Alchip Technologies: Product Mix Pivot Near Hsinchu Foundry Hub as 354% OCF Surge Signals 2026 AI Margin Expansion

Date : 2026-05-28

Reading : 166

Alchip Technologies’ 2025 filings reveal a masterclass in balance sheet architecture. While top-line revenue contracted 40.5% due to legacy hyperscaler volume roll-offs, a strategic pivot toward 2nm/3nm NRE architectures generated a 354.8% surge in operating cash flow (USD 489.99 million). This cash anomaly, fueled by advance receipts from North American AI clients, effectively functions as zero-cost financing to secure scarce advanced packaging slots. For institutional LPs, this signals a high-quality earnings transition—sacrificing low-margin volume to lock in structural pricing power ahead of the 2026 AI hardware supercycle.

Forensic Analysis: Segmental Incremental Margins & Capital Allocation

A Forensic Analysis of Alchip’s (TWSE: 3661) 2025 financial statements reveals a deliberate decoupling of net income from volume shipments. By aggressively shifting its product mix toward sub-7nm process nodes and High-Performance Computing (HPC) applications, the company achieved massive operational leverage despite a top-line contraction.

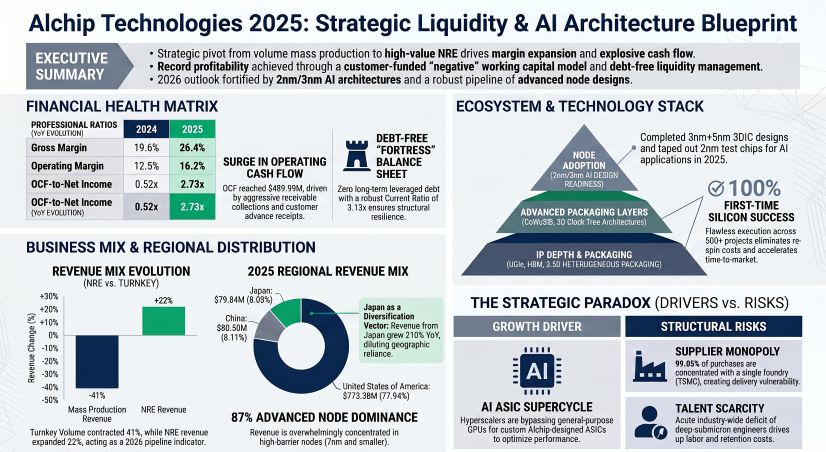

Figure Alchip Technologies 2025: Strategic Liquidity & Al Architecture Blueprint

* Revenue Quality & Price-Mix Variance: Total operating revenue fell to USD 992.29 million, driven by a 41.0% drop in legacy Mass Production (USD 976.92 million) as "Customer A" scaled down orders by 82.1%. Conversely, high-margin Non-Recurring Engineering (NRE) revenue expanded by 22.0% to USD 14.32 million, capturing early-stage 2nm/3nm tape-outs.

* Revenue Quality & Price-Mix Variance: Total operating revenue fell to USD 992.29 million, driven by a 41.0% drop in legacy Mass Production (USD 976.92 million) as "Customer A" scaled down orders by 82.1%. Conversely, high-margin Non-Recurring Engineering (NRE) revenue expanded by 22.0% to USD 14.32 million, capturing early-stage 2nm/3nm tape-outs.

* Margin Expansion Engine: Gross Margin expanded by an aggressive 680 bps to 26.4% (Gross profit: USD 261.64 million). Operating Margin grew 370 bps to 16.2%, aided by a 15.3% reduction in OPEX (USD 100.67 million). Net Profit Margin climbed from 12.4% to 18.1%.

* FCF Conversion & Asset-Light Architecture: The OCF-to-Net Income ratio expanded from a weak 0.52x in 2024 to a formidable 2.73x in 2025. With Capital Expenditure (PP&E) actively shrinking by 5.39% to USD 53.90 million, Alchip converts operating cash directly into Free Cash Flow.

Supply Chain Audit & Geo-Economic Moat

Alchip’s physical operational footprint operates on an extreme edge of the "fabless paradox." The company explicitly maintains a 99.06% supplier reliance on NYSE: TSM (USD 472.75 million in net purchases), presenting a severe single-point-of-failure risk regarding 5nm/3nm node allocation and CoWoS® / InFO packaging capacities.

To circumvent the lack of binding long-term capacity contracts, Alchip leverages its geographic proximity. Operating its ASIC Manufacturing Center in Hsinchu, Taiwan, Province of China, Alchip interfaces directly with Tier-1 foundries, supplying predictive 6-month capacity slots. Globally, the firm is consciously diluting its 77.94% geographic revenue concentration in the United States by scaling alternative R&D and design subsidiaries. In 2025, operations in Yokohama, Japan, yielded a massive 210.0% YoY revenue growth (reaching USD 79.84 million), proving the viability of the Japanese HPC and supercomputing market. Furthermore, Alchip has fortified alternative engineering hubs across San Jose, California, alongside facilities in Penang, Malaysia, and Da Nang, Vietnam, insulating its talent pipeline from the severe regional human capital deficit.

