Global Luxury 2026 Outlook: Why LVMH, Kering & Lanvin Group Diverge on Supply Chain Verticalization Amid IEEPA Tariffs and APAC Contraction

Date : 2026-05-23

Reading : 290

The 2025 luxury filings reveal a structural divorce between distressed asset-light aggregators and hyper-verticalized heritage moats. As LVMH (EPA: MC) and Hermès (EPA: RMS) insulate margins via absolute upstream control, highly levered operators like Lanvin Group (NYSE: LANV) face existential liquidity threats. For institutional LPs, the immediate alpha lies in geographic hedges: shielding capital from UFLPA-driven supply shocks and Chinese macro contractions by aggressively overweighting U.S. and Japanese local consumption engines. We project the 2026 cycle will heavily penalize unhedged wholesale exposure as the aspirational consumer base permanently evaporates.

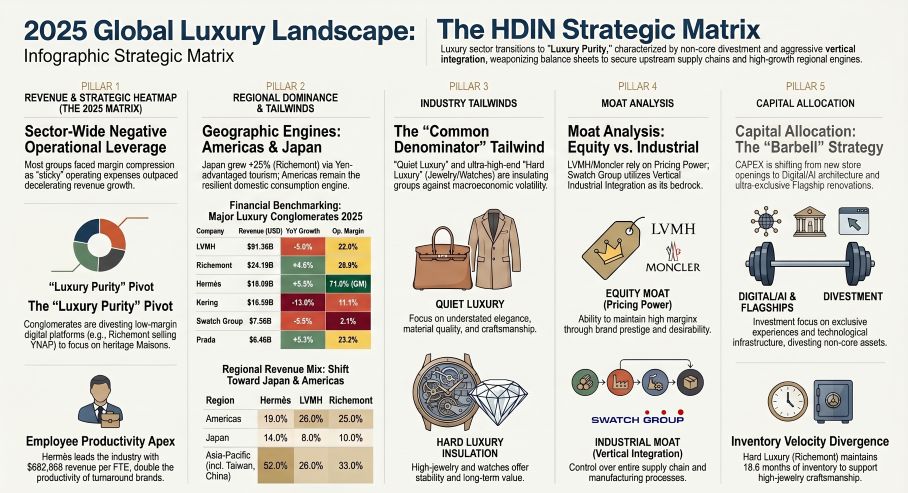

Figure 2025 Global Luxury Landscape

FCF Conversion Spreads, Operating Leverage, and 2026 CAPEX Reallocations

FCF Conversion Spreads, Operating Leverage, and 2026 CAPEX Reallocations

The normalization of the luxury demand curve in 2025 exposed critical vulnerabilities in balance sheet structuring and working capital management. Groups operating strictly in the "Absolute Luxury" tier converted brand equity directly into supreme cash generation, whereas highly cyclical players suffered severe margin compression.

Segmental Inventory & Solvency Audit:

* The Anti-Fragile Balance Sheets: LVMH (EPA: MC) executed an extraordinary 104.1% FCF conversion rate, generating $12,813.1 million in operating FCF against $12,298.7 million in net profit. Similarly, Moncler (BIT: MONC) maintains a formidable $1,648 million (€1,458M) net cash position and a 20.4x interest coverage ratio, allowing it to self-fund its $243.8 million CAPEX allocation without debt market exposure.

* The Over-Leveraged Distress: Lanvin Group (NYSE: LANV) exhibits critical insolvency indicators. Operating with a negative equity deficit of $318.4 million (€281.6M), the group posted an operating loss of $261.9 million (€231.6M). With external borrowing costs hitting 10.0% and a $75.4 million impairment charge levied against its Goodwill and Brand assets, Lanvin operates completely unhedged against foreign exchange (FX) volatility.

* Dividend Suspensions & Margin Contraction: Burberry (LON: BRBY) breached its target leverage range (0.5x–1.0x), spiking to a 2.3x Net Debt-to-EBITDA ratio, forcing the Board to suspend dividend payments. Kering (EPA: KER) saw its recurring operating income plummet 33% YoY to $1,844 million (€1,631M), compressing interest coverage to a dangerous 2.9x against a massive $9,088 million net debt load.

2026 CAPEX Realignment & Infrastructure:

Capital allocation has definitively pivoted from mass physical retail expansion to strict O2O (Online-to-Offline) digital integration and flagship consolidation.

* LVMH deployed a sector-leading $5,163.4 million (€4,567M) in CAPEX, aggressively targeting experiential upgrades like the Tiffany & Co. Fifth Avenue Giga-store and Sephora's global omnichannel rollout.

