NEIS Co., Ltd.: Aggressive Franchise Rollout Near Kanto as 750-bps Margin Expansion Signals Peak Cash Conversion

Date : 2026-05-29

Reading : 152

What does NEIS Co., Ltd.’s $19.09M top-line actually represent for institutional capital? The 23% YoY revenue jump is entirely volume-driven, camouflaging a structural negative working capital cycle where prepaid tuition funds CapEx by a 5.7x ratio. Operating at the intersection of retail foot traffic and Japan’s heavily subsidized $5.9B Child Welfare Act ecosystem, the firm bypasses demographic headwinds. However, with an average instructor tenure of just 2.0 years, this hyper-expansion relies entirely on a precarious 20-day proprietary training pipeline to sustain its sub-$85k unit economics.

Forensic Financials & Segmental Margin Analysis

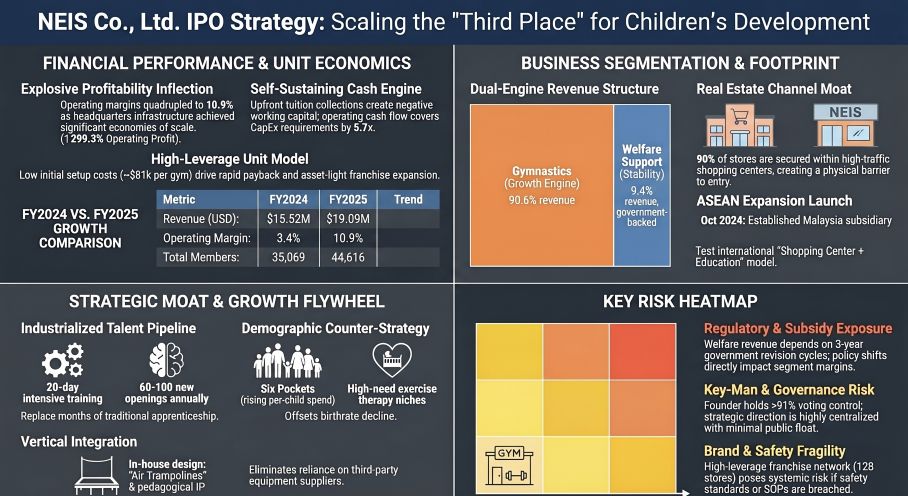

NEIS Co., Ltd. has reached a critical inflection point in its profitability matrix, demonstrating textbook operating leverage as fixed SG&A costs are diluted by rapid franchise onboarding. Growth is completely volume-driven (store count +31.3% YoY, active members +27.2% YoY), rather than relying on ARPU expansion.

Figure NEIS lPO Strategy: Scaling the Third Place for Children's Development

Segmental Incremental Margins:

Segmental Incremental Margins:

* *Children’s Gymnastics:* Generated $17.29M (90.6% of total revenue) in FY2025, up 24.2% YoY.

* *Child Development Support (Welfare):* Generated $1.80M (9.4% of total revenue), growing 12.2% YoY despite zero new store openings in FY2025, signaling higher utilization of existing assets.

* Operating Leverage & Cost Architecture: Gross margins expanded 250 bps to 45.6%, largely driven by instructor labor cost optimization (falling to 49.4% of the $10.38M COGS). A mere 7.4% increase in SG&A ($6.62M) propelled Operating Margins up 750 bps to 10.9% ($2.09M).

* Unit Economics: Initial CapEx is structurally suppressed. A new Gymnastics facility requires merely $81,345, yielding ~$114,500/year at a mass-market ARPU of $59.50/month. A new Welfare facility requires $69,132, yielding ~$180,000/year.

* FCF Conversion & Internal Capital Allocation: The firm operates with $2.41M in Contract Liabilities (prepaid tuition/franchise fees), engineering a negative working capital cycle. Operating Cash Flow ($4.41M) covers total FY2025 CapEx ($0.77M) by an exceptional 5.7x, entirely self-funding the FY2026-FY2028 projection of opening 11-20 direct-operated stores annually.

Physical Footprint Audit & Geo-Economic Moat

The physical manifestation of NEIS Co., Ltd. is distinctly bifurcated between an asset-light, decentralized franchise model and a hyper-dense, direct-operated welfare network.

* Geographic Density & Real Estate Strategy: As of April 2026, the firm operates 188 total facilities (177 Gymnastics, 11 Welfare). The expansion is heavily anchored in the Kanto Region (110 gymnastics locations, 11 welfare locations), with secondary penetration in Chubu (22), Kinki (21), and Kyushu/Okinawa (16). Approximately 90% of locations are strategically embedded within high-traffic shopping centers, weaponizing commercial real estate as a zero-CAC (Customer Acquisition Cost) funnel.

* Supply Chain & Proprietary Hardware: The firm bypasses third-party vendor bottlenecks by utilizing its proprietary, internally designed Air Trampolines and specialized pedagogical IP (the NEIS Method). This vertical integration standardizes physical output across all 128 franchisee-operated stores (managed by 34 separate entities).

* Global Offshoring & Southeast Asia Pivot: To mitigate domestic demographic shrinkage, the firm deployed a $233,595 (1,000,000 MYR) initial capital injection to establish NEIS Gymnastics SDN. BHD. in Kuala Lumpur, Malaysia, in October 2024. This facility acts as the strategic beachhead for testing Southeast Asian compliance, local instructor recruitment, and hardware export logistics.

