Beijing Ingenic: Advanced Node Pivot Near Taiwan Production Hub as Deflated ASPs Signal Suppressed 2026 Capital Efficiency

Date : 2026-05-28

Reading : 223

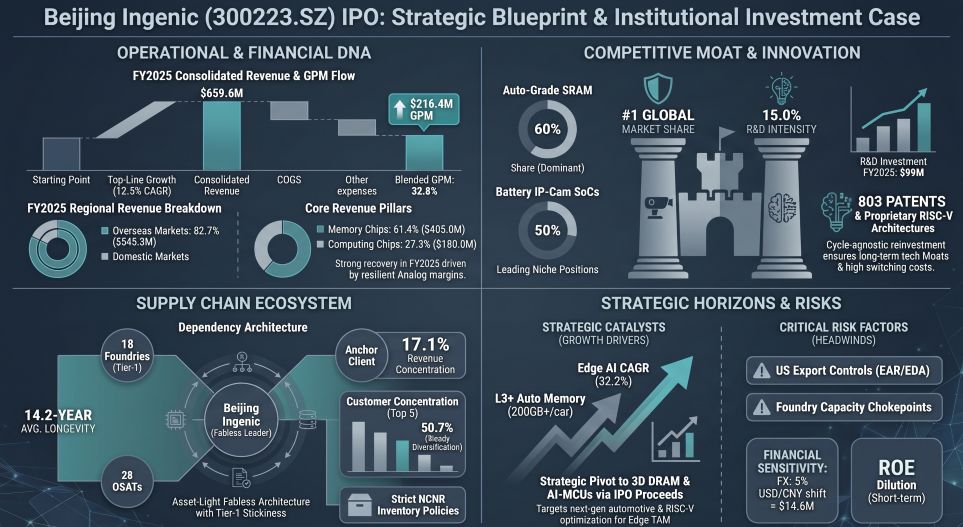

Beijing Ingenic’s 2025 revenue rebounded 12.5% to $659.62 million, yet net profit marginally recovered by 3.1% to $52.22 million, exposing a severe decoupling driven by defensive pricing and upstream foundry dependencies. With an unlevered balance sheet holding $693.83 million in short-term liquidity, the firm operates with a constrained 1.08x equity multiplier, capping ROE at 4.3%. For institutional LPs, the firm’s dominance in auto-grade SRAM provides a definitive moat, but mitigating US EDA software restrictions and deploying trapped capital via M&A are critical mandates ahead of the 2026 Edge AI replacement cycle.

Figure Beijing Ingenic lPO: Strategic Blueprint & Institutional Investment Case

Forensic Financials & Segmental Margin Compression

Forensic Financials & Segmental Margin Compression

A Forensic Analysis of Beijing Ingenic (SZSE: 300223) reveals an intentional sacrifice of unit economics to defend market share amid global sector de-stocking. The 270-bps compression in gross profit margin (GPM)—from 35.5% in 2023 to 32.8% in 2025—demonstrates deteriorating operating leverage, heavily padded by below-the-line items. In 2025, non-operating income ($24.58 million) constituted a massive 47.1% of total net profit, propped up by $12.63 million in bank interest and a 15% preferential High-Tech Enterprise tax rate.

FY2025 Quantitative Inventory & Segmental Breakdown:

* Memory Chips (61.4% of Revenue): Revenue of $405.04 million on 602.42 million units. GPM deteriorated 440 bps (from 34.4% in 2023 to 30.0% in 2025) due to TWD-RMB FX headwinds and product mix shifts toward entry-level NOR Flash.

* Computing Chips (27.3% of Revenue): Revenue of $179.95 million on 120.87 million units. Despite a unit volume increase, ASP plummeted 27.3% from $2.05 to $1.49 per unit, driving a 200-bps GPM drop (32.8% to 30.8%).

