AISpeech: Manufacturing Pivot Near Liuzhou Facility as 63.24% Gross Margin Signals Structural Premium in Auto Supply Chain

Date : 2026-05-27

Reading : 104

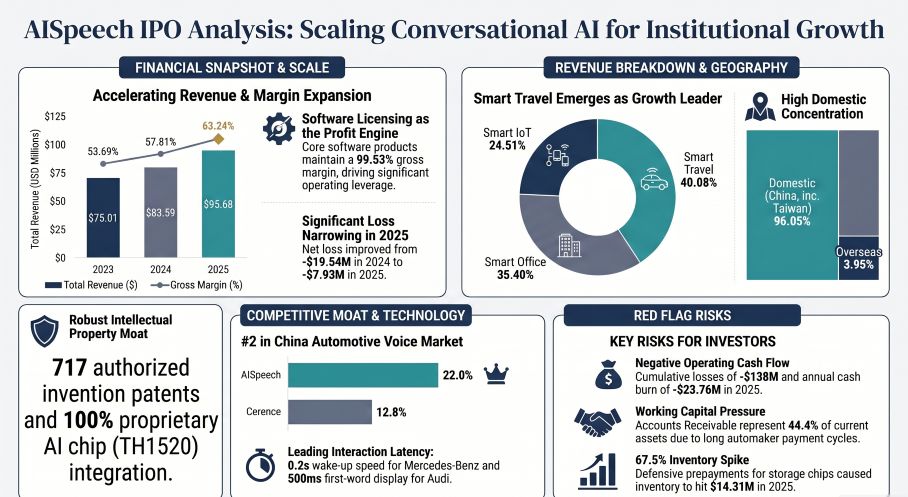

AISpeech's $216 million IPO prospectus reveals a critical transition from pure algorithm licensing to a vertically integrated physical supply chain. While securing 22.0% of China's pre-installed automotive voice market, the firm's robust 63.24% gross margin masks severe working capital distress, evidenced by a sustained $23.76 million operating cash outflow in 2025. Constrained by lengthy Tier-1 automaker payment cycles and semiconductor inflation requiring defensive memory chip hoarding, the company’s 2026 profitability target relies heavily on resolving its cash conversion cycle amid fierce, capital-intensive macro headwinds.

Figure AISpeech IPO Analysis: Scaling Conversational Al for Institutional Growth

Forensic Financials & Segmental Margin Accretion

Forensic Financials & Segmental Margin Accretion

AISpeech’s financial architecture displays a pronounced disconnect between top-line quality and Free Cash Flow (FCF) conversion. A Forensic Analysis of its operating leverage indicates that while the company is successfully executing a Land-and-Expand strategy against legacy incumbents like iFlytek (SZSE: 002230) and Cerence (NASDAQ: CRNC), internal capital allocation remains under severe pressure from downstream client leverage.

* Segmental Revenue & Unit Economics: Revenue expanded from $75.01 million (2023) to $95.68 million (2025). The Smart Travel segment (40.08% of total revenue) operates as the primary growth engine, where core Software Products & Licensing command a near-zero marginal cost, yielding a 99.53% gross margin. This directly engineered the consolidated gross margin expansion from 53.69% to 63.24% over the 36-month reporting period.

* Operating Leverage & R&D-to-Moat Translation: The firm applies a highly conservative 100% R&D expensing policy (zero capitalization), booking $35.27 million in 2025. This R&D spend translates directly into the proprietary DUI 2.0 Platform—a low-code orchestration layer that prevents the "human-body-shop" margin dilution typical of AI custom development (custom dev margins sustained at 78.86% in auto).

* Working Capital Squeeze: Despite narrowing net losses to -$7.93 million, OCF plunged to -$23.76 million. Accounts Receivable turnover deteriorated to 2.07x (balance: $45.28 million), while Inventory turnover collapsed from 3.59x to 2.78x.

Supply Chain Audit & Geo-Economic Moat: The Liuzhou Physicality

AISpeech is abandoning its pure asset-light model in response to geopolitical supply shocks and the physical realities of edge-AI deployment. The company exhibits polarized value-chain bargaining power: total pricing dominance downstream via software licensing, offset by extreme vulnerability to upstream silicon suppliers.

* Geographic Manufacturing Shift: In H2 2024, the company activated the Guangxi AISpeech self-production base in Liuzhou. This pivot away from 100% outsourced manufacturing allows localized, in-house assembly of automotive electronic products (smart dashboards), co-locating near Southern China's automotive manufacturing hubs.

* Core R&D Hub: Foundational large language model (DFM) training remains centralized at the Ascendas IT Park in Suzhou, heavily reliant on Alibaba Cloud (NYSE: BABA) for compute resources ($1.57 million in related-party cloud procurement).

