Deep Robotics: $348 Million STAR Market Pivot Near Hangzhou as 52.83% Gross Margin Signals Breakeven in Industrial Embodied AI

Date : 2026-05-22

Reading : 110

By reallocating 100% of its proposed $348.18 million IPO proceeds away from global marketing and into hardware/AI engineering in Hangzhou, Deep Robotics is structurally insulating its B2B industrial market share from Tesla (NASDAQ: TSLA) and Figure AI. Institutional LPs should note that while the firm monopolizes China’s State Grid quadruped deployments, its post-IPO voting power dilution (25.46%) and rapid Work-in-Progress (WIP) inventory impairments signal a highly capital-intensive transition toward end-to-end Vision-Language-Action (VLA) models. The immediate financial profile is authentic, but the long-term AI-convergence risk remains unpriced.

Figure Deep Robotics (Yunshenchu): The B2B Embodied Al Strategic Roadmap & IPO Analysis

Forensic Financials & Segmental Inventory: The 52.83% Margin Inflection

Forensic Financials & Segmental Inventory: The 52.83% Margin Inflection

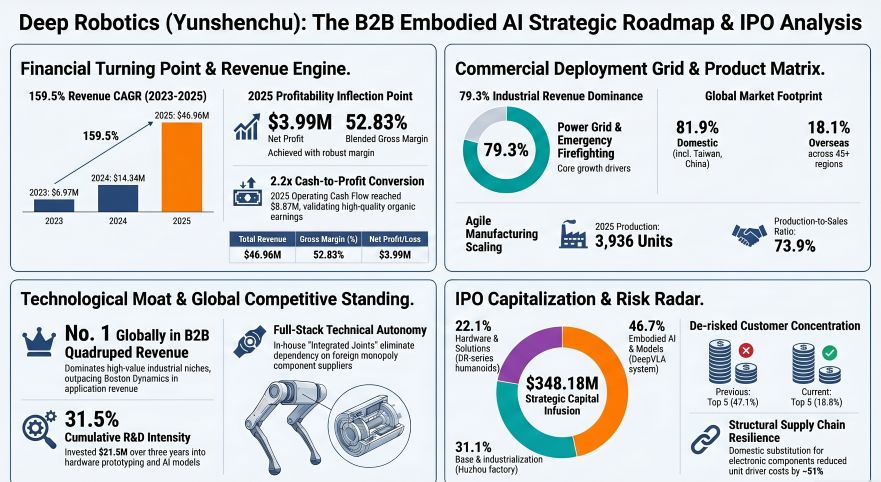

A forensic analysis of the Deep Robotics STAR Market prospectus reveals a high-quality, organically generated profit turnaround. The firm has actively avoided R&D capitalization and policy-dependent "blood transfusions," deriving its earnings fundamentally from high-margin B2B hardware scale. In 2025, pure market mechanics—driven by volume expansion from 896 to 2,908 units—pushed the blended gross margin to 52.83%, overpowering a massive ~$11.73 million R&D expense.

Quantitative Inventory & Operating Leverage Ledger

* Top-Line & Core Earnings: 2025 total revenue reached ~$46.96 million. Stripping away non-recurring items (a 4.15% net profit weight for ~$165.58k in government subsidies, ~$16.27k in VAT refunds, and ~$57.44k in fair-value wealth management gains), the core operational net profit organically inflected from a -$3.97 million loss in 2023 and -$3.37 million in 2024 to a +$2.10 million profit in 2025. Total reported 2025 net profit was ~$3.99 million.

* Capital Allocation (IPO): The ~$348.18 million raise is allocated strictly to structural bottlenecks: 46.72% (~$162.68M) to Embodied Algorithm & Model R&D (DeepVLA), 22.14% (~$77.09M) to Hardware & Solution R&D, 22.07% (~$76.84M) to Base Construction, and 9.07% (~$31.56M) to Industrialization.

