Arverne Group: Dual-Valorization Pivot Near Schwabwiller as $2.15B CapEx Pipeline Signals Transition to Sovereign Infrastructure

Date : 2026-05-22

Reading : 151

Arverne Group’s 2025 structural pivot from external drilling contractor to sovereign infrastructure developer exposes a critical juncture in European energy autonomy. While the $88.20 million cash reserve and $56.53 million ORANE bridge facility secure near-term liquidity, achieving the 2031 dual-target of 27,000 tonnes of lithium and 4 TWh/year of geothermal heat demands overcoming a staggering $2.15 billion CapEx hurdle. For institutional allocators, Arverne represents a high-beta proxy for the EU Critical Raw Materials Act, pairing aggressive dilution risks against first-quartile operational economics driven by proprietary subsurface integration.

Figure Arverne Group 2025: Decoding the Geothermal-Lithium Nexus

Capital Deployment Architecture & Dilution Diagnostics

Capital Deployment Architecture & Dilution Diagnostics

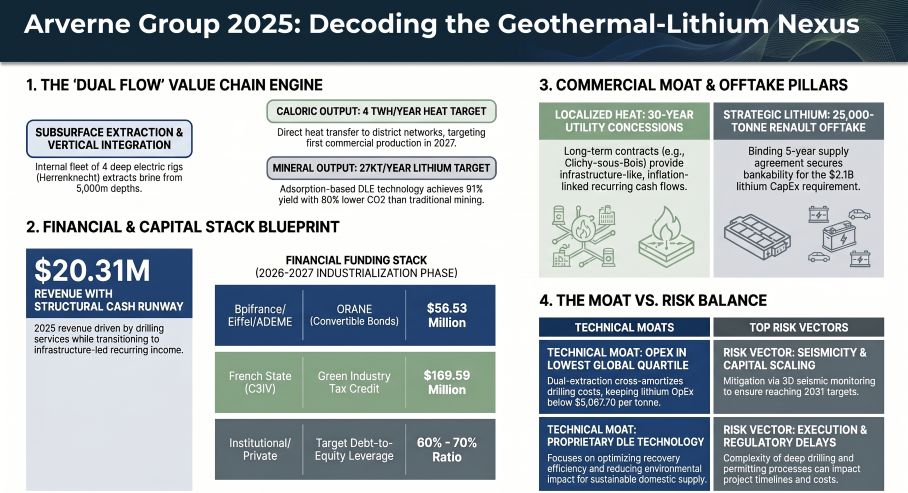

Arverne Group (Euronext Paris: ARV) is executing a highly capital-intensive transition. While consolidated top-line revenue expanded, the quality of earnings is entirely dependent on legacy B2B drilling contracts. Proprietary infrastructure assets remain in an accelerating cash-burn phase.

Forensic Analysis of 2025 Consolidated Financials:

* Top-Line & Segmental Margins: Total revenue hit $20.31 million. The Drilling & Well Construction division generated $19.13 million (94.2% of total) but operated at near-breakeven EBITDA (-$0.25 million). Proprietary geothermal (2gré) generated merely $0.95 million with a -$2.74 million EBITDA drag, while the pre-revenue Lithium de France (LDF) recorded an -$8.73 million EBITDA loss.

* Operating Leverage & Unit Economics: Through its "dual-valorization" model, baseline heat sales subsidize fixed infrastructure costs. This cross-amortization structurally lowers the Direct Lithium Extraction (DLE) estimated OpEx to below $5,087.70 per tonne of Lithium Carbonate Equivalent (LCE), placing it in the global first quartile.

* Cash Runway & Structuring Frictions: 2025 operating cash flow stood at -$15.66 million against a $43.66 million CapEx spend. While the $88.20 million year-end cash balance provides a 12-month runway, going-concern status hinges on the complex $56.53 million ORANE bridge bond. Carrying a 7% capitalized interest rate, the ORANE triggers automatic equity conversion at a punitive 20% discount if Arverne secures a public market raise.

* Minority Interest & Consolidation: Arverne executed a $25.24 million share swap with Hydro Energy Invest AS (issuing 2.23 million parent shares at $11.31) to increase its LDF stake to 73.83%. However, Equinor’s remaining 26.17% minority stake forces a $20.26 million non-controlling interest liability on the consolidated balance sheet.

Hardware Sovereignty & Upper Rhine Subsurface Footprint

Arverne's physical operations are entirely domestic, heavily concentrated in France to align with the state’s Multi-Year Energy Plan (PPE 3). The company's competitive moat is strictly defined by physical asset ownership and localized supply chain procurement.

* Proprietary Drilling Infrastructure: To bypass critical European rig shortages, Arverne internalizes operations utilizing 4 deep-drilling rigs, including the electric B18 and B04 co-developed with Herrenknecht AG.

* Alsace / Upper Rhine Graben Epicenter: The industrialization of the DLE process is anchored at the Schwabwiller site. The first geothermal doublet commenced drilling in November 2025 and completed its first well by February 2026. A DLE demonstrator, engineered via Pre-FEED/FEED contracts with Technip Energies and Sedgman, targets operational launch at this facility by late 2026.

* Tier-1 Supply Chain Buffer: To mitigate macro-inflationary shocks on $28.27 million-per-project geothermal CapEx profiles, Arverne executed strategic long-lead procurement agreements. This includes a master supply contract with Cameron France S.A.S. (SLB) for wellheads and a 5-year casing supply agreement with Dalmine S.p.A. (Tenaris Group).

