Logitech International: Manufacturing Realignment Near Suzhou and Mexico as 24% ROIC Signals Robust Asset-Light Economics

Date : 2026-05-23

Reading : 154

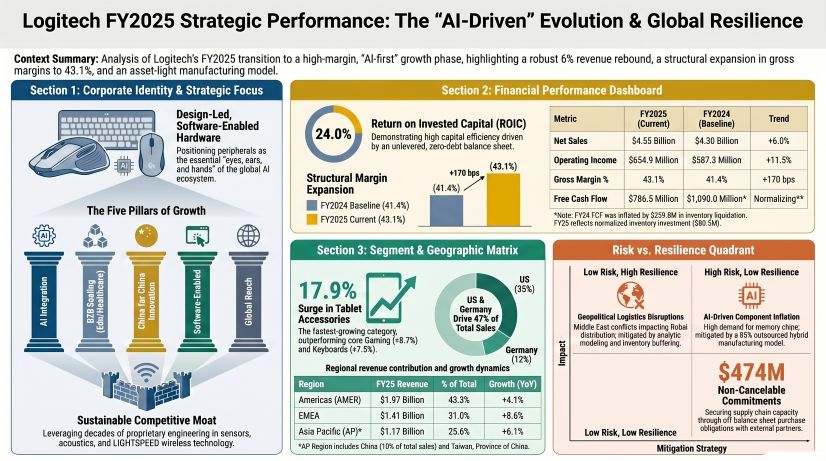

Logitech’s FY2025 filings reveal a stark operational dichotomy. While the company boasts an unlevered balance sheet and a stellar 24% ROIC, a $19.6 million liability for "underwater" purchase commitments and a 90% finished-goods inventory concentration expose severe supply chain rigidity. Driven by Middle East conflicts disrupting its Dubai distribution node and AI data centers siphoning critical memory chips, Logitech is pivoting from its 35% in-house Suzhou dependency toward Southeast Asia and Mexico. For institutional LPs, the 17.9% M&S burn rate reveals a marketing-heavy defense masking as a software-first moat.

Figure Logitech FY2025 Strategic Performance: The Al-Driven Evolution & Global Resilience

Forensic Financials & Segmental Operating Leverage

Forensic Financials & Segmental Operating Leverage

Logitech (NASDAQ: LOGI) operates on a highly optimized, hybrid asset-light model. In FY2025, Capital Expenditures stood at merely $56.1 million against Total D&A of $79.8 million (Depreciation: $59.7 million; Amortization: $20.1 million). This ~70% CapEx-to-D&A ratio confirms a reliance on Tier-1 contract manufacturers to fund physical capacity expansion.

Segmental Inventory & Revenue Distribution (FY2025)

Total net sales expanded by 6.0% YoY to $4.55 billion. The unit economics were heavily buttressed by strategic pricing power in North America, driving Gross Margin expansion from 41.4% (FY2024) to 43.1% in FY2025, and creeping higher by 10 bps to 43.2% in FY2026.

* Gaming: $1.34 billion (+8.7% YoY) – Anchored by proprietary hardware utilizing HITS (Haptic Inductive Trigger System) and the PLAYSYNC multi-console ecosystem.

* Keyboards & Combos: $882.6 million (+7.5% YoY).

* Pointing Devices: $788.8 million (+6.2% YoY) – Leveraging Logi Bolt and Logitech Flow cross-OS interoperability.

* Video Collaboration: $626.0 million (+2.7% YoY).

* Webcams: $315.5 million (-3.0% YoY).

* Tablet Accessories: $299.5 million (+17.9% YoY).

* Headsets & Audio: $179.7 million (+6.7% YoY) and Other Audio at $124.2 million (-14.8% YoY).

Margin Dynamics & Capital Conversion

* Operating Leverage: EBIT surged 11.5% YoY to $654.9 million (14.4% margin), outpacing top-line growth. Proxy EBITDA hit $734.7 million (16.1% margin).

* Tax Anomalies: Net Income grew only 3.2% to $631.5 million, suppressed by a base-effect anomaly. FY2025 recorded an artificially low effective tax rate of 10.7%, driven by a $53.3 million favorable effect from audit resolutions and statute of limitation expirations on uncertain tax positions (UTPs). FY2026 tax rates normalized upward to 14.0%. Total accrued liabilities for remaining UTPs sit at $152.0 million (with $88.5 million in current payable reserves, including $7.2 million in penalties/interest).

* Liquidity & Shareholder Returns: Operating Cash Flow dropped from $1.15 billion in FY24 to $842.6 million in FY25 due to a working capital pivot—liquidating $259.8 million of channel inventory in FY24 and investing $80.5 million to rebuild buffers in FY25. FCF remained highly robust at $786.5 million. Returning this cash, the Board authorized a $588.0 million buyback (6.68 million shares) and paid $207.9 million in dividends (CHF 1.16/share) in FY25. For FY26, a new 3-year, $1.4 billion share repurchase program takes effect in May 2026, alongside a recommended dividend hike to CHF 1.36/share ($243.9 million payout).

