per share (or a 10% IPO discount, whichever is lower), while the $75.0 million Regeneron private placement secures equity at 90% of the IPO price. Crucially, post-180-day lock-up expiration will trigger a massive market overhang, rendering 119,586,303 pre-IPO baseline shares—currently held by institutional giants like Fidelity (11.27%) and RA Capital (9.97%)—eligible for public dumping via highly negotiated Demand and Piggyback registration rights.

Physical Infrastructure, Supply Chain Audit & Geo-Economic Vulnerabilities

Parabilis Medicines operates an asset-light, structurally outsourced supply chain that introduces critical single-point-of-failure and geopolitical risks.

* R&D Innovation Hubs: The scientific core is anchored at the 122,000-square-foot Cambridge Headquarters in Massachusetts, integrated with non-GMP laboratories under a lease expiring in February 2031. Critical *in vivo* toxicology testing occurs at leased Massachusetts Vivarium Facilities (expiring December 2027), which are currently facing operational constraints due to a severe global shortage of non-human primates (NHPs).

* Geo-Economic Expansion: To support global trial enrollment for the planned 1H 2027 Phase 3 trial, the company established Parabilis Medicines (Shanghai) Ltd Co. as a wholly-owned Chinese subsidiary in March 2026. Clinical trial sites are actively being expanded into Australia and China to augment the existing U.S. network.

* Manufacturing Bottlenecks & BIOSECURE Exposure: The company does not own internal cGMP facilities. Active Pharmaceutical Ingredient (API) supply is precariously dual-sourced from Bachem Americas, Inc. and WuXi AppTec Co. Ltd. (China). Should WuXi be officially designated a "biotechnology company of concern" under the U.S. BIOSECURE Act, Parabilis faces immediate federal contracting blockades. Furthermore, Alcami Corporation acts as the sole-source supplier for the finished Drug Product (DP), leaving clinical timelines entirely exposed to Alcami's capacity and cold-chain/cryopreservation logistics.

HDIN Institutional Perspective

While the S-1 aggressively champions the Helicon™ platform as a "holy grail" modality capable of drugging flat intracellular Wnt/β-catenin targets (achieving a 74% ORR and 100% Disease Control Rate in desmoid tumors vs. Ogsiveo's 41% ORR), the Street is systematically underpricing a massive clinical delivery bottleneck.

Due to Grade 1 and Grade 2 injection site reactions (ISRs) in healthy volunteer bridging studies, Parabilis was forced to abandon its self-administered subcutaneous formulation. Consequently, the pivotal 1H 2027 Phase 3 trial is locked into an intravenous (IV) delivery mechanism. This places zolucatetide at a distinct commercial disadvantage against highly convenient oral $\gamma$-secretase inhibitors (GSIs) for chronic, lifelong disease management. Furthermore, with zero patents officially issued to protect the composition-of-matter for zolucatetide, and the underlying Harvard IP subject to U.S. Bayh-Dole Act march-in rights, the company's defensive moat is currently built entirely on pending applications and unissued claims. The Regeneron deal ($50M upfront, up to $1.15B in commercial milestones) validates the ex-oncology Helicon™ platform, but the core proprietary oncology pipeline faces intense formulation and FTO hurdles that public valuations have yet to reconcile.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Parabilis Medicines: Unlocking the Undruggable through Helicon Innovation

Capitalization Structure, Burn Velocity & Dilution MechanicsOperating as a pre-revenue biopharmaceutical entity, Parabilis Medicines exhibits an aggressive capital burn profile intrinsic to advancing a novel biologic modality. With zero product revenue, the company has amassed a $586.82 million accumulated deficit as of March 31, 2026.

Table Operating Expense Dynamics & Capital Deficit Trajectory (in $ Millions)

| Financial Metric | FY24 (USD Millions) | FY25 (USD Millions) | YoY Change | Q1'26 (USD Millions) | YTD Change |

|---|---|---|---|---|---|

| Research & Development (R&D) | $100.83 | $125.58 | +24.6% | $37.75 | +11.3% |

| General & Administrative (G&A) | $25.30 | $26.50 | +4.7% | $9.70 | +53.1% |

| Total Operating Expenses | $126.13 | $152.08 | — | $47.45 | — |

| Operating Cash Flow (OCF) Burn | $(103.61) | $(123.71) | — | $(49.20) | — |

| Net Loss | $(117.91) | $(145.89) | — | $(45.32) | — |

The 53.1% Q1 2026 G&A spike was catalyzed by $1.8 million in heightened professional fees for IPO preparations and intellectual property litigation defense, alongside $0.9 million in severance and personnel expansion. R&D acceleration remains anchored to the lead asset, zolucatetide, which drove $9.2 million in FY25 external clinical costs, supplemented by $5.5 million combined for ERG and ARON degrader preclinical programs.

