Jiangsu Sintek Semiconductor: Advanced Packaging Pivot Near Yangzhou Base as Capital Expenditure Signals 2026 Profitability Delay

Date : 2026-05-26

Reading : 99

While Jiangsu Sintek Semiconductor aggressively captures Tier-1 market share via its proprietary CAPiC platform, the firm’s $67.21 million 2025 net loss exposes a severe depreciation drag. Institutional LPs must recognize that despite a 41.0% revenue CAGR, 73.7% of the firm's positive 2025 operating cash flow stemmed directly from government subsidies. As U.S. EAR restrictions tighten, the company’s localized manufacturing moat in Mainland China provides critical supply chain insulation. However, the imminent full-year depreciation of the new Yangzhou Production Base mathematically guarantees a delayed statutory profitability threshold through fiscal 2026.

Forensic Financials & Segmental Capital Allocation

The company’s transition from traditional QFN to high-density Outsource Semiconductor Assembly and Test (OSAT) solutions has generated robust top-line growth but introduced severe unit economic friction. A forensic analysis of the internal capital allocation reveals a highly capital-intensive burn rate masked by state-sponsored financial engineering.

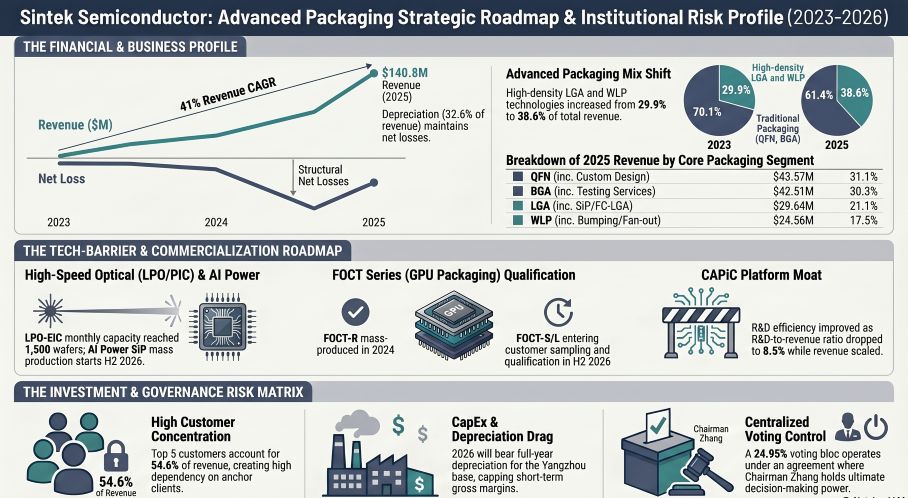

Figure Sintek Semiconductor: Advanced Packaging Strategic Roadmap & lnstitutional Risk Profile (2023-2026)

Segmental Inventory & Margin Constraints:

Segmental Inventory & Margin Constraints:

* Revenue vs. Margin Divergence: Top-line revenue scaled from $70.83M (2023) to $140.82M (2025). However, structural gross margins remained negative at -38.4% (2023), -20.1% (2024), and -18.0% (2025), culminating in a $25.39M absolute gross loss in 2025.

* Segmental Mix Shift: Revenue is aggressively pivoting toward high-density interconnects. LGA (including SiP-LGA) and WLP categories combined grew from 29.9% of total revenue in 2023 to 38.6% in 2025. Over 99.6% of total revenue is derived from core Packaging & Testing Services.

* Operating Leverage & D&A Burden: The aggressive expansion of physical facilities pushed depreciation and amortization (D&A) from $25.26M in 2023 to $42.38M in 2025, consuming 25.5% of total Cost of Goods Sold (COGS).

* Cash Runway & Subsidy Reliance: While 2025 reported a positive Operating Cash Flow (OCF) of $5.56M, $4.10M of this was derived from state cash grants. Free Cash Flow (FCF) conversion remains heavily negative due to $98.63M in 2025 CapEx. With only $26.10M in Q1 2026 cash reserves against $64.88M in contracted capital commitments, reliance on credit facilities is critical.

* Share-Based Compensation Dilution: Administrative expenses artificially spiked by nearly 100% year-over-year to $16.33M in 2025, driven by $5.54M in pre-IPO equity incentives allocated to executives, directly diluting existing shareholder equity.

Supply Chain Audit & Geo-Economic Moat

The physicality of Jiangsu Sintek Semiconductor relies on a heavily centralized footprint designed to counter geopolitical macro-risks, alongside strategic penetration of the High-Performance Computing (HPC) and AI optical module supply chains.

* The Nanjing Production Base: Serving as the primary manufacturing hub (64,280.6 sq. meters), this facility produces the core advanced matrix (FOCT-R, FOCT-S, FOCT-L, and X-SiP). It successfully ramped capacity utilization from 62.3% in 2023 to 84.5% in 2025, diluting marginal production costs.

* The Yangzhou Production Base: Spanning 87,553.8 sq. meters, this facility initiated operations in July 2025. Dedicated currently to LGA packaging, its utilization sits at a nascent 69.0%. Its design capacity will scale to 522.0M pieces by late 2026, acting as the primary catalyst for the anticipated 2026 depreciation drag.

* Tier-1 Synergies & R&D Translation: The CAPiC platform is validating its R&D moat. The R&D-to-revenue ratio decreased from 15.1% in 2023 to 8.5% in 2025, signaling exceptional R&D economies of scale. The company has secured verification for LPO-EIC and delivered global first-generation NPO daisy-chain samples, targeting H2 2026 mass production for AI server integration.

