Silicon Intelligence: Autopilot Pivot Near Nanjing Headquarters Signals Structural Margin Expansion Amid Severe Working Capital Drag

Date : 2026-05-25

Reading : 113

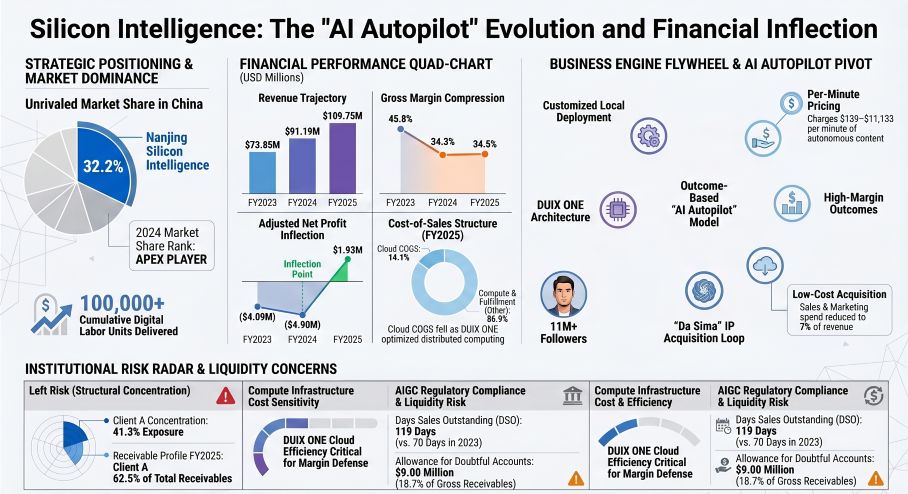

Silicon Intelligence’s transition to a positive USD $1.93 million adjusted net profit in FY2025 validates its pivot from SaaS tool licensing to an outcome-oriented "AI Autopilot" model. While the Nanjing-headquartered firm commands a 32.2% domestic market share, its structural reliance on customized local deployments for state-owned telecom operators has stretched its Cash Conversion Cycle to 85 days. For institutional LPs, the critical metric is whether the high-margin, fully automated content generation segment can scale rapidly enough to offset the severe working capital drag caused by extreme client concentration.

Figure Silicon Intelligence: The Al Autopilot Evolution and Financial Inflection

Forensic Financials & Segmental Inventory of Silicon Intelligence

Forensic Financials & Segmental Inventory of Silicon Intelligence

A Forensic Analysis of the firm’s FY2023–FY2025 track record reveals a highly deliberate price-mix variance strategy: sacrificing legacy product margins to capture market share, while absorbing fixed R&D costs to drive operating leverage through a newly introduced premium segment.

Quantitative Inventory & Margin Dynamics:

* Top-Line & Core Margins: Revenue expanded at a 21.9% CAGR, reaching USD $109.75M in FY2025. However, gross margins compressed from 45.8% (FY2023) to 34.5% (FY2025) due to proactive price reductions on early-version products and a shift toward capital-intensive customized deployments.

* Segmental Incremental Margins: The newly launched "Auto Content Generation" (AI Autopilot) generated USD $7.15M within five months of its August 2025 launch. By charging USD $139 to $11,133 per minute of generated content, this segment commands a superior 54.9% gross margin, structurally divorcing revenue from traditional SaaS seat-license caps.

* Internal Capital Allocation: R&D remains 100% expensed directly to the P&L, totaling USD $22.73M (20.7% of revenue) in FY2025 with zero capitalization. Sales & Marketing (S&M) expenditure structurally compressed from 20.8% of revenue in 2023 to 7.0% (USD $7.69M) in 2025, lowering Customer Acquisition Cost (CAC) to USD $15.4k.

* Valuation & Capital Structure: The pre-IPO trajectory peaked at a USD $438.26M valuation (Round D, May 2025). Critically, the firm extinguished USD $134.5M in venture-debt redemption liabilities (Put Options) in November 2024, cleansing the balance sheet of non-cash accretion charges that previously inflated statutory net losses.

Supply Chain Audit & Geo-Economic Moat

The physicality of Silicon Intelligence’s business highlights a dual-track dependency on highly secure, localized deployment zones and constrained external hardware infrastructure.

* Geographic Footprint: Operations are anchored at the global headquarters in Nanjing, Jiangsu Province, with specialized regional subsidiaries executing domestic deliveries across Shanghai, Shenzhen, Kunshan, Mianyang, Suqian, Yuxi, and Jiaxing. International pilot initiatives are currently stationed in Singapore and Hong Kong SAR, focusing on localized e-commerce and digital immortality services.

* Infrastructure & Supply Chain Vulnerabilities: The firm remains exposed to US export controls (EAR). Public cloud hosting relies partially on "Supplier A" (representing USD $3.74M in FY2025 procurement), an entity currently listed on the US BIS Entity List. Furthermore, internal algorithmic training for the proprietary Yan Di LLM relied on historical procurement of US-origin GPUs (Models A, B, and C) sourced domestically via "Supplier Y".

* Edge-Computing Margin Defense: To defend against rising third-party cloud computing taxes, the company optimized its proprietary DUIX ONE multimodal engine to process tasks on end-user devices. This architectural pivot successfully collapsed Cloud Infrastructure Costs from 38.4% of COGS in 2023 down to 14.1% in FY2025. However, Project Fulfillment Costs (manual integration and debugging for massive SOE networks) surged to 77.0% of total COGS.

HDIN Institutional Perspective

While the prospectus frames the 21.9% revenue CAGR and the FY2025 USD $1.93M adjusted profit as a fundamental breakout, the underlying Cash Conversion Cycle (CCC) indicates a structurally cash-consumptive operation that the Street has not fully priced in.