* Asset Quality & R&D Fidelity: The company enforces a 0% R&D capitalization rate. The ~$21.52 million cumulative 3-year R&D spend (31.52% of revenue) is 100% expensed. Intangible assets rest at a trivial ~$0.10 million (~$0.08M software, ~$0.02M patent fees). R&D material inputs consume 25.53% to 30.76% of the R&D budget (~$3.24M in 2025), validating capital-intensive prototyping for the Shanmao M-series and DR-series humanoids.

* Inventory Obsolescence Protocol: Total inventory sits at ~$18.27 million with a blended 5.28% impairment (~$0.96M). However, Work-in-Progress (WIP) carries an aggressive 19.98% markdown on a ~$2.34 million balance, neutralizing mid-iteration obsolescence, while finished goods ($4.25M) carry a 0.46% provision. Inventory turnover accelerated from 1.23x in 2023 to 1.79x in 2025.

* Receivables & Liquidity: The ~$5.91 million AR balance is highly secure; 85.74% is aged under one year, backed primarily by State-Owned Enterprises (SOEs). The Expected Credit Loss (ECL) matrix enforces a rigid 9.70% (~$0.57M) blended bad debt provision (5% at <1 year, 100% at >3 years).

* Related-Party Hygiene: Transactions are immaterial. 2024 sales to former associate Anyun Zhi Neng were ~$4,459, fully reversed in 2025 (-$4,161). The founder provided a ~$1.046M liquidity bridge and a temporary ~$278k loan at standard bank deposit rates (generating just ~$5,407 in interest), while the firm paid a trivial ~$43 in ESOP platform banking fees. Executive remuneration scaled rationally ($32,267 in 2023, $38,800 in 2024, $61,978 in 2025).

Supply Chain Audit & Geo-Economic Moat: Hangzhou-Based Ecosystems

Unlike Unitree, which captures 70% of its revenue from consumer and educational volume, Deep Robotics bypassed the price war, generating ~80% of revenue from B2B industrial niches. The firm utilizes a "Direct Sales-led, Integrator-heavy" architecture, where integrators/trading companies generate 63.98% of total revenue, buffering direct dependency and accelerating grid penetration.

* Supplier Decentralization & Domestic Substitution: The upstream ecosystem is insulated from US/EU export embargoes. By developing proprietary Integrated Joints (motor, reducer, driver), the firm eliminated reliance on foreign monopolies (e.g., Harmonic Drive). Consequently, the procurement unit price of drivers collapsed by -51.22% in 2024 and -27.57% in 2025. Top 5 supplier concentration dropped to 29.89% (~$10.43M) in 2025: Suzhou Shengyuyuan (10.43%), Shaanxi Jiushihechuang (5.73%), Hangzhou Guiling (5.47%), Beijing BDStar Navigation (4.18%), and Kunshan Jingyue (4.08%).

* Customer Dilution & Market Share: Customer concentration plummeted from 47.12% in 2024 (where State Grid held 6.56%) to a highly de-risked 18.83% in 2025. The 2025 Top 5 roster reflects fragmented horizontal scaling: Customer A (9.07%, ~$4.26M), Sichuan Embodied Humanoid Robot (2.66%), Customer C (2.60%), Suzhou Naoqi (2.39%), and Germany's Inmotion Robotic GmbH (2.11%).

* Governance & Talent Architecture: The board heavily leverages the Zhejiang University (ZJU) academic nexus. While structurally mitigating IP friction—despite absorbing key personnel from Hangzhou Nanjiang Robotics—the capitalization table is fragmented. Founder Zhu Qiuguo's pre-IPO voting block (31.05%) will dilute to a fragile 25.46% post-IPO (Zhu 12.80% + Hangzhou Kongjian 8.39% + CTO Li Chao 4.27%). To defend the stock, the ESOP platform (Kongjian, $205,134 capital, $1.007M in 2025 share-based expenses) operates under a draconian 36-month lock-up, extending up to 54 months if net profit drops >50% annually. The firm resolved historical LLC procedural flaws and indemnified a minor 4-person social security non-compliance issue.