* Île-de-France Geothermal Expansion: Corporate momentum is building in the Paris region via the 2gré subsidiary, which secured a $169.59 million, 30-year concession to operate a deep district heating network across Clichy-sous-Bois and Livry-Gargan.

HDIN Institutional Perspective

While Arverne Group’s executive board achieved 100% of its financial engineering and ESG compensation targets in 2025, our forensic audit exposes a severe misalignment between capital-raising agility and operational execution. Management secured the $45.22 million LDF Series B2 and up to $169.59 million in C3IV Green Industry Tax Credits, proving Arverne’s utility as a sovereign funding proxy. However, operational management drastically missed its gross business volume targets (scoring only 10.64%). The lag in commercial heat network deployment forces prolonged cash bleed.

Crucially, the institutional thesis rests on the Renault Group offtake agreement (25,000 tonnes of LCE over 5 years). If ongoing community resistance or geomechanical anomalies—such as the induced seismicity that paralyzed the legacy Vendenheim project (carrying a $1.81 million abandonment provision)—delay the Schwabwiller demonstrator scaling, Renault’s strict December 2029 cancellation clause will be triggered. This represents an asymmetric execution risk that current market valuations fail to accurately discount against the required $2.03 billion - $2.15 billion lithium scaling pipeline.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Arverne Group 2025: Decoding the Geothermal-Lithium Nexus

Capital Deployment Architecture & Dilution DiagnosticsArverne Group (Euronext Paris: ARV) is executing a highly capital-intensive transition. While consolidated top-line revenue expanded, the quality of earnings is entirely dependent on legacy B2B drilling contracts. Proprietary infrastructure assets remain in an accelerating cash-burn phase.

Forensic Analysis of 2025 Consolidated Financials:

* Top-Line & Segmental Margins: Total revenue hit $20.31 million. The Drilling & Well Construction division generated $19.13 million (94.2% of total) but operated at near-breakeven EBITDA (-$0.25 million). Proprietary geothermal (2gré) generated merely $0.95 million with a -$2.74 million EBITDA drag, while the pre-revenue Lithium de France (LDF) recorded an -$8.73 million EBITDA loss.

* Operating Leverage & Unit Economics: Through its "dual-valorization" model, baseline heat sales subsidize fixed infrastructure costs. This cross-amortization structurally lowers the Direct Lithium Extraction (DLE) estimated OpEx to below $5,087.70 per tonne of Lithium Carbonate Equivalent (LCE), placing it in the global first quartile.

* Cash Runway & Structuring Frictions: 2025 operating cash flow stood at -$15.66 million against a $43.66 million CapEx spend. While the $88.20 million year-end cash balance provides a 12-month runway, going-concern status hinges on the complex $56.53 million ORANE bridge bond. Carrying a 7% capitalized interest rate, the ORANE triggers automatic equity conversion at a punitive 20% discount if Arverne secures a public market raise.

* Minority Interest & Consolidation: Arverne executed a $25.24 million share swap with Hydro Energy Invest AS (issuing 2.23 million parent shares at $11.31) to increase its LDF stake to 73.83%. However, Equinor’s remaining 26.17% minority stake forces a $20.26 million non-controlling interest liability on the consolidated balance sheet.

Hardware Sovereignty & Upper Rhine Subsurface Footprint

Arverne's physical operations are entirely domestic, heavily concentrated in France to align with the state’s Multi-Year Energy Plan (PPE 3). The company's competitive moat is strictly defined by physical asset ownership and localized supply chain procurement.

* Proprietary Drilling Infrastructure: To bypass critical European rig shortages, Arverne internalizes operations utilizing 4 deep-drilling rigs, including the electric B18 and B04 co-developed with Herrenknecht AG.

* Alsace / Upper Rhine Graben Epicenter: The industrialization of the DLE process is anchored at the Schwabwiller site. The first geothermal doublet commenced drilling in November 2025 and completed its first well by February 2026. A DLE demonstrator, engineered via Pre-FEED/FEED contracts with Technip Energies and Sedgman, targets operational launch at this facility by late 2026.

* Tier-1 Supply Chain Buffer: To mitigate macro-inflationary shocks on $28.27 million-per-project geothermal CapEx profiles, Arverne executed strategic long-lead procurement agreements. This includes a master supply contract with Cameron France S.A.S. (SLB) for wellheads and a 5-year casing supply agreement with Dalmine S.p.A. (Tenaris Group).

* Île-de-France Geothermal Expansion: Corporate momentum is building in the Paris region via the 2gré subsidiary, which secured a $169.59 million, 30-year concession to operate a deep district heating network across Clichy-sous-Bois and Livry-Gargan.

HDIN Institutional Perspective

While Arverne Group’s executive board achieved 100% of its financial engineering and ESG compensation targets in 2025, our forensic audit exposes a severe misalignment between capital-raising agility and operational execution. Management secured the $45.22 million LDF Series B2 and up to $169.59 million in C3IV Green Industry Tax Credits, proving Arverne’s utility as a sovereign funding proxy. However, operational management drastically missed its gross business volume targets (scoring only 10.64%). The lag in commercial heat network deployment forces prolonged cash bleed.

Crucially, the institutional thesis rests on the Renault Group offtake agreement (25,000 tonnes of LCE over 5 years). If ongoing community resistance or geomechanical anomalies—such as the induced seismicity that paralyzed the legacy Vendenheim project (carrying a $1.81 million abandonment provision)—delay the Schwabwiller demonstrator scaling, Renault’s strict December 2029 cancellation clause will be triggered. This represents an asymmetric execution risk that current market valuations fail to accurately discount against the required $2.03 billion - $2.15 billion lithium scaling pipeline.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."