* Ralph Lauren (NYSE: RL) absorbed $83.9 million in restructuring charges to fund its "Next Generation Transformation" (NGT), an enterprise ERP and AI demand-planning overhaul.

* Burberry explicitly capitulated on retail expansion, capping its FY26 CAPEX at a highly restricted $171.4 million (£130M) to preserve cash flow after physical refurbishments failed to prevent a 12% collapse in comparable store sales.

The San Mauro Pascoli Divestment vs. French Tannery Monopolies

The physical footprint of the luxury sector is currently undergoing a radical reorganization driven by absolute upstream control and geopolitical risk mitigation.

Industrial Aggregation vs. De-Verticalization:

* Hermès (EPA: RMS) continues to construct the industry's deepest physical moat, manufacturing 55% of its objects in-house across 63 French production sites. In 2025, it executed massive capital expansions at the Tannerie d'Annonay, Mégisserie Jullien, and Tannerie Gal facilities to monopolize the global supply of ultra-premium exotic skins.

* Kering executed a hard-luxury supply chain rollup, acquiring Italian eyewear hubs Visard and Lenti, alongside a $130.0 million (€115M) 20% equity stake in jewelry manufacturer Raselli Franco Group (with a binding path to 100% control by 2032).

* Conversely, Lanvin Group stripped its physical infrastructure, transferring Sergio Rossi's historic San Mauro Pascoli factory into a subsidiary and selling a 70% equity stake to Massimo Bonini Group, alongside the complete divestment of Italian menswear manufacturer Caruso.

Geo-Economic Bottlenecks & Tariff Friction:

The operating environment is constrained by a severe "Macro Ceiling." Sourcing frameworks are colliding with strict U.S. enforcement of the Uyghur Forced Labor Prevention Act (UFLPA) and Countering America's Adversaries Through Sanctions Act (CAATSA). Ralph Lauren explicitly flagged margin risk from retaliatory International Emergency Economic Powers Act (IEEPA) U.S. tariffs, while maritime chokepoints in the Red Sea and Panama Canal have permanently inflated global freight outlays. Simultaneously, UK domestic policy—specifically the withdrawal of VAT refunds—has structurally damaged London's retail competitiveness, heavily suppressing EMEIA volumes for legacy British brands.

HDIN Institutional Perspective

While sell-side consensus frames Lanvin Group's divestment of the San Mauro Pascoli factory as a strategic pivot toward an "asset-light, agile operational model," HDIN Research categorically challenges this narrative. Asset-light in the luxury sector is rarely a strategic choice; it is almost exclusively a symptom of capital starvation. Lanvin's stripping of fixed manufacturing assets, combined with unhedged FX exposure and the looming Arpège SAS legal dispute—which threatens the legal rights to the actual Lanvin trademark—signals distressed liquidation, not operational flexibility.

Conversely, the market continues to penalize Swatch Group (SWX: UHR) for its massive $8.78 billion (CHF 7.295B) inventory accumulation against $7.56 billion in net sales. We hold a differentiated viewpoint: Swatch is not suffering from algorithmic merchandising failure. This bloat is a deliberate, highly calculated industrial raw-material moat. By absorbing a severe negative operating margin in its Production segment and refusing to cut manufacturing hours, Swatch is utilizing its balance sheet to permanently secure 32,000 Swiss jobs and monopolize critical component supply (ETA, Nivarox). When global hard luxury demand eventually normalizes, Swatch will command total pricing supremacy over its supply-constrained competitors.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

Figure 2025 Global Luxury Landscape

FCF Conversion Spreads, Operating Leverage, and 2026 CAPEX ReallocationsThe normalization of the luxury demand curve in 2025 exposed critical vulnerabilities in balance sheet structuring and working capital management. Groups operating strictly in the "Absolute Luxury" tier converted brand equity directly into supreme cash generation, whereas highly cyclical players suffered severe margin compression.

Segmental Inventory & Solvency Audit:

* The Anti-Fragile Balance Sheets: LVMH (EPA: MC) executed an extraordinary 104.1% FCF conversion rate, generating $12,813.1 million in operating FCF against $12,298.7 million in net profit. Similarly, Moncler (BIT: MONC) maintains a formidable $1,648 million (€1,458M) net cash position and a 20.4x interest coverage ratio, allowing it to self-fund its $243.8 million CAPEX allocation without debt market exposure.