HDIN Institutional Perspective

While consensus models might penalize Alchip for the 40.5% top-line contraction and the hyper-concentration risk of Customer B (which surged 40.8% to capture a 50.14% revenue share), the Street is mispricing the company's liability structure. The 59.1% expansion in current liabilities is an anomaly of strength, entirely funded by "receipts in advance from customers." In an environment constrained by severe CoWoS® bottlenecks, Alchip has forced North American hyper-scalers to finance its balance sheet. This structurally de-risks the USD 277.37 million anticipated material purchasing outflow for 2026 and ensures that Alchip can execute its proprietary 3D LiteIO and 2nm AI accelerator tape-outs with zero reliance on leveraged debt.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Forensic Analysis: Segmental Incremental Margins & Capital Allocation

A Forensic Analysis of Alchip’s (TWSE: 3661) 2025 financial statements reveals a deliberate decoupling of net income from volume shipments. By aggressively shifting its product mix toward sub-7nm process nodes and High-Performance Computing (HPC) applications, the company achieved massive operational leverage despite a top-line contraction.

Figure Alchip Technologies 2025: Strategic Liquidity & Al Architecture Blueprint

* Revenue Quality & Price-Mix Variance: Total operating revenue fell to USD 992.29 million, driven by a 41.0% drop in legacy Mass Production (USD 976.92 million) as "Customer A" scaled down orders by 82.1%. Conversely, high-margin Non-Recurring Engineering (NRE) revenue expanded by 22.0% to USD 14.32 million, capturing early-stage 2nm/3nm tape-outs.* Margin Expansion Engine: Gross Margin expanded by an aggressive 680 bps to 26.4% (Gross profit: USD 261.64 million). Operating Margin grew 370 bps to 16.2%, aided by a 15.3% reduction in OPEX (USD 100.67 million). Net Profit Margin climbed from 12.4% to 18.1%.

* FCF Conversion & Asset-Light Architecture: The OCF-to-Net Income ratio expanded from a weak 0.52x in 2024 to a formidable 2.73x in 2025. With Capital Expenditure (PP&E) actively shrinking by 5.39% to USD 53.90 million, Alchip converts operating cash directly into Free Cash Flow.

Table FY2025 Financial Performance and Advanced Packaging Strategy Analysis

| Metric | 2025 Result (USD) | YoY Variance | Strategic Driver |

|---|---|---|---|

| Total Revenue | $992.29M | -40.5% | Cyclical volume reduction from top hyperscaler client |

| Operating Cash Flow | $489.99M | +354.8% | Accelerated DSO collection and surging customer advance receipts |

| NRE Segment Revenue | $14.32M | +22.0% | Robust 3nm/2nm design demand transitioning to 2026 volume |

| Current Liabilities | $544.65M | +59.1% | Zero-cost NRE pre-funding to secure capacity; not liquidity distress |

| R&D Expenditure | $58.75M | N/A (5.92% of Rev) | Focus on System-on-Wafer (SoW) and 3.5D heterogeneous packaging |

| Net Profit | $179.56M | -13.2% | Offset by $54.65M non-operating income (time deposit interest) |

Supply Chain Audit & Geo-Economic Moat

Alchip’s physical operational footprint operates on an extreme edge of the "fabless paradox." The company explicitly maintains a 99.06% supplier reliance on NYSE: TSM (USD 472.75 million in net purchases), presenting a severe single-point-of-failure risk regarding 5nm/3nm node allocation and CoWoS® / InFO packaging capacities.

To circumvent the lack of binding long-term capacity contracts, Alchip leverages its geographic proximity. Operating its ASIC Manufacturing Center in Hsinchu, Taiwan, Province of China, Alchip interfaces directly with Tier-1 foundries, supplying predictive 6-month capacity slots. Globally, the firm is consciously diluting its 77.94% geographic revenue concentration in the United States by scaling alternative R&D and design subsidiaries. In 2025, operations in Yokohama, Japan, yielded a massive 210.0% YoY revenue growth (reaching USD 79.84 million), proving the viability of the Japanese HPC and supercomputing market. Furthermore, Alchip has fortified alternative engineering hubs across San Jose, California, alongside facilities in Penang, Malaysia, and Da Nang, Vietnam, insulating its talent pipeline from the severe regional human capital deficit.

HDIN Institutional Perspective

While consensus models might penalize Alchip for the 40.5% top-line contraction and the hyper-concentration risk of Customer B (which surged 40.8% to capture a 50.14% revenue share), the Street is mispricing the company's liability structure. The 59.1% expansion in current liabilities is an anomaly of strength, entirely funded by "receipts in advance from customers." In an environment constrained by severe CoWoS® bottlenecks, Alchip has forced North American hyper-scalers to finance its balance sheet. This structurally de-risks the USD 277.37 million anticipated material purchasing outflow for 2026 and ensures that Alchip can execute its proprietary 3D LiteIO and 2nm AI accelerator tape-outs with zero reliance on leveraged debt.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."