HDIN Institutional Perspective: The Critical Edge

While the S-1 claims a dominant trajectory in "Embodied AI" and touts its No. 1 global ranking in industrial quadrupeds over Boston Dynamics, the immediate economic moat relies entirely on classical robotics engineering—specifically Model Predictive Control (MPC) and Whole Body Control (WBC) for the Jueying X30 in IP67/extreme temperature (-20 to 55°C) environments.

Our differentiated viewpoint is that Deep Robotics currently operates as a highly successful hardware integrator, not an AI foundation model company. Its genuine AI capabilities (e.g., DeepVLA1.0) remain in pilot phases. The ~$162.68 million injection into algorithm R&D is a defensive necessity against a 3-year structural vulnerability. If the sector pivots definitively to end-to-end neural network control (the "World Model" approach pioneered by well-capitalized U.S. giants), Deep Robotics' historical MPC/WBC algorithmic moats will face rapid obsolescence. Furthermore, the DR-series humanoid pipeline remains embryonic, recording merely 3 units sold in 2024 (~$117.11k) and 1 unit in 2025 (~$82.30k). The street has priced in the state-backed hardware grid deployment, but has yet to factor in the massive compute-cluster CAPEX required to compete globally in foundational VLA models.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Deep Robotics (Yunshenchu): The B2B Embodied Al Strategic Roadmap & IPO Analysis

Forensic Financials & Segmental Inventory: The 52.83% Margin InflectionA forensic analysis of the Deep Robotics STAR Market prospectus reveals a high-quality, organically generated profit turnaround. The firm has actively avoided R&D capitalization and policy-dependent "blood transfusions," deriving its earnings fundamentally from high-margin B2B hardware scale. In 2025, pure market mechanics—driven by volume expansion from 896 to 2,908 units—pushed the blended gross margin to 52.83%, overpowering a massive ~$11.73 million R&D expense.

Quantitative Inventory & Operating Leverage Ledger

* Top-Line & Core Earnings: 2025 total revenue reached ~$46.96 million. Stripping away non-recurring items (a 4.15% net profit weight for ~$165.58k in government subsidies, ~$16.27k in VAT refunds, and ~$57.44k in fair-value wealth management gains), the core operational net profit organically inflected from a -$3.97 million loss in 2023 and -$3.37 million in 2024 to a +$2.10 million profit in 2025. Total reported 2025 net profit was ~$3.99 million.

* Capital Allocation (IPO): The ~$348.18 million raise is allocated strictly to structural bottlenecks: 46.72% (~$162.68M) to Embodied Algorithm & Model R&D (DeepVLA), 22.14% (~$77.09M) to Hardware & Solution R&D, 22.07% (~$76.84M) to Base Construction, and 9.07% (~$31.56M) to Industrialization.

* Asset Quality & R&D Fidelity: The company enforces a 0% R&D capitalization rate. The ~$21.52 million cumulative 3-year R&D spend (31.52% of revenue) is 100% expensed. Intangible assets rest at a trivial ~$0.10 million (~$0.08M software, ~$0.02M patent fees). R&D material inputs consume 25.53% to 30.76% of the R&D budget (~$3.24M in 2025), validating capital-intensive prototyping for the Shanmao M-series and DR-series humanoids.

* Inventory Obsolescence Protocol: Total inventory sits at ~$18.27 million with a blended 5.28% impairment (~$0.96M). However, Work-in-Progress (WIP) carries an aggressive 19.98% markdown on a ~$2.34 million balance, neutralizing mid-iteration obsolescence, while finished goods ($4.25M) carry a 0.46% provision. Inventory turnover accelerated from 1.23x in 2023 to 1.79x in 2025.

* Receivables & Liquidity: The ~$5.91 million AR balance is highly secure; 85.74% is aged under one year, backed primarily by State-Owned Enterprises (SOEs). The Expected Credit Loss (ECL) matrix enforces a rigid 9.70% (~$0.57M) blended bad debt provision (5% at <1 year, 100% at >3 years).

