Seven & i Holdings: Radical Pure-Play Convenience Restructuring Across North America and Japan as $3.60 Billion Net Asset Liquidation Subsidizes Capital Returns

Date : 2026-05-22

Reading : 219

Seven & i Holdings' FY2026 disclosures reveal a ruthless structural simplification, shedding legacy superstore and financial segments to insulate against hostile takeovers via a pure-play global convenience strategy. For institutional LPs, the focal point is the ¥600 billion ($4.01 billion) share buyback tranche. Crucially, this is not supported by the company’s ¥150.8 billion organic FCF. Instead, it is heavily subsidized by $3.60 billion in net proceeds from the York Holdings divestiture to Bain Capital, masking underlying liquidity friction as North American fuel margins face structural macroeconomic compression.

Figure Seven & i Holdings 2025: The Pure-Play Global CVS Transformation

Forensic Analysis of Transitional Financials & Segmental Bifurcation

Forensic Analysis of Transitional Financials & Segmental Bifurcation

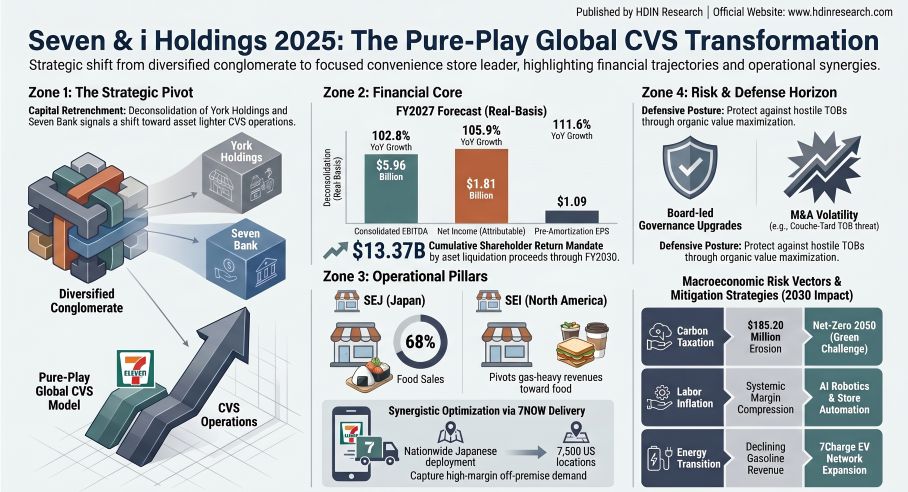

The FY2026 reporting period marks a definitive inflection point, characterized by massive boundary changes following the deconsolidation of the Superstore (SST) and Financial segments. The corporate balance sheet is actively draining accumulated cash reserves (contracting from ¥1,349,820 million to ¥426,146 million) to engineer a ¥2.0 trillion ($13.37 billion) cumulative shareholder return policy through FY2030.

A forensic audit of unit economics reveals a highly bifurcated segmental margin profile:

* Consolidated Group Baseline (FY2026): Total Group Sales reached ¥16,992,087 million ($113.61 billion), representing a YoY decline to 92.1% due to structural exits. Consolidated Net Income surged to ¥292,760 million ($1.96 billion) or 169.2% YoY, artificially inflated by the absence of prior-year overseas closure impairments and a ¥26,946 million extraordinary gain from the SST split.

* Domestic CVS (Seven-Eleven Japan - SEJ): The high-margin, merchandise-centric engine. Total chain sales registered at ¥5,469,315 million ($36.57 billion). Operations exhibit superior incremental margins driven by a 68.0% food category dominance (Processed 27.3%, Fast 28.5%, Daily 12.2%). Capital allocation is strictly disciplined, with ¥114,499 million ($765.5 million) in CapEx routed toward fresh food infrastructure, including the rollout of "Seven Cafe Bakery" to 18,000 stores and "Seven Cafe Tea" to 10,000 stores by FY2026.

* Overseas CVS (7-Eleven, Inc. - SEI): The volume-heavy, margin-dilutive segment. Total chain sales hit ¥9,725,461 million ($65.02 billion), but revenues remain perilously tethered to volatile gasoline sales (58.9% or $38.31 billion). Merchandise accounts for only 41.1%. The retirement of former SEI CEO Joe DePinto triggered a ¥5,635 million ($37.67 million) severance, recognizing a ¥2,977 million ($19.90 million) extraordinary loss.

