Yaskawa Electric: Localized Production Pivot Near Yahatanishi as Robotics Margin Contraction Signals Structurally Higher Capital Intensity

Date : 2026-05-27

Reading : 416

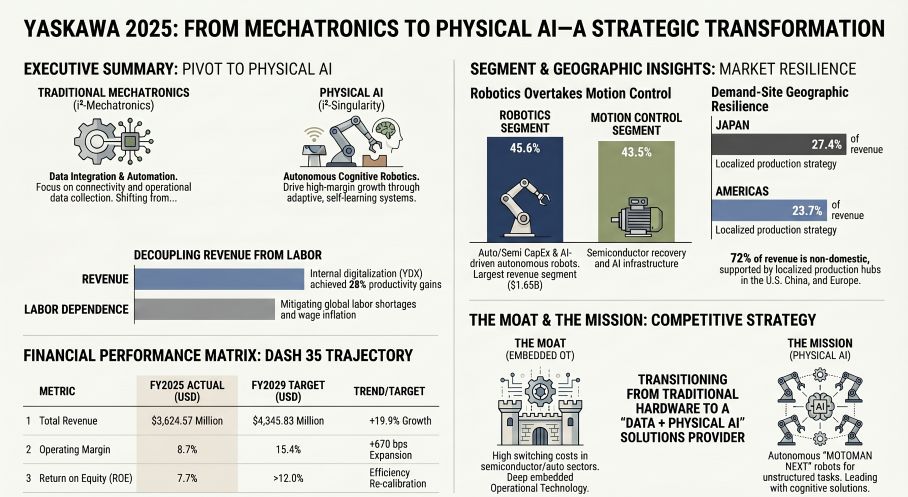

Yaskawa Electric (TYO: 6506) filings for the fiscal year ending February 2026 reveal a margin-dilutive paradox: while Robotics eclipsed Motion Control as the primary revenue engine ($1.65 billion), consolidated operating margins contracted 60 bps to 8.73%. This profitability drag forces a strategic CapEx rotation into localized "demand-site" hubs, notably Robot Factory No. 5 in Yahatanishi. For institutional LPs, the $295.6 million investing outflow underscores a macroeconomic reality: mitigating geopolitical fragmentation via onshore production structurally raises capital intensity, challenging the 12% ROE targets under the newly minted "Dash 35" mandate.

Figure YASKAWA 2025: FROM MECHATRONICS TO PHYSICAL AI-A STRATEGIC TRANSFORMATION

Segmental Capital Allocation & Operating Leverage

Segmental Capital Allocation & Operating Leverage

Despite recording marginal consolidated top-line growth to $3,624.57 million (+0.8% YoY), Yaskawa’s operating leverage deteriorated. Increased indirect costs and FX translation headwinds completely neutralized the price-mix benefits derived from global AI-related semiconductor CapEx. The 38.2% YoY decline in net income to $235.61 million represents an optical distortion resulting from the absence of a prior-year $178.96 million one-off gain linked to the Yantai Dongxing Magnetic Materials Co., Ltd. (YSM) share transfer.

A forensic breakdown of segment-level unit economics and capital allocation reveals a distinct divergence in value-add capture:

Robotics (The Volume-Margin Disconnect):

* Revenue: $1,651.50 million (+4.0% YoY).

* Operating Profit: $136.51 million (-14.0% YoY), yielding a segment-low margin of 8.27%.

* Unit Economics & CapEx: The margin compression stems directly from an unfavorable value-add mix within large-volume projects in Asia. Paradoxically, management is heavily concentrating CapEx here, deploying an industry-leading $132.37 million to aggressively scale the autonomous MOTOMAN NEXT-NHC12 collaborative robots.

Motion Control (The Margin Protector):

* Revenue: $1,578.23 million (-1.1% YoY).

* Operating Profit: $163.03 million (+6.0% YoY), with margins expanding to 10.33%.

* Unit Economics & CapEx: Slower Asian infrastructure demand suppressed top-line volume, but high-margin semiconductor deployment utilizing the iCube Control platform (specifically YRM1030 and iC9200 controllers) and Σ-X series AC servo drives buffered profitability. CapEx allocation stood at $117.49 million.

System Engineering (Peak Profitability):

* Revenue & Margin: $259.04 million (+1.0% YoY), delivering the highest operating margin across the portfolio at 12.88%, driven by resilient domestic steel plant upgrades. CapEx received $60.88 million.