Supply Chain Audit & Geo-Economic Moat

Logitech’s physicality is bifurcated, exposing the firm to severe, geographically concentrated operational vulnerabilities.

Manufacturing & Logistics Footprint:

* The Suzhou Tier-1 Facility: Logitech retains 35% of its production value strictly in-house at its Suzhou, China facility to protect intellectual property and maintain agility. The remaining 65% is outsourced to EMS/ODM partners.

* Geopolitical Nearshoring: To circumvent volatile U.S. tariffs and cross-border technology restrictions, third-party manufacturing is aggressively diversifying. The footprint now spans Mexico (serving the Americas), alongside Vietnam, Thailand, Malaysia, and Taiwan.

* EMEA Logistics Chokepoint: Armed conflicts in the Middle East have caused material transit delays and elevated fuel costs for Logitech's critical EMEA distribution center in Dubai.

* R&D vs. Market Footprint: Core R&D is anchored in Lausanne (Switzerland), San Jose (California), and Hsinchu (Taiwan). Geographically, the Americas drive 43.3% of sales ($1.97 billion, with the US alone at 35%). EMEA accounts for 31.0% ($1.41 billion, Germany at 12%), and Asia Pacific represents 25.6% ($1.17 billion). Notably, a localized "China for China" strategy pushed Chinese revenue concentration from 10% in FY25 to 12% in FY26.

Component Squeeze & Regulatory Backlog:

The global AI data center build-out has severely constrained memory chip and micro-controller supplies, driving input inflation for Logitech’s Video Collaboration hardware. Compliance costs are escalating concurrently due to European eco-design directives (WEEE, Packaging Directive, Battery Regulation). In addition, a data exfiltration cybersecurity incident in Fall 2025 underscores the digital vulnerabilities inherent in transitioning to a software-enabled service model like Streamlabs.

HDIN Institutional Perspective

While management categorizes Logitech as a "design-led, software-enabled" enterprise, forensic analysis of the core financials challenges the durability of this moat.

1. The R&D vs. Marketing Discrepancy: R&D intensity marginally increased to 6.8% of sales ($309.0 million) in FY25. However, SG&A vasty overpowers engineering: Marketing and Selling (M&S) consumed 17.9% of sales ($814.4 million), including $355.1 million purely on advertising. This disparity indicates that Logitech’s market share defense against low-cost Asian entrants (e.g., Rapoo, Xiaomi) and retailer house-brands is fundamentally reliant on massive promotional burn, rather than impregnable software lock-in.

2. Supply Chain Financing & Obsolescence Risk: Logitech operates an incredibly tight Cash Conversion Cycle (CCC) of 54.3 days (DSO: 40; DIO: 79.3; DPO: 65). Management aggressively stretched DPO to 79 days by the end of FY26, effectively forcing Tier-1 suppliers to fully finance Logitech's 79-day channel inventory. However, holding $455.0 million in finished goods (90.3% of total $503.7 million inventory) carries a severe obsolescence risk. The $19.6 million liability accrued for "underwater" off-balance sheet purchase commitments (out of $474.0 million total FY26 commitments) penalizes current earnings for structural supply chain misalignments.

3. The California Tax Shield Red Flag: Despite strong global metrics, management holds a $36.4 million valuation allowance against deferred tax assets in the State of California. This signals an internal accounting consensus that it is "more likely than not" Logitech will fail to generate sufficient future taxable income in its San Jose-based US hub to utilize these shields, hinting at structural profitability headwinds in the highly competitive North American theater.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Logitech FY2025 Strategic Performance: The Al-Driven Evolution & Global Resilience

Forensic Financials & Segmental Operating LeverageLogitech (NASDAQ: LOGI) operates on a highly optimized, hybrid asset-light model. In FY2025, Capital Expenditures stood at merely $56.1 million against Total D&A of $79.8 million (Depreciation: $59.7 million; Amortization: $20.1 million). This ~70% CapEx-to-D&A ratio confirms a reliance on Tier-1 contract manufacturers to fund physical capacity expansion.

Segmental Inventory & Revenue Distribution (FY2025)

Total net sales expanded by 6.0% YoY to $4.55 billion. The unit economics were heavily buttressed by strategic pricing power in North America, driving Gross Margin expansion from 41.4% (FY2024) to 43.1% in FY2025, and creeping higher by 10 bps to 43.2% in FY2026.

* Gaming: $1.34 billion (+8.7% YoY) – Anchored by proprietary hardware utilizing HITS (Haptic Inductive Trigger System) and the PLAYSYNC multi-console ecosystem.

* Keyboards & Combos: $882.6 million (+7.5% YoY).

* Pointing Devices: $788.8 million (+6.2% YoY) – Leveraging Logi Bolt and Logitech Flow cross-OS interoperability.

* Video Collaboration: $626.0 million (+2.7% YoY).

* Webcams: $315.5 million (-3.0% YoY).

* Tablet Accessories: $299.5 million (+17.9% YoY).