Our differentiated viewpoint confirms that Silicon Intelligence is acting as a massive unsecured creditor for its largest counterparty. "Client A" (a major state-owned telecom operator) accounted for 41.3% of 2025 revenue but dominates 62.5% of total trade receivables. Consequently, Days Sales Outstanding (DSO) surged to 119 days, driving an operational cash outflow of USD $17.03M in FY2025. Furthermore, allowing USD $11.12M of Client A’s receivables to age beyond 365 days (forcing a USD $5.75M ECL provision) demonstrates that the firm is effectively financing SOE digital infrastructure at a zero percent interest rate.

Additionally, investors must closely monitor the impending *Interim Measures for AI Humanoid Interactive Services* (effective July 2026) and the *AI Sci-Tech Ethics Review Measures* (effective March 2026). While the firm has completed its baseline CAC algorithm filings, these 2026 regulatory hurdles will drastically increase compliance OPEX for any future B2C emotional-care integrations. The true viability of this equity hinges entirely on whether the high-margin "AI Autopilot" segment can scale rapidly enough to bypass the capital-intensive integrator bottlenecks.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Silicon Intelligence: The Al Autopilot Evolution and Financial Inflection

Forensic Financials & Segmental Inventory of Silicon IntelligenceA Forensic Analysis of the firm’s FY2023–FY2025 track record reveals a highly deliberate price-mix variance strategy: sacrificing legacy product margins to capture market share, while absorbing fixed R&D costs to drive operating leverage through a newly introduced premium segment.

Quantitative Inventory & Margin Dynamics:

* Top-Line & Core Margins: Revenue expanded at a 21.9% CAGR, reaching USD $109.75M in FY2025. However, gross margins compressed from 45.8% (FY2023) to 34.5% (FY2025) due to proactive price reductions on early-version products and a shift toward capital-intensive customized deployments.

* Segmental Incremental Margins: The newly launched "Auto Content Generation" (AI Autopilot) generated USD $7.15M within five months of its August 2025 launch. By charging USD $139 to $11,133 per minute of generated content, this segment commands a superior 54.9% gross margin, structurally divorcing revenue from traditional SaaS seat-license caps.

* Internal Capital Allocation: R&D remains 100% expensed directly to the P&L, totaling USD $22.73M (20.7% of revenue) in FY2025 with zero capitalization. Sales & Marketing (S&M) expenditure structurally compressed from 20.8% of revenue in 2023 to 7.0% (USD $7.69M) in 2025, lowering Customer Acquisition Cost (CAC) to USD $15.4k.

* Valuation & Capital Structure: The pre-IPO trajectory peaked at a USD $438.26M valuation (Round D, May 2025). Critically, the firm extinguished USD $134.5M in venture-debt redemption liabilities (Put Options) in November 2024, cleansing the balance sheet of non-cash accretion charges that previously inflated statutory net losses.

Supply Chain Audit & Geo-Economic Moat

The physicality of Silicon Intelligence’s business highlights a dual-track dependency on highly secure, localized deployment zones and constrained external hardware infrastructure.

* Geographic Footprint: Operations are anchored at the global headquarters in Nanjing, Jiangsu Province, with specialized regional subsidiaries executing domestic deliveries across Shanghai, Shenzhen, Kunshan, Mianyang, Suqian, Yuxi, and Jiaxing. International pilot initiatives are currently stationed in Singapore and Hong Kong SAR, focusing on localized e-commerce and digital immortality services.

* Infrastructure & Supply Chain Vulnerabilities: The firm remains exposed to US export controls (EAR). Public cloud hosting relies partially on "Supplier A" (representing USD $3.74M in FY2025 procurement), an entity currently listed on the US BIS Entity List. Furthermore, internal algorithmic training for the proprietary Yan Di LLM relied on historical procurement of US-origin GPUs (Models A, B, and C) sourced domestically via "Supplier Y".

* Edge-Computing Margin Defense: To defend against rising third-party cloud computing taxes, the company optimized its proprietary DUIX ONE multimodal engine to process tasks on end-user devices. This architectural pivot successfully collapsed Cloud Infrastructure Costs from 38.4% of COGS in 2023 down to 14.1% in FY2025. However, Project Fulfillment Costs (manual integration and debugging for massive SOE networks) surged to 77.0% of total COGS.

HDIN Institutional Perspective

While the prospectus frames the 21.9% revenue CAGR and the FY2025 USD $1.93M adjusted profit as a fundamental breakout, the underlying Cash Conversion Cycle (CCC) indicates a structurally cash-consumptive operation that the Street has not fully priced in.

Our differentiated viewpoint confirms that Silicon Intelligence is acting as a massive unsecured creditor for its largest counterparty. "Client A" (a major state-owned telecom operator) accounted for 41.3% of 2025 revenue but dominates 62.5% of total trade receivables. Consequently, Days Sales Outstanding (DSO) surged to 119 days, driving an operational cash outflow of USD $17.03M in FY2025. Furthermore, allowing USD $11.12M of Client A’s receivables to age beyond 365 days (forcing a USD $5.75M ECL provision) demonstrates that the firm is effectively financing SOE digital infrastructure at a zero percent interest rate.

Additionally, investors must closely monitor the impending *Interim Measures for AI Humanoid Interactive Services* (effective July 2026) and the *AI Sci-Tech Ethics Review Measures* (effective March 2026). While the firm has completed its baseline CAC algorithm filings, these 2026 regulatory hurdles will drastically increase compliance OPEX for any future B2C emotional-care integrations. The true viability of this equity hinges entirely on whether the high-margin "AI Autopilot" segment can scale rapidly enough to bypass the capital-intensive integrator bottlenecks.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."