* FY2027 Forward Guidance (Real-Basis): Stripped of legacy assets, management forecasts Group CVS Sales of ¥10.03 trillion ($67.06 billion), Consolidated Operating Income of ¥405 billion ($2.71 billion), and Consolidated EBITDA of ¥891 billion ($5.96 billion), targeting a High-Teens% Adjusted EPS growth.

Supply Chain Audit & Geo-Economic Moat Vulnerabilities

Seven & i Holdings is aggressively restructuring its physical footprint to mitigate severe macroeconomic friction, specifically US inflation, Japanese demographic labor shortages, and global decarbonization mandates.

* Geographic Footprint & Expansion: Growth is anchored in North America (Texas, Delaware, Hawaii) and Asia (Okinawa, Japan; Beijing, Tianjin, Chengdu, Shandong in China), with Oceania integration accelerating via the Victoria, Australia-based Convenience Group Holdings Pty Ltd. Europe is explicitly identified as the "4th pillar of growth" via equity-based expansion models under 7-Eleven International LLC (7IN).

* Technological CapEx & Labor Substitution: To counter wage inflation, SEJ is transferring the franchisee OPEX burden to corporate CapEx. The deployment of AI-equipped stocking robots and employee monitoring systems aims to structurally reduce store-level headcount. Concurrently, the 7NOW delivery network is scaling aggressively, currently operating across 7,500 US locations to capture off-premise digital demand.

* Energy Transition & Carbon Liability Risk: The heavy reliance on high-frequency, temperature-controlled logistics exposes the supply chain to severe physical climate risks. Scope 3 emissions currently sit at a massive 170,923,000 t-CO2. Management's TCFD scenario analysis projects that without aggressive mitigation, global carbon pricing ($135/ton) will erode consolidated profits by ¥27.7 billion ($185.20 million) annually by 2030. To hedge this and declining fuel revenues, SEI is scaling the 7Charge EV fast-charging network while SEJ executes off-site Power Purchase Agreements (PPAs) and store-level solar deployments.

HDIN Institutional Perspective: The "Food Convenience" Execution Deficit

While the FY2026 Annual Report positions the "7-Eleven Transformation" as an airtight defense against hostile M&A, the execution roadmap is fraught with operational dissonance. The Board’s strict performance share unit (PSU) KPIs—tying executive compensation equally to ROIC and Relative Total Shareholder Return (TSR)—force extreme capital discipline.

However, our differentiated viewpoint challenges the sustainability of this model. The corporate balance sheet currently internalizes ¥1,398,990 million ($9.35 billion) in lease obligations to shield franchisees, while holding ¥2,109,806 million ($14.11 billion) in goodwill from North American acquisitions. With organic Free Cash Flow (FCF) covering less than 26% of the recent share buybacks, the company's capital return architecture is dangerously reliant on structural asset liquidations rather than operational cash generation. If the integration of the 1,000 restaurant-integrated US stores fails to seamlessly adapt the Japanese "Tanpin-Kanri" (item-by-item management) methodology, the resulting M&A frictions and subsequent goodwill impairment will instantly vaporize the projected FY2027 $5.96 billion EBITDA target.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Seven & i Holdings 2025: The Pure-Play Global CVS Transformation

Forensic Analysis of Transitional Financials & Segmental BifurcationThe FY2026 reporting period marks a definitive inflection point, characterized by massive boundary changes following the deconsolidation of the Superstore (SST) and Financial segments. The corporate balance sheet is actively draining accumulated cash reserves (contracting from ¥1,349,820 million to ¥426,146 million) to engineer a ¥2.0 trillion ($13.37 billion) cumulative shareholder return policy through FY2030.

A forensic audit of unit economics reveals a highly bifurcated segmental margin profile:

* Consolidated Group Baseline (FY2026): Total Group Sales reached ¥16,992,087 million ($113.61 billion), representing a YoY decline to 92.1% due to structural exits. Consolidated Net Income surged to ¥292,760 million ($1.96 billion) or 169.2% YoY, artificially inflated by the absence of prior-year overseas closure impairments and a ¥26,946 million extraordinary gain from the SST split.