Annualizing Q1 2026 data establishes a baseline burn of ~$197 million. However, factoring in public company overhead and the 1H 2027 initiation of a global Phase 3 trial, forward OCF burn is projected to expand 20% to 30%, reaching $235 million to $255 million annually. Current pro-forma liquidity provides 21 to 23 months of runway (funding operations into Q2 2028).

Dilution & Liquidity Overhang:

Incoming retail equities will absorb immediate Net Tangible Book Value (NTBV) dilution driven by two heavily discounted instruments. A $50.0 million SAFE converts at a mathematically capped price of $6.1644 per share (or a 10% IPO discount, whichever is lower), while the $75.0 million Regeneron private placement secures equity at 90% of the IPO price. Crucially, post-180-day lock-up expiration will trigger a massive market overhang, rendering 119,586,303 pre-IPO baseline shares—currently held by institutional giants like Fidelity (11.27%) and RA Capital (9.97%)—eligible for public dumping via highly negotiated Demand and Piggyback registration rights.

Physical Infrastructure, Supply Chain Audit & Geo-Economic Vulnerabilities

Parabilis Medicines operates an asset-light, structurally outsourced supply chain that introduces critical single-point-of-failure and geopolitical risks.

* R&D Innovation Hubs: The scientific core is anchored at the 122,000-square-foot Cambridge Headquarters in Massachusetts, integrated with non-GMP laboratories under a lease expiring in February 2031. Critical *in vivo* toxicology testing occurs at leased Massachusetts Vivarium Facilities (expiring December 2027), which are currently facing operational constraints due to a severe global shortage of non-human primates (NHPs).

* Geo-Economic Expansion: To support global trial enrollment for the planned 1H 2027 Phase 3 trial, the company established Parabilis Medicines (Shanghai) Ltd Co. as a wholly-owned Chinese subsidiary in March 2026. Clinical trial sites are actively being expanded into Australia and China to augment the existing U.S. network.

* Manufacturing Bottlenecks & BIOSECURE Exposure: The company does not own internal cGMP facilities. Active Pharmaceutical Ingredient (API) supply is precariously dual-sourced from Bachem Americas, Inc. and WuXi AppTec Co. Ltd. (China). Should WuXi be officially designated a "biotechnology company of concern" under the U.S. BIOSECURE Act, Parabilis faces immediate federal contracting blockades. Furthermore, Alcami Corporation acts as the sole-source supplier for the finished Drug Product (DP), leaving clinical timelines entirely exposed to Alcami's capacity and cold-chain/cryopreservation logistics.

HDIN Institutional Perspective

While the S-1 aggressively champions the Helicon™ platform as a "holy grail" modality capable of drugging flat intracellular Wnt/β-catenin targets (achieving a 74% ORR and 100% Disease Control Rate in desmoid tumors vs. Ogsiveo's 41% ORR), the Street is systematically underpricing a massive clinical delivery bottleneck.

Due to Grade 1 and Grade 2 injection site reactions (ISRs) in healthy volunteer bridging studies, Parabilis was forced to abandon its self-administered subcutaneous formulation. Consequently, the pivotal 1H 2027 Phase 3 trial is locked into an intravenous (IV) delivery mechanism. This places zolucatetide at a distinct commercial disadvantage against highly convenient oral $\gamma$-secretase inhibitors (GSIs) for chronic, lifelong disease management. Furthermore, with zero patents officially issued to protect the composition-of-matter for zolucatetide, and the underlying Harvard IP subject to U.S. Bayh-Dole Act march-in rights, the company's defensive moat is currently built entirely on pending applications and unissued claims. The Regeneron deal ($50M upfront, up to $1.15B in commercial milestones) validates the ex-oncology Helicon™ platform, but the core proprietary oncology pipeline faces intense formulation and FTO hurdles that public valuations have yet to reconcile.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."