To decouple production capacity from tight labor markets, internal operational efficiencies offset headcount reductions (178 employees exited Motion Control; 157 exited Robotics). Utilizing the proprietary YDX (Yaskawa Digital Transformation) framework, domestic factory productivity increased 28% against a 2019 baseline, successfully absorbing wage inflation vectors. Return on Invested Capital (ROIC) settled at 6.9%, confirming the necessity of the "Dash 35" strategic recalibration targeting an 11.0% ROIC and a $4,345.83 million top-line by FY2029.

Demand-Site Supply Chain Audit & Physicality

Yaskawa is dismantling its traditional Just-In-Time (JIT) architecture in favor of a "demand-site" strategic buffering model. This CapEx-heavy localized production mandate is explicitly designed to preempt cross-border decoupling, currency volatility, and circumvention export risks.

* Global Logistics & Production Hubs: Yaskawa is heavily capitalizing its physical footprint. In Japan, end-to-end motor-to-robot consolidation is fully operational at the Yahatanishi headquarters. To insulate the Americas market (which generates 23.70% of revenue), active investments are centralizing regional R&D and manufacturing across new campuses in Illinois and Ohio. European localization is anchored by robotics manufacturing in Hessen, Bayern (Germany), and Kočevje (Slovenia).

* Tier-1 Sourcing & Component Bottlenecks: To circumvent geopolitical restrictions on rare earth elements critical for high-performance servomotors, procurement is bypassing global spot markets via long-term contracts with domestic Japanese suppliers. Furthermore, the company funded a new printed circuit board (PCB) facility in Quang Ninh, Vietnam, to dilute electronic component dependency on its Shanghai, Shenyang, and Changzhou nodes in China.

* Energy Dependencies & ESG Governance: Yaskawa applies a strict internal carbon price of $33.43 (5,000 JPY) per t-CO2 to force environmental CapEx, aimed at achieving a 51% Scope 1 and 2 emissions cut by 2030 (2018 baseline). The company's CCE100 metric signals extreme operational efficiency, as its hardware reduced 102.2x more carbon in the field than the firm emitted.

* Regulatory & Contingent Liabilities: While litigation remains immaterial, Asset Retirement Obligations (ARO) have scaled to $19.36 million, requiring independent line-item disclosure. Concurrently, human rights due diligence is tightening ahead of impending EU supply chain directives, with the firm mandating strict Self-Assessment Questionnaires (SAQ) across global suppliers.

HDIN Institutional Perspective

While management asserts that the transition to i³-Singularity and software-driven "Physical AI" will yield higher-margin recurring revenues, the actual capital deployment narrative contradicts this pure-play "software-first" thesis. With a massive $381.34 million deployed into physical CapEx, alongside $131.74 million in legally binding forward commitments for physical infrastructure, Yaskawa remains deeply tethered to traditional hardware economics.

The Street is currently underpricing the prolonged margin compression required to decouple supply chains and execute this demand-site localization strategy. Pushing a $33.43 per t-CO2 internal carbon tax while concurrently elevating the WACC discount rate to a stringent 17.2% for goodwill impairment testing signals that management internally acknowledges significant macroeconomic headwinds. Until the YDX digital layer demonstrates standalone SaaS-level monetization rather than merely subsidizing hardware sales, expecting a rapid expansion to the "Dash 35" 15.4% operating margin target by FY2029 is mathematically aggressive.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure YASKAWA 2025: FROM MECHATRONICS TO PHYSICAL AI-A STRATEGIC TRANSFORMATION

Segmental Capital Allocation & Operating LeverageDespite recording marginal consolidated top-line growth to $3,624.57 million (+0.8% YoY), Yaskawa’s operating leverage deteriorated. Increased indirect costs and FX translation headwinds completely neutralized the price-mix benefits derived from global AI-related semiconductor CapEx. The 38.2% YoY decline in net income to $235.61 million represents an optical distortion resulting from the absence of a prior-year $178.96 million one-off gain linked to the Yantai Dongxing Magnetic Materials Co., Ltd. (YSM) share transfer.

A forensic breakdown of segment-level unit economics and capital allocation reveals a distinct divergence in value-add capture:

Robotics (The Volume-Margin Disconnect):

* Revenue: $1,651.50 million (+4.0% YoY).

* Operating Profit: $136.51 million (-14.0% YoY), yielding a segment-low margin of 8.27%.