* Analog Chips (10.7% of Revenue): Revenue of $70.35 million on 250.25 million units. The sole margin-accretive segment, achieving a 330-bps GPM expansion to 50.5% through precision wafer procurement optimization.

* Internal Capital Allocation: Administrative OPEX ballooned by 25.3% to 5.7% of revenue, driven by the 2024 Restricted Stock Incentive Plan (3.11 million unvested shares). R&D expenditure remained aggressive at $99.06 million (15.0% of revenue), though 98.8% was expensed rather than capitalized, reflecting highly conservative accounting.

Global Supply Chain Audit & Geo-Economic Moat

Beijing Ingenic operates an asset-light physicality completely tethered to 18 upstream foundries and 28 OSAT partners, creating severe capacity choking points. While R&D is decentralized across mainland nodes (Hefei, Shanghai, Xiamen, Wuhan, Shenzhen) and international centers in Israel and the United States (via the 2020 NASDAQ: ISSI acquisition), operational execution hinges on specialized regional coordination.

Logistical and Geopolitical Constraints:

* The Taiwan Production Hub: The Taiwan, China branch of Integrated Silicon Solution (Cayman), Inc. acts as the central production coordination hub, directly interfacing with regional foundries to manage the $216.36 million in procurement allocated to the top 5 suppliers.

* Channel Concentration & NCNR Governance: Over 79.5% of revenue routes through distributors. A US-based distributor ("Customer A") represents 17.1% ($113.04 million) of total revenue. To prevent channel stuffing, Beijing Ingenic enforces strict Non-Cancelable/Non-Returnable (NCNR) terms for automotive/industrial chips, stabilizing its 14.2-year average customer longevity.

* Tariff & Regulatory Headwinds: Products exported to the US fall under HTS 8542, exposing them to a devastating 60% cumulative tariff burden (50% baseline + 10% fentanyl penalty). Furthermore, US Executive Order 14105 classifies the firm as a "Restricted Foreign Person," threatening its access to critical US-origin EDA software required for its 16nm and RISC-V tape-outs.

* Inventory Overhang: The strategic stockpiling executed during price dips pushed inventory turnover to 323 days ($413.86 million equivalent). While the firm booked a $6.68 million net impairment reversal in 2025, holding nearly a year's worth of stock exposes the balance sheet to severe obsolescence risks if the 3D DRAM transition is delayed.

HDIN Institutional Perspective

While management claims the upcoming migration to 3D DRAM and RISC-V AI-MCUs will act as primary growth engines, the structural reality suggests an overcapitalized firm struggling with capital deployment velocity.

Differentiated Viewpoint: Beijing Ingenic’s unlevered equity structure is exceptionally passive. Maintaining $693.83 million in liquid assets while generating an ROE of under 4.3% signals a severe lack of financial engineering. The draft prospectus outlines an intent to fund "strategic M&A" with IPO proceeds, yet the firm already holds enough idle cash to execute mid-market acquisitions immediately. We assess that the primary bottleneck is not gross margin compression, but the absolute failure to utilize financial leverage. Unless management deploys this trapped capital to acquire EDA alternatives or secure guaranteed foundry capacity ahead of the projected 32.2% CAGR (2026-2030) in Edge AI shipments, the immediate dilution of net tangible assets per share from any subsequent offering will heavily penalize minority shareholders.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Beijing Ingenic lPO: Strategic Blueprint & Institutional Investment Case

Forensic Financials & Segmental Margin CompressionA Forensic Analysis of Beijing Ingenic (SZSE: 300223) reveals an intentional sacrifice of unit economics to defend market share amid global sector de-stocking. The 270-bps compression in gross profit margin (GPM)—from 35.5% in 2023 to 32.8% in 2025—demonstrates deteriorating operating leverage, heavily padded by below-the-line items. In 2025, non-operating income ($24.58 million) constituted a massive 47.1% of total net profit, propped up by $12.63 million in bank interest and a 15% preferential High-Tech Enterprise tax rate.