* Domestic CVS (Seven-Eleven Japan - SEJ): The high-margin, merchandise-centric engine. Total chain sales registered at ¥5,469,315 million ($36.57 billion). Operations exhibit superior incremental margins driven by a 68.0% food category dominance (Processed 27.3%, Fast 28.5%, Daily 12.2%). Capital allocation is strictly disciplined, with ¥114,499 million ($765.5 million) in CapEx routed toward fresh food infrastructure, including the rollout of "Seven Cafe Bakery" to 18,000 stores and "Seven Cafe Tea" to 10,000 stores by FY2026.

* Overseas CVS (7-Eleven, Inc. - SEI): The volume-heavy, margin-dilutive segment. Total chain sales hit ¥9,725,461 million ($65.02 billion), but revenues remain perilously tethered to volatile gasoline sales (58.9% or $38.31 billion). Merchandise accounts for only 41.1%. The retirement of former SEI CEO Joe DePinto triggered a ¥5,635 million ($37.67 million) severance, recognizing a ¥2,977 million ($19.90 million) extraordinary loss.

* FY2027 Forward Guidance (Real-Basis): Stripped of legacy assets, management forecasts Group CVS Sales of ¥10.03 trillion ($67.06 billion), Consolidated Operating Income of ¥405 billion ($2.71 billion), and Consolidated EBITDA of ¥891 billion ($5.96 billion), targeting a High-Teens% Adjusted EPS growth.

Supply Chain Audit & Geo-Economic Moat Vulnerabilities

Seven & i Holdings is aggressively restructuring its physical footprint to mitigate severe macroeconomic friction, specifically US inflation, Japanese demographic labor shortages, and global decarbonization mandates.

* Geographic Footprint & Expansion: Growth is anchored in North America (Texas, Delaware, Hawaii) and Asia (Okinawa, Japan; Beijing, Tianjin, Chengdu, Shandong in China), with Oceania integration accelerating via the Victoria, Australia-based Convenience Group Holdings Pty Ltd. Europe is explicitly identified as the "4th pillar of growth" via equity-based expansion models under 7-Eleven International LLC (7IN).

* Technological CapEx & Labor Substitution: To counter wage inflation, SEJ is transferring the franchisee OPEX burden to corporate CapEx. The deployment of AI-equipped stocking robots and employee monitoring systems aims to structurally reduce store-level headcount. Concurrently, the 7NOW delivery network is scaling aggressively, currently operating across 7,500 US locations to capture off-premise digital demand.

* Energy Transition & Carbon Liability Risk: The heavy reliance on high-frequency, temperature-controlled logistics exposes the supply chain to severe physical climate risks. Scope 3 emissions currently sit at a massive 170,923,000 t-CO2. Management's TCFD scenario analysis projects that without aggressive mitigation, global carbon pricing ($135/ton) will erode consolidated profits by ¥27.7 billion ($185.20 million) annually by 2030. To hedge this and declining fuel revenues, SEI is scaling the 7Charge EV fast-charging network while SEJ executes off-site Power Purchase Agreements (PPAs) and store-level solar deployments.

HDIN Institutional Perspective: The "Food Convenience" Execution Deficit

While the FY2026 Annual Report positions the "7-Eleven Transformation" as an airtight defense against hostile M&A, the execution roadmap is fraught with operational dissonance. The Board’s strict performance share unit (PSU) KPIs—tying executive compensation equally to ROIC and Relative Total Shareholder Return (TSR)—force extreme capital discipline.

However, our differentiated viewpoint challenges the sustainability of this model. The corporate balance sheet currently internalizes ¥1,398,990 million ($9.35 billion) in lease obligations to shield franchisees, while holding ¥2,109,806 million ($14.11 billion) in goodwill from North American acquisitions. With organic Free Cash Flow (FCF) covering less than 26% of the recent share buybacks, the company's capital return architecture is dangerously reliant on structural asset liquidations rather than operational cash generation. If the integration of the 1,000 restaurant-integrated US stores fails to seamlessly adapt the Japanese "Tanpin-Kanri" (item-by-item management) methodology, the resulting M&A frictions and subsequent goodwill impairment will instantly vaporize the projected FY2027 $5.96 billion EBITDA target.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."