* Defensive Semiconductor Hoarding: Anticipating memory chip shortages, AISpeech aggressively spiked its supplier concentration. Procurement from Tier-1 hardware supplier Shenzhen Zhilintai surged to $8.02 million (13.50% of total), which included a highly unusual $3.89 million defensive prepayment package ($1.41 million paid strictly in advance) to lock in storage capacity for its self-branded AI Notebooks featuring the TH1520 AI Chip.

HDIN Institutional Perspective

While management explicitly guides for a 2026 profitability inflection, HDIN Research challenges the timeline of this cash-flow crossover.

The S-1 equivalent positions AISpeech as a "software-first" compounder. However, the $216 million IPO CapEx realignment—earmarked primarily for cloud leasing ($32.00 million) and server hardware procurement ($15.30 million)—will trigger an intensive depreciation and amortization cycle between 2026 and 2028. Furthermore, the bloat in physical inventory ($14.31 million) and the erosion of AR turnover suggest that Tier-1 auto giants (BYD, SAIC, Geely) are effectively utilizing AISpeech as a zero-interest financing vehicle. The Street has yet to fully price in the reality that AISpeech’s premium 99% software margins are actively cross-subsidizing a traditional, hardware-intensive working capital burn.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure AISpeech IPO Analysis: Scaling Conversational Al for Institutional Growth

Forensic Financials & Segmental Margin AccretionAISpeech’s financial architecture displays a pronounced disconnect between top-line quality and Free Cash Flow (FCF) conversion. A Forensic Analysis of its operating leverage indicates that while the company is successfully executing a Land-and-Expand strategy against legacy incumbents like iFlytek (SZSE: 002230) and Cerence (NASDAQ: CRNC), internal capital allocation remains under severe pressure from downstream client leverage.

* Segmental Revenue & Unit Economics: Revenue expanded from $75.01 million (2023) to $95.68 million (2025). The Smart Travel segment (40.08% of total revenue) operates as the primary growth engine, where core Software Products & Licensing command a near-zero marginal cost, yielding a 99.53% gross margin. This directly engineered the consolidated gross margin expansion from 53.69% to 63.24% over the 36-month reporting period.

* Operating Leverage & R&D-to-Moat Translation: The firm applies a highly conservative 100% R&D expensing policy (zero capitalization), booking $35.27 million in 2025. This R&D spend translates directly into the proprietary DUI 2.0 Platform—a low-code orchestration layer that prevents the "human-body-shop" margin dilution typical of AI custom development (custom dev margins sustained at 78.86% in auto).

* Working Capital Squeeze: Despite narrowing net losses to -$7.93 million, OCF plunged to -$23.76 million. Accounts Receivable turnover deteriorated to 2.07x (balance: $45.28 million), while Inventory turnover collapsed from 3.59x to 2.78x.

Supply Chain Audit & Geo-Economic Moat: The Liuzhou Physicality

AISpeech is abandoning its pure asset-light model in response to geopolitical supply shocks and the physical realities of edge-AI deployment. The company exhibits polarized value-chain bargaining power: total pricing dominance downstream via software licensing, offset by extreme vulnerability to upstream silicon suppliers.

* Geographic Manufacturing Shift: In H2 2024, the company activated the Guangxi AISpeech self-production base in Liuzhou. This pivot away from 100% outsourced manufacturing allows localized, in-house assembly of automotive electronic products (smart dashboards), co-locating near Southern China's automotive manufacturing hubs.

* Core R&D Hub: Foundational large language model (DFM) training remains centralized at the Ascendas IT Park in Suzhou, heavily reliant on Alibaba Cloud (NYSE: BABA) for compute resources ($1.57 million in related-party cloud procurement).

* Defensive Semiconductor Hoarding: Anticipating memory chip shortages, AISpeech aggressively spiked its supplier concentration. Procurement from Tier-1 hardware supplier Shenzhen Zhilintai surged to $8.02 million (13.50% of total), which included a highly unusual $3.89 million defensive prepayment package ($1.41 million paid strictly in advance) to lock in storage capacity for its self-branded AI Notebooks featuring the TH1520 AI Chip.

HDIN Institutional Perspective

While management explicitly guides for a 2026 profitability inflection, HDIN Research challenges the timeline of this cash-flow crossover.

The S-1 equivalent positions AISpeech as a "software-first" compounder. However, the $216 million IPO CapEx realignment—earmarked primarily for cloud leasing ($32.00 million) and server hardware procurement ($15.30 million)—will trigger an intensive depreciation and amortization cycle between 2026 and 2028. Furthermore, the bloat in physical inventory ($14.31 million) and the erosion of AR turnover suggest that Tier-1 auto giants (BYD, SAIC, Geely) are effectively utilizing AISpeech as a zero-interest financing vehicle. The Street has yet to fully price in the reality that AISpeech’s premium 99% software margins are actively cross-subsidizing a traditional, hardware-intensive working capital burn.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."