* Related-Party Hygiene: Transactions are immaterial. 2024 sales to former associate Anyun Zhi Neng were ~$4,459, fully reversed in 2025 (-$4,161). The founder provided a ~$1.046M liquidity bridge and a temporary ~$278k loan at standard bank deposit rates (generating just ~$5,407 in interest), while the firm paid a trivial ~$43 in ESOP platform banking fees. Executive remuneration scaled rationally ($32,267 in 2023, $38,800 in 2024, $61,978 in 2025).

Supply Chain Audit & Geo-Economic Moat: Hangzhou-Based Ecosystems

Unlike Unitree, which captures 70% of its revenue from consumer and educational volume, Deep Robotics bypassed the price war, generating ~80% of revenue from B2B industrial niches. The firm utilizes a "Direct Sales-led, Integrator-heavy" architecture, where integrators/trading companies generate 63.98% of total revenue, buffering direct dependency and accelerating grid penetration.

* Supplier Decentralization & Domestic Substitution: The upstream ecosystem is insulated from US/EU export embargoes. By developing proprietary Integrated Joints (motor, reducer, driver), the firm eliminated reliance on foreign monopolies (e.g., Harmonic Drive). Consequently, the procurement unit price of drivers collapsed by -51.22% in 2024 and -27.57% in 2025. Top 5 supplier concentration dropped to 29.89% (~$10.43M) in 2025: Suzhou Shengyuyuan (10.43%), Shaanxi Jiushihechuang (5.73%), Hangzhou Guiling (5.47%), Beijing BDStar Navigation (4.18%), and Kunshan Jingyue (4.08%).

* Customer Dilution & Market Share: Customer concentration plummeted from 47.12% in 2024 (where State Grid held 6.56%) to a highly de-risked 18.83% in 2025. The 2025 Top 5 roster reflects fragmented horizontal scaling: Customer A (9.07%, ~$4.26M), Sichuan Embodied Humanoid Robot (2.66%), Customer C (2.60%), Suzhou Naoqi (2.39%), and Germany's Inmotion Robotic GmbH (2.11%).

* Governance & Talent Architecture: The board heavily leverages the Zhejiang University (ZJU) academic nexus. While structurally mitigating IP friction—despite absorbing key personnel from Hangzhou Nanjiang Robotics—the capitalization table is fragmented. Founder Zhu Qiuguo's pre-IPO voting block (31.05%) will dilute to a fragile 25.46% post-IPO (Zhu 12.80% + Hangzhou Kongjian 8.39% + CTO Li Chao 4.27%). To defend the stock, the ESOP platform (Kongjian, $205,134 capital, $1.007M in 2025 share-based expenses) operates under a draconian 36-month lock-up, extending up to 54 months if net profit drops >50% annually. The firm resolved historical LLC procedural flaws and indemnified a minor 4-person social security non-compliance issue.

HDIN Institutional Perspective: The Critical Edge

While the S-1 claims a dominant trajectory in "Embodied AI" and touts its No. 1 global ranking in industrial quadrupeds over Boston Dynamics, the immediate economic moat relies entirely on classical robotics engineering—specifically Model Predictive Control (MPC) and Whole Body Control (WBC) for the Jueying X30 in IP67/extreme temperature (-20 to 55°C) environments.

Our differentiated viewpoint is that Deep Robotics currently operates as a highly successful hardware integrator, not an AI foundation model company. Its genuine AI capabilities (e.g., DeepVLA1.0) remain in pilot phases. The ~$162.68 million injection into algorithm R&D is a defensive necessity against a 3-year structural vulnerability. If the sector pivots definitively to end-to-end neural network control (the "World Model" approach pioneered by well-capitalized U.S. giants), Deep Robotics' historical MPC/WBC algorithmic moats will face rapid obsolescence. Furthermore, the DR-series humanoid pipeline remains embryonic, recording merely 3 units sold in 2024 (~$117.11k) and 1 unit in 2025 (~$82.30k). The street has priced in the state-backed hardware grid deployment, but has yet to factor in the massive compute-cluster CAPEX required to compete globally in foundational VLA models.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."