* The Over-Leveraged Distress: Lanvin Group (NYSE: LANV) exhibits critical insolvency indicators. Operating with a negative equity deficit of $318.4 million (€281.6M), the group posted an operating loss of $261.9 million (€231.6M). With external borrowing costs hitting 10.0% and a $75.4 million impairment charge levied against its Goodwill and Brand assets, Lanvin operates completely unhedged against foreign exchange (FX) volatility.

* Dividend Suspensions & Margin Contraction: Burberry (LON: BRBY) breached its target leverage range (0.5x–1.0x), spiking to a 2.3x Net Debt-to-EBITDA ratio, forcing the Board to suspend dividend payments. Kering (EPA: KER) saw its recurring operating income plummet 33% YoY to $1,844 million (€1,631M), compressing interest coverage to a dangerous 2.9x against a massive $9,088 million net debt load.

2026 CAPEX Realignment & Infrastructure:

Capital allocation has definitively pivoted from mass physical retail expansion to strict O2O (Online-to-Offline) digital integration and flagship consolidation.

* LVMH deployed a sector-leading $5,163.4 million (€4,567M) in CAPEX, aggressively targeting experiential upgrades like the Tiffany & Co. Fifth Avenue Giga-store and Sephora's global omnichannel rollout.

* Ralph Lauren (NYSE: RL) absorbed $83.9 million in restructuring charges to fund its "Next Generation Transformation" (NGT), an enterprise ERP and AI demand-planning overhaul.

* Burberry explicitly capitulated on retail expansion, capping its FY26 CAPEX at a highly restricted $171.4 million (£130M) to preserve cash flow after physical refurbishments failed to prevent a 12% collapse in comparable store sales.

The San Mauro Pascoli Divestment vs. French Tannery Monopolies

The physical footprint of the luxury sector is currently undergoing a radical reorganization driven by absolute upstream control and geopolitical risk mitigation.

Industrial Aggregation vs. De-Verticalization:

* Hermès (EPA: RMS) continues to construct the industry's deepest physical moat, manufacturing 55% of its objects in-house across 63 French production sites. In 2025, it executed massive capital expansions at the Tannerie d'Annonay, Mégisserie Jullien, and Tannerie Gal facilities to monopolize the global supply of ultra-premium exotic skins.

* Kering executed a hard-luxury supply chain rollup, acquiring Italian eyewear hubs Visard and Lenti, alongside a $130.0 million (€115M) 20% equity stake in jewelry manufacturer Raselli Franco Group (with a binding path to 100% control by 2032).

* Conversely, Lanvin Group stripped its physical infrastructure, transferring Sergio Rossi's historic San Mauro Pascoli factory into a subsidiary and selling a 70% equity stake to Massimo Bonini Group, alongside the complete divestment of Italian menswear manufacturer Caruso.

Geo-Economic Bottlenecks & Tariff Friction:

The operating environment is constrained by a severe "Macro Ceiling." Sourcing frameworks are colliding with strict U.S. enforcement of the Uyghur Forced Labor Prevention Act (UFLPA) and Countering America's Adversaries Through Sanctions Act (CAATSA). Ralph Lauren explicitly flagged margin risk from retaliatory International Emergency Economic Powers Act (IEEPA) U.S. tariffs, while maritime chokepoints in the Red Sea and Panama Canal have permanently inflated global freight outlays. Simultaneously, UK domestic policy—specifically the withdrawal of VAT refunds—has structurally damaged London's retail competitiveness, heavily suppressing EMEIA volumes for legacy British brands.

HDIN Institutional Perspective

While sell-side consensus frames Lanvin Group's divestment of the San Mauro Pascoli factory as a strategic pivot toward an "asset-light, agile operational model," HDIN Research categorically challenges this narrative. Asset-light in the luxury sector is rarely a strategic choice; it is almost exclusively a symptom of capital starvation. Lanvin's stripping of fixed manufacturing assets, combined with unhedged FX exposure and the looming Arpège SAS legal dispute—which threatens the legal rights to the actual Lanvin trademark—signals distressed liquidation, not operational flexibility.

Conversely, the market continues to penalize Swatch Group (SWX: UHR) for its massive $8.78 billion (CHF 7.295B) inventory accumulation against $7.56 billion in net sales. We hold a differentiated viewpoint: Swatch is not suffering from algorithmic merchandising failure. This bloat is a deliberate, highly calculated industrial raw-material moat. By absorbing a severe negative operating margin in its Production segment and refusing to cut manufacturing hours, Swatch is utilizing its balance sheet to permanently secure 32,000 Swiss jobs and monopolize critical component supply (ETA, Nivarox). When global hard luxury demand eventually normalizes, Swatch will command total pricing supremacy over its supply-constrained competitors.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*