FY2025 Quantitative Inventory & Segmental Breakdown:

* Memory Chips (61.4% of Revenue): Revenue of $405.04 million on 602.42 million units. GPM deteriorated 440 bps (from 34.4% in 2023 to 30.0% in 2025) due to TWD-RMB FX headwinds and product mix shifts toward entry-level NOR Flash.

* Computing Chips (27.3% of Revenue): Revenue of $179.95 million on 120.87 million units. Despite a unit volume increase, ASP plummeted 27.3% from $2.05 to $1.49 per unit, driving a 200-bps GPM drop (32.8% to 30.8%).

* Analog Chips (10.7% of Revenue): Revenue of $70.35 million on 250.25 million units. The sole margin-accretive segment, achieving a 330-bps GPM expansion to 50.5% through precision wafer procurement optimization.

* Internal Capital Allocation: Administrative OPEX ballooned by 25.3% to 5.7% of revenue, driven by the 2024 Restricted Stock Incentive Plan (3.11 million unvested shares). R&D expenditure remained aggressive at $99.06 million (15.0% of revenue), though 98.8% was expensed rather than capitalized, reflecting highly conservative accounting.

Global Supply Chain Audit & Geo-Economic Moat

Beijing Ingenic operates an asset-light physicality completely tethered to 18 upstream foundries and 28 OSAT partners, creating severe capacity choking points. While R&D is decentralized across mainland nodes (Hefei, Shanghai, Xiamen, Wuhan, Shenzhen) and international centers in Israel and the United States (via the 2020 NASDAQ: ISSI acquisition), operational execution hinges on specialized regional coordination.

Logistical and Geopolitical Constraints:

* The Taiwan Production Hub: The Taiwan, China branch of Integrated Silicon Solution (Cayman), Inc. acts as the central production coordination hub, directly interfacing with regional foundries to manage the $216.36 million in procurement allocated to the top 5 suppliers.

* Channel Concentration & NCNR Governance: Over 79.5% of revenue routes through distributors. A US-based distributor ("Customer A") represents 17.1% ($113.04 million) of total revenue. To prevent channel stuffing, Beijing Ingenic enforces strict Non-Cancelable/Non-Returnable (NCNR) terms for automotive/industrial chips, stabilizing its 14.2-year average customer longevity.

* Tariff & Regulatory Headwinds: Products exported to the US fall under HTS 8542, exposing them to a devastating 60% cumulative tariff burden (50% baseline + 10% fentanyl penalty). Furthermore, US Executive Order 14105 classifies the firm as a "Restricted Foreign Person," threatening its access to critical US-origin EDA software required for its 16nm and RISC-V tape-outs.

* Inventory Overhang: The strategic stockpiling executed during price dips pushed inventory turnover to 323 days ($413.86 million equivalent). While the firm booked a $6.68 million net impairment reversal in 2025, holding nearly a year's worth of stock exposes the balance sheet to severe obsolescence risks if the 3D DRAM transition is delayed.

HDIN Institutional Perspective

While management claims the upcoming migration to 3D DRAM and RISC-V AI-MCUs will act as primary growth engines, the structural reality suggests an overcapitalized firm struggling with capital deployment velocity.

Differentiated Viewpoint: Beijing Ingenic’s unlevered equity structure is exceptionally passive. Maintaining $693.83 million in liquid assets while generating an ROE of under 4.3% signals a severe lack of financial engineering. The draft prospectus outlines an intent to fund "strategic M&A" with IPO proceeds, yet the firm already holds enough idle cash to execute mid-market acquisitions immediately. We assess that the primary bottleneck is not gross margin compression, but the absolute failure to utilize financial leverage. Unless management deploys this trapped capital to acquire EDA alternatives or secure guaranteed foundry capacity ahead of the projected 32.2% CAGR (2026-2030) in Edge AI shipments, the immediate dilution of net tangible assets per share from any subsequent offering will heavily penalize minority shareholders.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."