* Headsets & Audio: $179.7 million (+6.7% YoY) and Other Audio at $124.2 million (-14.8% YoY).

Margin Dynamics & Capital Conversion

* Operating Leverage: EBIT surged 11.5% YoY to $654.9 million (14.4% margin), outpacing top-line growth. Proxy EBITDA hit $734.7 million (16.1% margin).

* Tax Anomalies: Net Income grew only 3.2% to $631.5 million, suppressed by a base-effect anomaly. FY2025 recorded an artificially low effective tax rate of 10.7%, driven by a $53.3 million favorable effect from audit resolutions and statute of limitation expirations on uncertain tax positions (UTPs). FY2026 tax rates normalized upward to 14.0%. Total accrued liabilities for remaining UTPs sit at $152.0 million (with $88.5 million in current payable reserves, including $7.2 million in penalties/interest).

* Liquidity & Shareholder Returns: Operating Cash Flow dropped from $1.15 billion in FY24 to $842.6 million in FY25 due to a working capital pivot—liquidating $259.8 million of channel inventory in FY24 and investing $80.5 million to rebuild buffers in FY25. FCF remained highly robust at $786.5 million. Returning this cash, the Board authorized a $588.0 million buyback (6.68 million shares) and paid $207.9 million in dividends (CHF 1.16/share) in FY25. For FY26, a new 3-year, $1.4 billion share repurchase program takes effect in May 2026, alongside a recommended dividend hike to CHF 1.36/share ($243.9 million payout).

Supply Chain Audit & Geo-Economic Moat

Logitech’s physicality is bifurcated, exposing the firm to severe, geographically concentrated operational vulnerabilities.

Manufacturing & Logistics Footprint:

* The Suzhou Tier-1 Facility: Logitech retains 35% of its production value strictly in-house at its Suzhou, China facility to protect intellectual property and maintain agility. The remaining 65% is outsourced to EMS/ODM partners.

* Geopolitical Nearshoring: To circumvent volatile U.S. tariffs and cross-border technology restrictions, third-party manufacturing is aggressively diversifying. The footprint now spans Mexico (serving the Americas), alongside Vietnam, Thailand, Malaysia, and Taiwan.

* EMEA Logistics Chokepoint: Armed conflicts in the Middle East have caused material transit delays and elevated fuel costs for Logitech's critical EMEA distribution center in Dubai.

* R&D vs. Market Footprint: Core R&D is anchored in Lausanne (Switzerland), San Jose (California), and Hsinchu (Taiwan). Geographically, the Americas drive 43.3% of sales ($1.97 billion, with the US alone at 35%). EMEA accounts for 31.0% ($1.41 billion, Germany at 12%), and Asia Pacific represents 25.6% ($1.17 billion). Notably, a localized "China for China" strategy pushed Chinese revenue concentration from 10% in FY25 to 12% in FY26.

Component Squeeze & Regulatory Backlog:

The global AI data center build-out has severely constrained memory chip and micro-controller supplies, driving input inflation for Logitech’s Video Collaboration hardware. Compliance costs are escalating concurrently due to European eco-design directives (WEEE, Packaging Directive, Battery Regulation). In addition, a data exfiltration cybersecurity incident in Fall 2025 underscores the digital vulnerabilities inherent in transitioning to a software-enabled service model like Streamlabs.

HDIN Institutional Perspective

While management categorizes Logitech as a "design-led, software-enabled" enterprise, forensic analysis of the core financials challenges the durability of this moat.

1. The R&D vs. Marketing Discrepancy: R&D intensity marginally increased to 6.8% of sales ($309.0 million) in FY25. However, SG&A vasty overpowers engineering: Marketing and Selling (M&S) consumed 17.9% of sales ($814.4 million), including $355.1 million purely on advertising. This disparity indicates that Logitech’s market share defense against low-cost Asian entrants (e.g., Rapoo, Xiaomi) and retailer house-brands is fundamentally reliant on massive promotional burn, rather than impregnable software lock-in.

2. Supply Chain Financing & Obsolescence Risk: Logitech operates an incredibly tight Cash Conversion Cycle (CCC) of 54.3 days (DSO: 40; DIO: 79.3; DPO: 65). Management aggressively stretched DPO to 79 days by the end of FY26, effectively forcing Tier-1 suppliers to fully finance Logitech's 79-day channel inventory. However, holding $455.0 million in finished goods (90.3% of total $503.7 million inventory) carries a severe obsolescence risk. The $19.6 million liability accrued for "underwater" off-balance sheet purchase commitments (out of $474.0 million total FY26 commitments) penalizes current earnings for structural supply chain misalignments.

3. The California Tax Shield Red Flag: Despite strong global metrics, management holds a $36.4 million valuation allowance against deferred tax assets in the State of California. This signals an internal accounting consensus that it is "more likely than not" Logitech will fail to generate sufficient future taxable income in its San Jose-based US hub to utilize these shields, hinting at structural profitability headwinds in the highly competitive North American theater.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."