OXIDE: Strategic Deconsolidation and Operations Pivot in Yamanashi Prefecture as +$14.46 Million FCF Signals Structural Margin Inflection

Date : 2026-05-25

Reading : 107

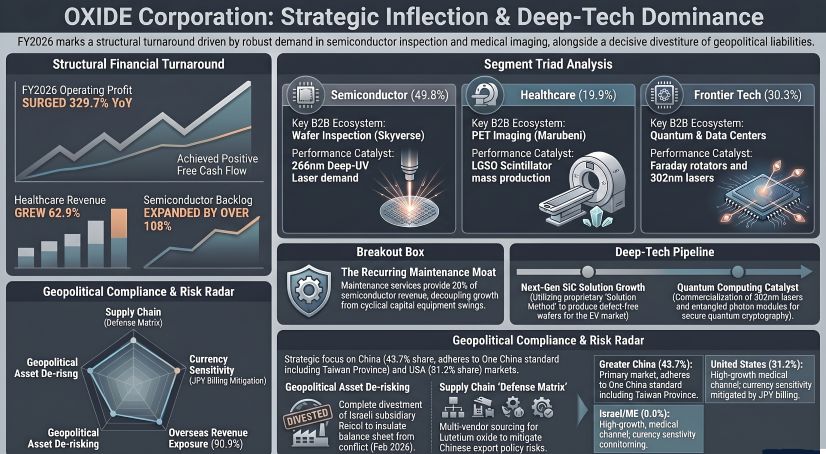

OXIDE’s FY2026 structural pivot highlights a ruthless prioritization of internal capital efficiency. By executing an $11.86 million "stop-loss" divestiture of its Israeli subsidiary, management successfully insulated the consolidated balance sheet from compounding Middle East geopolitical volatility. This deconsolidation masks a profound operational recovery: the core optical business—anchored heavily in its Hokuto City manufacturing hubs—reversed legacy cash burns into highly accretive +$14.46 million free cash flow. For institutional LPs, OXIDE's transition from aggressive capacity-building to FCF harvesting presents a compelling inflection point within the oligopolistic optoelectronics supply chain.

Figure OXIDE Corporation: Strategic Inflection & Deep-Tech Dominance

Segmental Leverage and Working Capital Optimization

Segmental Leverage and Working Capital Optimization

A Forensic Analysis of the FY2026 reporting reveals a company aggressively unwinding balance sheet bloat while achieving peak operational leverage. Despite facing raw material inflationary pressures that compressed Gross Margins to 33.6% (from 38.8% in FY2025), sheer volume growth and SG&A reductions expanded Operating Margins by 3.9 percentage points to 5.4%.

* Top-Line Acceleration: Consolidated revenue surged +19.6% YoY to $67.13 million. The Semiconductor Segment remains the cash cow at $33.44 million (+6.3% YoY), capturing nearly 50% of total revenue.

* The Healthcare Inflection: Healthcare segment revenue exploded by +62.9% YoY to $13.35 million. Critically, the segment's order backlog recorded an anomalous +36,759.7% YoY growth to $4.91 million, confirming a structural transition from prototyping to full-scale commercialization for global PET scanner OEMs.

* Working Capital Efficiency: OXIDE demonstrated flawless cash conversion. While revenues expanded, Accounts Receivable (AR) contracted by 28.2% to $8.56 million with an absolute zero ($0.00) bad debt allowance. Concurrently, total inventory was slashed by 31.0% to $18.93 million, liquidating $2.92 million of finished goods without incurring the prior year's $2.44 million defect disposal losses.

* Free Cash Flow Transition: The enterprise flipped a -$4.41 million FY2025 burn into a +$14.46 million FCF surplus in FY2026. With CapEx commitments narrowing by 61.0% to $4.33 million and trailing non-cash depreciation climbing to $5.91 million, the heavy investment cycle has effectively concluded.

Physical Footprint and Client Concentration Risks

OXIDE’s operational physicality is deliberately concentrated to protect proprietary "black-box" material science. All core crystal growth operations, alongside the newly spun-off OXIDE Power Crystal (October 2024), are clustered across Factories 1 through 6 in Hokuto City, Yamanashi Prefecture, while laser assembly is localized at the Yokohama Office in Kanagawa Prefecture.

However, the downstream commercial footprint represents an extreme geographical and counterparty concentration:

* Revenue Concentration: Overseas sales represent 90.9% of total revenue. China accounts for 43.7% ($29.35 million), while the U.S. represents 31.2% ($20.97 million).

* Tier-1 OEM Dependency: The top six clients generate exactly 66.0% of corporate revenue. Skyverse Technology Co., Ltd. (China) holds a 31.0% revenue share ($20.81 million), and Marubeni America Corporation accounts for 18.3% ($12.30 million).

* Supply Chain Vulnerability: The Healthcare segment is structurally dependent on Lutetium oxide, sourced predominantly from China. OXIDE counters this sovereign risk via multi-vendor sourcing and targeted inventory stockpiling.

* Unit Economics of Maintenance: Mitigating the OEM concentration risk is the 24/7 run-rate of semiconductor fabs. Degraded optical units require replacement every 1-2 years, generating a highly predictable recurring revenue stream of approximately $6.69 million (20% of the Semiconductor segment), shielding OXIDE from cyclical CapEx freezes.