HDIN Institutional Perspective

While the Street perceives NEIS Co., Ltd. as a consumer-discretionary education play, our Forensic Analysis reveals a highly leveraged real-estate arbitrage and regulatory-capture mechanism. The firm’s rapid 1,000-store vision is financially buoyed by an invisible subsidy: President Yusuke Minami’s zero-fee personal guarantee covering $1.10M in annual rent liabilities across 44 leases. This structurally deflates the firm's WACC and inflates near-term operating profit.

Furthermore, the firm's highest-yielding Welfare segment is exposed to a binary tail-risk: the triennial remuneration revisions mandated by Japan's Child Welfare Act. With 90% of this segment's revenue funded directly by municipal governments (B2G), any macro-level fiscal austerity targeting the $5.9B disabled-child support budget will result in immediate, unhedgeable margin compression. Additionally, the aggressive deployment of the Noren-wake (employee-to-franchisee) system masks a severe labor retention crisis, characterized by a precarious 2.0-year average instructor tenure. If the proprietary 20-day intensive training pipeline fractures, the resulting service degradation across 128 autonomous franchise nodes will trigger catastrophic reputational damage.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Forensic Financials & Segmental Margin Analysis

NEIS Co., Ltd. has reached a critical inflection point in its profitability matrix, demonstrating textbook operating leverage as fixed SG&A costs are diluted by rapid franchise onboarding. Growth is completely volume-driven (store count +31.3% YoY, active members +27.2% YoY), rather than relying on ARPU expansion.

Figure NEIS lPO Strategy: Scaling the Third Place for Children's Development

Segmental Incremental Margins: * *Children’s Gymnastics:* Generated $17.29M (90.6% of total revenue) in FY2025, up 24.2% YoY.

* *Child Development Support (Welfare):* Generated $1.80M (9.4% of total revenue), growing 12.2% YoY despite zero new store openings in FY2025, signaling higher utilization of existing assets.

* Operating Leverage & Cost Architecture: Gross margins expanded 250 bps to 45.6%, largely driven by instructor labor cost optimization (falling to 49.4% of the $10.38M COGS). A mere 7.4% increase in SG&A ($6.62M) propelled Operating Margins up 750 bps to 10.9% ($2.09M).

* Unit Economics: Initial CapEx is structurally suppressed. A new Gymnastics facility requires merely $81,345, yielding ~$114,500/year at a mass-market ARPU of $59.50/month. A new Welfare facility requires $69,132, yielding ~$180,000/year.

* FCF Conversion & Internal Capital Allocation: The firm operates with $2.41M in Contract Liabilities (prepaid tuition/franchise fees), engineering a negative working capital cycle. Operating Cash Flow ($4.41M) covers total FY2025 CapEx ($0.77M) by an exceptional 5.7x, entirely self-funding the FY2026-FY2028 projection of opening 11-20 direct-operated stores annually.

Physical Footprint Audit & Geo-Economic Moat

The physical manifestation of NEIS Co., Ltd. is distinctly bifurcated between an asset-light, decentralized franchise model and a hyper-dense, direct-operated welfare network.

* Geographic Density & Real Estate Strategy: As of April 2026, the firm operates 188 total facilities (177 Gymnastics, 11 Welfare). The expansion is heavily anchored in the Kanto Region (110 gymnastics locations, 11 welfare locations), with secondary penetration in Chubu (22), Kinki (21), and Kyushu/Okinawa (16). Approximately 90% of locations are strategically embedded within high-traffic shopping centers, weaponizing commercial real estate as a zero-CAC (Customer Acquisition Cost) funnel.

* Supply Chain & Proprietary Hardware: The firm bypasses third-party vendor bottlenecks by utilizing its proprietary, internally designed Air Trampolines and specialized pedagogical IP (the NEIS Method). This vertical integration standardizes physical output across all 128 franchisee-operated stores (managed by 34 separate entities).

* Global Offshoring & Southeast Asia Pivot: To mitigate domestic demographic shrinkage, the firm deployed a $233,595 (1,000,000 MYR) initial capital injection to establish NEIS Gymnastics SDN. BHD. in Kuala Lumpur, Malaysia, in October 2024. This facility acts as the strategic beachhead for testing Southeast Asian compliance, local instructor recruitment, and hardware export logistics.

HDIN Institutional Perspective

While the Street perceives NEIS Co., Ltd. as a consumer-discretionary education play, our Forensic Analysis reveals a highly leveraged real-estate arbitrage and regulatory-capture mechanism. The firm’s rapid 1,000-store vision is financially buoyed by an invisible subsidy: President Yusuke Minami’s zero-fee personal guarantee covering $1.10M in annual rent liabilities across 44 leases. This structurally deflates the firm's WACC and inflates near-term operating profit.

Furthermore, the firm's highest-yielding Welfare segment is exposed to a binary tail-risk: the triennial remuneration revisions mandated by Japan's Child Welfare Act. With 90% of this segment's revenue funded directly by municipal governments (B2G), any macro-level fiscal austerity targeting the $5.9B disabled-child support budget will result in immediate, unhedgeable margin compression. Additionally, the aggressive deployment of the Noren-wake (employee-to-franchisee) system masks a severe labor retention crisis, characterized by a precarious 2.0-year average instructor tenure. If the proprietary 20-day intensive training pipeline fractures, the resulting service degradation across 128 autonomous franchise nodes will trigger catastrophic reputational damage.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."