Phihong Technology: Strategic Reallocation Near Haiphong Hub as Negative FCF Signals Severe EV Margin Contraction

Date : 2026-05-28

Reading : 103

Phihong Technology’s FY2025 audit reveals a severe fundamental recalibration: a $25.80M negative operating cash flow driven by extreme U.S. tariff volatility and Chinese EV hardware overcapacity. To counter a 593 bps gross margin contraction, management is aggressively pivoting capital toward the Haiphong Plant in Vietnam, which now shields 51% of total revenue from geopolitical friction. For institutional LPs, Phihong’s structural viability relies entirely on effectively monetizing its high-margin Megawatt Charging System (MCS) pipeline and executing its 2026 target of 48 million units before foreign exchange fluctuations further erode profitability.

Forensic Analysis of Segmental Margin Deterioration and Capital Allocation

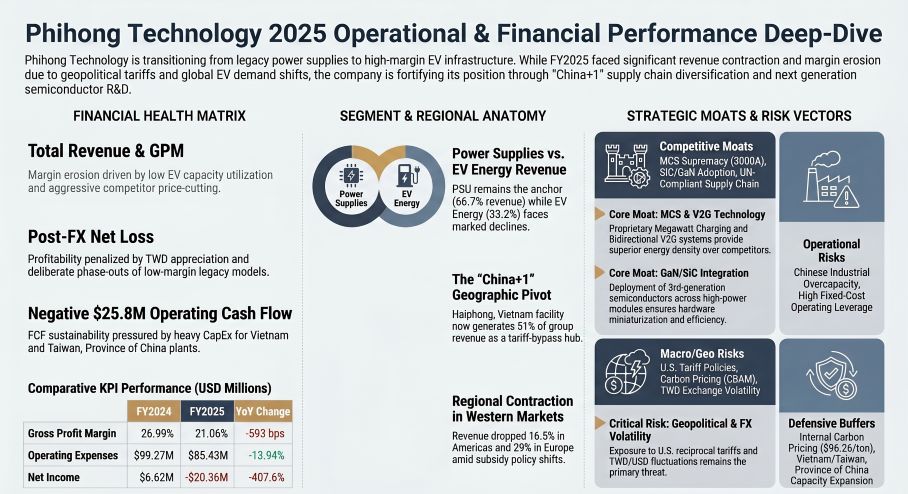

Phihong Technology faces significant near-term financial headwinds characterized by a contracting top-line (-10.11% YoY to $314.30M) and deeply negative operating leverage. Despite executing a disciplined $13.84M (13.94%) reduction in operating expenses, the sheer velocity of gross profit deterioration outpaced cost-saving measures, pushing the consolidated operating margin down 472 bps to -6.12%.

Figure Phihong Technology 2025 0perational & Financial Performance Deep-Dive

Unit Economics & R&D-to-Moat Translation:

The $25.80M negative OCF points to distressed cash conversion, exacerbated by the deliberate September–December 2025 phase-out of high-volume, low-margin legacy products. To replace commoditized revenue, Phihong maintained an 8.76% R&D intensity ($27.52M). Management plans to surge R&D CapEx by roughly 30% to $35.81M in FY2026, primarily funding the Silicon Carbide (SiC) and Gallium Nitride (GaN) architectures required for its Bidirectional Vehicle-to-Grid (V2G) (UL 1741/9741 certified) and high-density Megawatt Charging System (MCS) pipelines (targeting 1,500–3,000A output).

Geo-Economic Moat Construction and Supply Chain Recalibration

Phihong’s physical footprint dictates its defensive strategy against geopolitical and macroeconomic shocks. The company is actively restructuring its manufacturing base to bypass the Trump administration's reciprocal U.S. tariffs and neutralize the risk of upstream carbon-cost pass-throughs.

* The Vietnam Tariff Buffer: The Haiphong Plant (PHV) in North Vietnam is the centerpiece of the "China+1" strategy. Following a $38.89M self-funded CapEx deployment, this facility now generates 51% of total group revenue, effectively insulating Western-bound exports from U.S.-China trade friction.

* High-Value Assembly Localization: The company deployed $30.76M into the expansion of Tainan Plants 1, 2, and 3 in Taiwan, Province of China. This capacity is specifically allocated for the final assembly and reliability testing of the high-margin Zerova AC/DC charging stations.

* Mainland China Consolidation: Operations in the Dongguan area (including PHC, PHP, and the Dongguan Tiesong 3rd Plant) received a modest $10.48M CapEx injection, strictly aimed at consolidating existing output and retrofitting air compressors to meet internal ESG targets rather than expanding localized exposure.

* Regulatory & Litigation Backlog: Phihong proactively instituted a strict Internal Carbon Pricing (ICP) mechanism at $96.26 per metric ton to front-run the 2026 EU Carbon Border Adjustment Mechanism (CBAM). Legally, the company is engaged in an offensive trade secret infringement appeal (filed February 9, 2026) to safeguard its proprietary EV power-sharing algorithms.

HDIN Institutional Perspective

While management attributes the FY2025 net margin collapse (-6.48%) to macro-level FX shocks and U.S. EV subsidy shifts, the structural deficit suggests a more fundamental mismatch in operating leverage that the Street is currently underpricing. The intentional phasing out of low-margin legacy EV hardware in late 2025 was a necessary defense against Chinese price dumping, yet the sheer scale of fixed-cost absorption in the newly expanded Tainan and Haiphong facilities remains unproven.

