Prefabricated Construction 2026 Outlook: Why Champion Homes, Cavco Industries & China Railway Prefabricated Construction Diverge on Factory Automation Amid Fragmented Zoning Regulations

Date : 2026-05-29

Reading : 287

Our research evaluating the 2025–2026 modular construction sector must recognize a stark divergence in capital velocity. While GSE financing and §45L tax credits drive robust cash conversion for decentralized U.S. manufacturers, aggressive factory automation models face systemic collapse against localized zoning bottlenecks. Concurrently, China's state-mandated 30% prefabrication floor creates artificial revenue certainty for captive B2G suppliers. The defining 2026 performance metric is not maximum factory throughput, but the precise synchronization of upstream manufacturing with downstream site-readiness and localized regulatory approvals.

Forensic Financials & Segmental Inventory Dynamics

A forensic analysis of FY2025 filings exposes severe spreads in Peer-Group ROIC, capital velocity, and earnings quality across the sector. Operating leverage currently favors decentralized mass customization over hyper-centralized standardization.

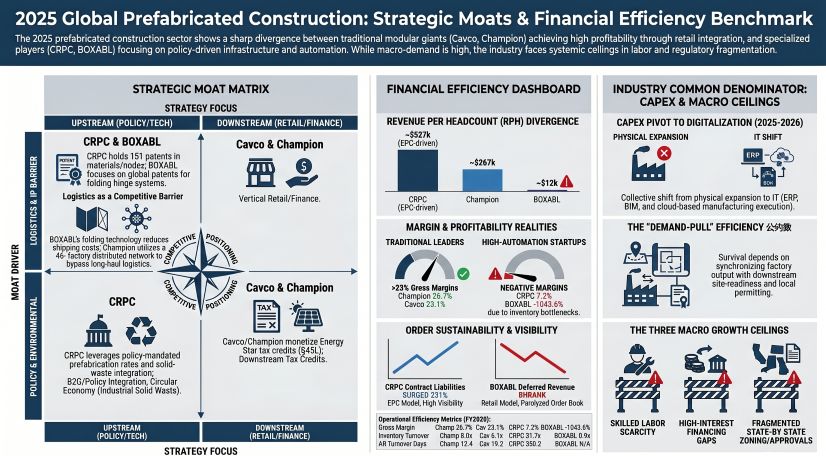

Figure 2025 Global Prefabricated Construction: Strategic Moats & Financial Efficiency Benchmark

Champion Homes (NYSE: SKY): The Cash Conversion Benchmark

Champion Homes (NYSE: SKY): The Cash Conversion Benchmark

* Unit Economics: Generated $2.48 billion in revenue with an industry-leading 26.7% gross margin. CFO-to-Net-Income conversion sits at an optimal 1.19x ($240.9M CFO vs. $198.4M NI).

* Inventory Velocity: Achieved an inventory turnover of ~5.0x with near-zero finished goods trapped on the balance sheet. Deliveries operate on a strict 90-day fulfillment cycle against a highly diversified $316.0M backlog.

* CapEx Realignment: Allocated $34.1M for FY2026, pivoting away from physical expansion toward cloud-based execution platforms and targeted component automation to mitigate structural labor shortages.

Cavco Industries (NASDAQ: CVCO): Regulatory Monetization

* Margin Subsidization: Reported 23.1% gross margins on $2.01 billion in revenue, heavily optimized by a $5.4M YoY increase in energy tax credits (totaling $10.5M under U.S. IRC §45L).

* Off-Balance-Sheet Risk: Operates with ~$19.2 days AR turnover, though reliant on dealer floor-plan financing that includes contingent repurchase agreements.

* China Railway Prefabricated Construction (SZSE: 300374): Capital-Intensive B2G Integration

* Revenue Quality & RPT: Recorded $267.2M in revenue (1 USD = 7.1875 CNY) at a compressed 7.2% gross margin. True market competitiveness is masked by extreme concentration risk: 61.45% of top-five customer revenue, with 51.34% originating from related-party transactions (RPT) within its parent ecosystem.