* U.S. EAR Exposure & Supplier Localization: Raw materials (accounting for 35.0% of 2025 COGS) are sourced primarily from domestic partners to insulate against U.S. Bureau of Industry and Security (BIS) sanctions. While 10 direct or subsidiary suppliers have been placed on the BIS Entity List, the localized Mainland China ecosystem ensures no immediate EAR violation or operational disruption.

HDIN Institutional Perspective

While the IPO prospectus champions the CAPiC AI packaging platform as a structural moat, our differentiated viewpoint indicates that the actual financial mechanics reflect a traditional, hardware-intensive burn rate that the Street has not adequately priced in.

The firm is heavily shielded by accumulated tax losses totaling $178.72M (neutralizing short-term cash tax exposure despite the expiration of its 15% High-Tech Enterprise status in 2025). However, governance risks remain elevated. An Acting-in-Concert agreement locks 24.95% of voting control with a single executive bloc, presenting a single-point-of-failure risk during aggressive M&A or capital allocation decisions. Investors must weigh the premium AI/GPU revenue potential against the stark reality of the J-Curve effect: the 2026 fiscal year will be burdened by peak capital depreciation and extreme reliance on state subsidies before true organic FCF materializes in 2027.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Forensic Financials & Segmental Capital Allocation

The company’s transition from traditional QFN to high-density Outsource Semiconductor Assembly and Test (OSAT) solutions has generated robust top-line growth but introduced severe unit economic friction. A forensic analysis of the internal capital allocation reveals a highly capital-intensive burn rate masked by state-sponsored financial engineering.

Figure Sintek Semiconductor: Advanced Packaging Strategic Roadmap & lnstitutional Risk Profile (2023-2026)

Segmental Inventory & Margin Constraints:* Revenue vs. Margin Divergence: Top-line revenue scaled from $70.83M (2023) to $140.82M (2025). However, structural gross margins remained negative at -38.4% (2023), -20.1% (2024), and -18.0% (2025), culminating in a $25.39M absolute gross loss in 2025.

* Segmental Mix Shift: Revenue is aggressively pivoting toward high-density interconnects. LGA (including SiP-LGA) and WLP categories combined grew from 29.9% of total revenue in 2023 to 38.6% in 2025. Over 99.6% of total revenue is derived from core Packaging & Testing Services.

* Operating Leverage & D&A Burden: The aggressive expansion of physical facilities pushed depreciation and amortization (D&A) from $25.26M in 2023 to $42.38M in 2025, consuming 25.5% of total Cost of Goods Sold (COGS).

* Cash Runway & Subsidy Reliance: While 2025 reported a positive Operating Cash Flow (OCF) of $5.56M, $4.10M of this was derived from state cash grants. Free Cash Flow (FCF) conversion remains heavily negative due to $98.63M in 2025 CapEx. With only $26.10M in Q1 2026 cash reserves against $64.88M in contracted capital commitments, reliance on credit facilities is critical.

* Share-Based Compensation Dilution: Administrative expenses artificially spiked by nearly 100% year-over-year to $16.33M in 2025, driven by $5.54M in pre-IPO equity incentives allocated to executives, directly diluting existing shareholder equity.

Supply Chain Audit & Geo-Economic Moat

The physicality of Jiangsu Sintek Semiconductor relies on a heavily centralized footprint designed to counter geopolitical macro-risks, alongside strategic penetration of the High-Performance Computing (HPC) and AI optical module supply chains.

* The Nanjing Production Base: Serving as the primary manufacturing hub (64,280.6 sq. meters), this facility produces the core advanced matrix (FOCT-R, FOCT-S, FOCT-L, and X-SiP). It successfully ramped capacity utilization from 62.3% in 2023 to 84.5% in 2025, diluting marginal production costs.

* The Yangzhou Production Base: Spanning 87,553.8 sq. meters, this facility initiated operations in July 2025. Dedicated currently to LGA packaging, its utilization sits at a nascent 69.0%. Its design capacity will scale to 522.0M pieces by late 2026, acting as the primary catalyst for the anticipated 2026 depreciation drag.

* Tier-1 Synergies & R&D Translation: The CAPiC platform is validating its R&D moat. The R&D-to-revenue ratio decreased from 15.1% in 2023 to 8.5% in 2025, signaling exceptional R&D economies of scale. The company has secured verification for LPO-EIC and delivered global first-generation NPO daisy-chain samples, targeting H2 2026 mass production for AI server integration.

* U.S. EAR Exposure & Supplier Localization: Raw materials (accounting for 35.0% of 2025 COGS) are sourced primarily from domestic partners to insulate against U.S. Bureau of Industry and Security (BIS) sanctions. While 10 direct or subsidiary suppliers have been placed on the BIS Entity List, the localized Mainland China ecosystem ensures no immediate EAR violation or operational disruption.

HDIN Institutional Perspective

While the IPO prospectus champions the CAPiC AI packaging platform as a structural moat, our differentiated viewpoint indicates that the actual financial mechanics reflect a traditional, hardware-intensive burn rate that the Street has not adequately priced in.

The firm is heavily shielded by accumulated tax losses totaling $178.72M (neutralizing short-term cash tax exposure despite the expiration of its 15% High-Tech Enterprise status in 2025). However, governance risks remain elevated. An Acting-in-Concert agreement locks 24.95% of voting control with a single executive bloc, presenting a single-point-of-failure risk during aggressive M&A or capital allocation decisions. Investors must weigh the premium AI/GPU revenue potential against the stark reality of the J-Curve effect: the 2026 fiscal year will be burdened by peak capital depreciation and extreme reliance on state subsidies before true organic FCF materializes in 2027.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."