However, Phihong’s explicit refusal to slash its innovation budget during a revenue contraction is a strong signal of structural resilience. The projected $19.85M operational deficit for FY2026 will burn near-term liquidity, but by establishing a decentralized, tariff-resistant supply chain and targeting a 48 million unit volume output, the company is sacrificing immediate Free Cash Flow to build an insurmountable hardware moat. If the company successfully scales its 720kW modular chargers to capture the commercial heavy-duty electrification supercycle, the currently negative operating leverage will violently reverse into outsized profitability.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Forensic Analysis of Segmental Margin Deterioration and Capital Allocation

Phihong Technology faces significant near-term financial headwinds characterized by a contracting top-line (-10.11% YoY to $314.30M) and deeply negative operating leverage. Despite executing a disciplined $13.84M (13.94%) reduction in operating expenses, the sheer velocity of gross profit deterioration outpaced cost-saving measures, pushing the consolidated operating margin down 472 bps to -6.12%.

Figure Phihong Technology 2025 0perational & Financial Performance Deep-Dive

Table FY2025 Segment Performance and Margin Compression Analysis

| Metric / Segment | FY2025 Value (USD) | YoY Variance / Margin Dynamics |

|---|---|---|

| Power Supply Unit (PSU) | $209.69M (66.72% of Rev) | +4.00% YoY; supported by a 9% reduction in segment operating expenses |

| EV Energy (Zerova) | $104.38M (33.21% of Rev) | Severe contraction; margin penalized by Chinese price dumping and underutilized capacity |

| Gross Profit Margin (GPM) | 21.06% | -593 bps; dragged by EV segment irrational price-cutting |

| Net Income / Margin | -$20.36M / -6.48% | -407.61% YoY; exacerbated by Q2 TWD appreciation FX losses |

| Operating Cash Flow (OCF) | -$25.80M | -$28.96M YoY swing; indicates severe working capital bottlenecks |

| Liquidity & Leverage | $112.25M Cash Balance | 1.78x Current Ratio; debt-to-equity at manageable 55.74% (+594 bps) |

The $25.80M negative OCF points to distressed cash conversion, exacerbated by the deliberate September–December 2025 phase-out of high-volume, low-margin legacy products. To replace commoditized revenue, Phihong maintained an 8.76% R&D intensity ($27.52M). Management plans to surge R&D CapEx by roughly 30% to $35.81M in FY2026, primarily funding the Silicon Carbide (SiC) and Gallium Nitride (GaN) architectures required for its Bidirectional Vehicle-to-Grid (V2G) (UL 1741/9741 certified) and high-density Megawatt Charging System (MCS) pipelines (targeting 1,500–3,000A output).

Geo-Economic Moat Construction and Supply Chain Recalibration

Phihong’s physical footprint dictates its defensive strategy against geopolitical and macroeconomic shocks. The company is actively restructuring its manufacturing base to bypass the Trump administration's reciprocal U.S. tariffs and neutralize the risk of upstream carbon-cost pass-throughs.

* The Vietnam Tariff Buffer: The Haiphong Plant (PHV) in North Vietnam is the centerpiece of the "China+1" strategy. Following a $38.89M self-funded CapEx deployment, this facility now generates 51% of total group revenue, effectively insulating Western-bound exports from U.S.-China trade friction.

* High-Value Assembly Localization: The company deployed $30.76M into the expansion of Tainan Plants 1, 2, and 3 in Taiwan, Province of China. This capacity is specifically allocated for the final assembly and reliability testing of the high-margin Zerova AC/DC charging stations.

* Mainland China Consolidation: Operations in the Dongguan area (including PHC, PHP, and the Dongguan Tiesong 3rd Plant) received a modest $10.48M CapEx injection, strictly aimed at consolidating existing output and retrofitting air compressors to meet internal ESG targets rather than expanding localized exposure.

* Regulatory & Litigation Backlog: Phihong proactively instituted a strict Internal Carbon Pricing (ICP) mechanism at $96.26 per metric ton to front-run the 2026 EU Carbon Border Adjustment Mechanism (CBAM). Legally, the company is engaged in an offensive trade secret infringement appeal (filed February 9, 2026) to safeguard its proprietary EV power-sharing algorithms.

HDIN Institutional Perspective

While management attributes the FY2025 net margin collapse (-6.48%) to macro-level FX shocks and U.S. EV subsidy shifts, the structural deficit suggests a more fundamental mismatch in operating leverage that the Street is currently underpricing. The intentional phasing out of low-margin legacy EV hardware in late 2025 was a necessary defense against Chinese price dumping, yet the sheer scale of fixed-cost absorption in the newly expanded Tainan and Haiphong facilities remains unproven.

However, Phihong’s explicit refusal to slash its innovation budget during a revenue contraction is a strong signal of structural resilience. The projected $19.85M operational deficit for FY2026 will burn near-term liquidity, but by establishing a decentralized, tariff-resistant supply chain and targeting a 48 million unit volume output, the company is sacrificing immediate Free Cash Flow to build an insurmountable hardware moat. If the company successfully scales its 720kW modular chargers to capture the commercial heavy-duty electrification supercycle, the currently negative operating leverage will violently reverse into outsized profitability.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."