* Working Capital Engineering: While reporting a net loss of -$16.8M, the firm engineered a positive CFO of +$20.8M via off-balance-sheet asset securitization ($3.0M AR de-recognized) and supplier-side supply chain financing. However, a 231% surge in contract liabilities ($29.47M) signals robust advanced payments for state-backed EPC contracts.

Boxabl (Private): The Automation Paradox

* Margin Collapse: Posted a catastrophic -1043.6% gross margin ($15.8M gross loss on $1.5M revenue) and a net loss of -$57.5M, sustained entirely by $55.6M in continuous Series A/Regulation D equity financing.

* Inventory Obsolescence: Extreme absolute standardization without localized regulatory compliance resulted in 175 trapped units and an $8.4M inventory write-down for 68 units rendered obsolete by climate-zone non-compliance. Revenue-per-Headcount collapsed to just $11,828.

Supply Chain Audit & Geo-Economic Moat

Physicality and geographic layout dictate unit profitability. The sector is sharply divided between closed-loop material integration and downstream logistics ownership.

* Distributed Networks vs. Single-Node Failure: NYSE: SKY insulates itself from high long-haul freight costs via a highly distributed 46-facility footprint spanning 20 U.S. states and British Columbia, augmented by its captive Star Fleet Trucking logistics arm. Conversely, Boxabl’s reliance on a singular North Las Vegas, Nevada mega-factory severely exposes it to long-distance shipping economics and fragmented state-by-state approvals (evidenced by recent permit revocations in Arizona).

* Proprietary Midstream Integration: SZSE: 300374 has established a formidable circular-economy moat via its Beijing, Suqian (Jiangsu), and Xinjiang Tier-1 cloud factories. By integrating Solid Waste Geopolymer Lightweight Partition Boards into its raw material supply, it systematically secures heavy infrastructure bids (e.g., Nanjing North Station, Kunming Changshui Airport GTC) mandated by China’s aggressive 2025 prefabrication floors (100% in Guangzhou, 40% in Chongqing).

* Tariff Vulnerability & Sourcing: While traditional builders hedge commodity volatility (lumber, OSB) through downstream pricing pass-throughs, early-stage modular startups utilizing advanced composites face severe import vulnerabilities. Boxabl cited restrictive U.S. government tariffs on foreign materials as the primary catalyst for internalizing light-gauge steel framing production domestically.

HDIN Institutional Perspective

The Street fundamentally misprices the "tech-valuation" of highly automated modular startups. Absolute standardization (the automotive-widget model) creates an illusion of scale that shatters upon contact with fragmented municipal zoning. Automation only yields margin expansion when perfectly synchronized with site-readiness. Traditional manufacturers executing computer-aided "Mass Customization"—generating $267,000+ in revenue per headcount without massive fixed CNC overhead—offer superior, risk-adjusted free cash flow conversion. Furthermore, the reliance of B2G players on internal related-party transactions (accounting for over 50% of revenue) warrants a strict discount on top-line backlog figures, as these do not reflect open-market pricing power.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

Forensic Financials & Segmental Inventory Dynamics

A forensic analysis of FY2025 filings exposes severe spreads in Peer-Group ROIC, capital velocity, and earnings quality across the sector. Operating leverage currently favors decentralized mass customization over hyper-centralized standardization.

Figure 2025 Global Prefabricated Construction: Strategic Moats & Financial Efficiency Benchmark

Champion Homes (NYSE: SKY): The Cash Conversion Benchmark* Unit Economics: Generated $2.48 billion in revenue with an industry-leading 26.7% gross margin. CFO-to-Net-Income conversion sits at an optimal 1.19x ($240.9M CFO vs. $198.4M NI).

* Inventory Velocity: Achieved an inventory turnover of ~5.0x with near-zero finished goods trapped on the balance sheet. Deliveries operate on a strict 90-day fulfillment cycle against a highly diversified $316.0M backlog.