* Unit Economics & CapEx: The margin compression stems directly from an unfavorable value-add mix within large-volume projects in Asia. Paradoxically, management is heavily concentrating CapEx here, deploying an industry-leading $132.37 million to aggressively scale the autonomous MOTOMAN NEXT-NHC12 collaborative robots.

Motion Control (The Margin Protector):

* Revenue: $1,578.23 million (-1.1% YoY).

* Operating Profit: $163.03 million (+6.0% YoY), with margins expanding to 10.33%.

* Unit Economics & CapEx: Slower Asian infrastructure demand suppressed top-line volume, but high-margin semiconductor deployment utilizing the iCube Control platform (specifically YRM1030 and iC9200 controllers) and Σ-X series AC servo drives buffered profitability. CapEx allocation stood at $117.49 million.

System Engineering (Peak Profitability):

* Revenue & Margin: $259.04 million (+1.0% YoY), delivering the highest operating margin across the portfolio at 12.88%, driven by resilient domestic steel plant upgrades. CapEx received $60.88 million.

To decouple production capacity from tight labor markets, internal operational efficiencies offset headcount reductions (178 employees exited Motion Control; 157 exited Robotics). Utilizing the proprietary YDX (Yaskawa Digital Transformation) framework, domestic factory productivity increased 28% against a 2019 baseline, successfully absorbing wage inflation vectors. Return on Invested Capital (ROIC) settled at 6.9%, confirming the necessity of the "Dash 35" strategic recalibration targeting an 11.0% ROIC and a $4,345.83 million top-line by FY2029.

Demand-Site Supply Chain Audit & Physicality

Yaskawa is dismantling its traditional Just-In-Time (JIT) architecture in favor of a "demand-site" strategic buffering model. This CapEx-heavy localized production mandate is explicitly designed to preempt cross-border decoupling, currency volatility, and circumvention export risks.

* Global Logistics & Production Hubs: Yaskawa is heavily capitalizing its physical footprint. In Japan, end-to-end motor-to-robot consolidation is fully operational at the Yahatanishi headquarters. To insulate the Americas market (which generates 23.70% of revenue), active investments are centralizing regional R&D and manufacturing across new campuses in Illinois and Ohio. European localization is anchored by robotics manufacturing in Hessen, Bayern (Germany), and Kočevje (Slovenia).

* Tier-1 Sourcing & Component Bottlenecks: To circumvent geopolitical restrictions on rare earth elements critical for high-performance servomotors, procurement is bypassing global spot markets via long-term contracts with domestic Japanese suppliers. Furthermore, the company funded a new printed circuit board (PCB) facility in Quang Ninh, Vietnam, to dilute electronic component dependency on its Shanghai, Shenyang, and Changzhou nodes in China.

* Energy Dependencies & ESG Governance: Yaskawa applies a strict internal carbon price of $33.43 (5,000 JPY) per t-CO2 to force environmental CapEx, aimed at achieving a 51% Scope 1 and 2 emissions cut by 2030 (2018 baseline). The company's CCE100 metric signals extreme operational efficiency, as its hardware reduced 102.2x more carbon in the field than the firm emitted.

* Regulatory & Contingent Liabilities: While litigation remains immaterial, Asset Retirement Obligations (ARO) have scaled to $19.36 million, requiring independent line-item disclosure. Concurrently, human rights due diligence is tightening ahead of impending EU supply chain directives, with the firm mandating strict Self-Assessment Questionnaires (SAQ) across global suppliers.

HDIN Institutional Perspective

While management asserts that the transition to i³-Singularity and software-driven "Physical AI" will yield higher-margin recurring revenues, the actual capital deployment narrative contradicts this pure-play "software-first" thesis. With a massive $381.34 million deployed into physical CapEx, alongside $131.74 million in legally binding forward commitments for physical infrastructure, Yaskawa remains deeply tethered to traditional hardware economics.

The Street is currently underpricing the prolonged margin compression required to decouple supply chains and execute this demand-site localization strategy. Pushing a $33.43 per t-CO2 internal carbon tax while concurrently elevating the WACC discount rate to a stringent 17.2% for goodwill impairment testing signals that management internally acknowledges significant macroeconomic headwinds. Until the YDX digital layer demonstrates standalone SaaS-level monetization rather than merely subsidizing hardware sales, expecting a rapid expansion to the "Dash 35" 15.4% operating margin target by FY2029 is mathematically aggressive.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."