HDIN Institutional Perspective: The Critical Edge

While algorithmic screeners may penalize OXIDE for its reported -$3.60 million FY2026 net loss, HDIN Research views this as a definitive "buy-the-transition" signal. The headline loss is entirely attributable to the $11.86 million deconsolidation of Raicol Crystals Ltd.—a strategic amputation that removes a -$2.26 million annualized operating drag.

Fundamentally, the Street is mispricing OXIDE's R&D-to-Moat translation. The company expensed $8.05 million directly into SG&A (backed by $4.99 million in public subsidies) to incubate next-generation Silicon Carbide (SiC) utilizing a proprietary, defect-free "Solution Method." Freed from historical warranty leaks and the capital drain of its Middle East operations, OXIDE’s core business is operating at a +329.7% Operating Profit growth rate. The current FCF yield provides the exact liquidity runway required to bridge the gap toward management's stringent mid-term KPIs (10% Operating Margin; 20% EBITDA) without the threat of dilutive equity financing.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure OXIDE Corporation: Strategic Inflection & Deep-Tech Dominance

Segmental Leverage and Working Capital OptimizationA Forensic Analysis of the FY2026 reporting reveals a company aggressively unwinding balance sheet bloat while achieving peak operational leverage. Despite facing raw material inflationary pressures that compressed Gross Margins to 33.6% (from 38.8% in FY2025), sheer volume growth and SG&A reductions expanded Operating Margins by 3.9 percentage points to 5.4%.

* Top-Line Acceleration: Consolidated revenue surged +19.6% YoY to $67.13 million. The Semiconductor Segment remains the cash cow at $33.44 million (+6.3% YoY), capturing nearly 50% of total revenue.

* The Healthcare Inflection: Healthcare segment revenue exploded by +62.9% YoY to $13.35 million. Critically, the segment's order backlog recorded an anomalous +36,759.7% YoY growth to $4.91 million, confirming a structural transition from prototyping to full-scale commercialization for global PET scanner OEMs.

* Working Capital Efficiency: OXIDE demonstrated flawless cash conversion. While revenues expanded, Accounts Receivable (AR) contracted by 28.2% to $8.56 million with an absolute zero ($0.00) bad debt allowance. Concurrently, total inventory was slashed by 31.0% to $18.93 million, liquidating $2.92 million of finished goods without incurring the prior year's $2.44 million defect disposal losses.

* Free Cash Flow Transition: The enterprise flipped a -$4.41 million FY2025 burn into a +$14.46 million FCF surplus in FY2026. With CapEx commitments narrowing by 61.0% to $4.33 million and trailing non-cash depreciation climbing to $5.91 million, the heavy investment cycle has effectively concluded.

Physical Footprint and Client Concentration Risks

OXIDE’s operational physicality is deliberately concentrated to protect proprietary "black-box" material science. All core crystal growth operations, alongside the newly spun-off OXIDE Power Crystal (October 2024), are clustered across Factories 1 through 6 in Hokuto City, Yamanashi Prefecture, while laser assembly is localized at the Yokohama Office in Kanagawa Prefecture.

However, the downstream commercial footprint represents an extreme geographical and counterparty concentration:

* Revenue Concentration: Overseas sales represent 90.9% of total revenue. China accounts for 43.7% ($29.35 million), while the U.S. represents 31.2% ($20.97 million).

* Tier-1 OEM Dependency: The top six clients generate exactly 66.0% of corporate revenue. Skyverse Technology Co., Ltd. (China) holds a 31.0% revenue share ($20.81 million), and Marubeni America Corporation accounts for 18.3% ($12.30 million).

* Supply Chain Vulnerability: The Healthcare segment is structurally dependent on Lutetium oxide, sourced predominantly from China. OXIDE counters this sovereign risk via multi-vendor sourcing and targeted inventory stockpiling.

* Unit Economics of Maintenance: Mitigating the OEM concentration risk is the 24/7 run-rate of semiconductor fabs. Degraded optical units require replacement every 1-2 years, generating a highly predictable recurring revenue stream of approximately $6.69 million (20% of the Semiconductor segment), shielding OXIDE from cyclical CapEx freezes.

HDIN Institutional Perspective: The Critical Edge

While algorithmic screeners may penalize OXIDE for its reported -$3.60 million FY2026 net loss, HDIN Research views this as a definitive "buy-the-transition" signal. The headline loss is entirely attributable to the $11.86 million deconsolidation of Raicol Crystals Ltd.—a strategic amputation that removes a -$2.26 million annualized operating drag.

Fundamentally, the Street is mispricing OXIDE's R&D-to-Moat translation. The company expensed $8.05 million directly into SG&A (backed by $4.99 million in public subsidies) to incubate next-generation Silicon Carbide (SiC) utilizing a proprietary, defect-free "Solution Method." Freed from historical warranty leaks and the capital drain of its Middle East operations, OXIDE’s core business is operating at a +329.7% Operating Profit growth rate. The current FCF yield provides the exact liquidity runway required to bridge the gap toward management's stringent mid-term KPIs (10% Operating Margin; 20% EBITDA) without the threat of dilutive equity financing.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."