* CapEx Realignment: Allocated $34.1M for FY2026, pivoting away from physical expansion toward cloud-based execution platforms and targeted component automation to mitigate structural labor shortages.

Cavco Industries (NASDAQ: CVCO): Regulatory Monetization

* Margin Subsidization: Reported 23.1% gross margins on $2.01 billion in revenue, heavily optimized by a $5.4M YoY increase in energy tax credits (totaling $10.5M under U.S. IRC §45L).

* Off-Balance-Sheet Risk: Operates with ~$19.2 days AR turnover, though reliant on dealer floor-plan financing that includes contingent repurchase agreements.

* China Railway Prefabricated Construction (SZSE: 300374): Capital-Intensive B2G Integration

* Revenue Quality & RPT: Recorded $267.2M in revenue (1 USD = 7.1875 CNY) at a compressed 7.2% gross margin. True market competitiveness is masked by extreme concentration risk: 61.45% of top-five customer revenue, with 51.34% originating from related-party transactions (RPT) within its parent ecosystem.

* Working Capital Engineering: While reporting a net loss of -$16.8M, the firm engineered a positive CFO of +$20.8M via off-balance-sheet asset securitization ($3.0M AR de-recognized) and supplier-side supply chain financing. However, a 231% surge in contract liabilities ($29.47M) signals robust advanced payments for state-backed EPC contracts.

Boxabl (Private): The Automation Paradox

* Margin Collapse: Posted a catastrophic -1043.6% gross margin ($15.8M gross loss on $1.5M revenue) and a net loss of -$57.5M, sustained entirely by $55.6M in continuous Series A/Regulation D equity financing.

* Inventory Obsolescence: Extreme absolute standardization without localized regulatory compliance resulted in 175 trapped units and an $8.4M inventory write-down for 68 units rendered obsolete by climate-zone non-compliance. Revenue-per-Headcount collapsed to just $11,828.

Supply Chain Audit & Geo-Economic Moat

Physicality and geographic layout dictate unit profitability. The sector is sharply divided between closed-loop material integration and downstream logistics ownership.

* Distributed Networks vs. Single-Node Failure: NYSE: SKY insulates itself from high long-haul freight costs via a highly distributed 46-facility footprint spanning 20 U.S. states and British Columbia, augmented by its captive Star Fleet Trucking logistics arm. Conversely, Boxabl’s reliance on a singular North Las Vegas, Nevada mega-factory severely exposes it to long-distance shipping economics and fragmented state-by-state approvals (evidenced by recent permit revocations in Arizona).

* Proprietary Midstream Integration: SZSE: 300374 has established a formidable circular-economy moat via its Beijing, Suqian (Jiangsu), and Xinjiang Tier-1 cloud factories. By integrating Solid Waste Geopolymer Lightweight Partition Boards into its raw material supply, it systematically secures heavy infrastructure bids (e.g., Nanjing North Station, Kunming Changshui Airport GTC) mandated by China’s aggressive 2025 prefabrication floors (100% in Guangzhou, 40% in Chongqing).

* Tariff Vulnerability & Sourcing: While traditional builders hedge commodity volatility (lumber, OSB) through downstream pricing pass-throughs, early-stage modular startups utilizing advanced composites face severe import vulnerabilities. Boxabl cited restrictive U.S. government tariffs on foreign materials as the primary catalyst for internalizing light-gauge steel framing production domestically.

HDIN Institutional Perspective

The Street fundamentally misprices the "tech-valuation" of highly automated modular startups. Absolute standardization (the automotive-widget model) creates an illusion of scale that shatters upon contact with fragmented municipal zoning. Automation only yields margin expansion when perfectly synchronized with site-readiness. Traditional manufacturers executing computer-aided "Mass Customization"—generating $267,000+ in revenue per headcount without massive fixed CNC overhead—offer superior, risk-adjusted free cash flow conversion. Furthermore, the reliance of B2G players on internal related-party transactions (accounting for over 50% of revenue) warrants a strict discount on top-line backlog figures, as these do not reflect open-market pricing power.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*