Fuji Seiko: Strategic Capacity Pivot Near Toyota City Headquarters as Robust FCF Conversion Signals Transitional Margin Recovery

Date : 2026-05-29

Reading : 133

Fuji Seiko’s FY2026 structural realignment highlights a severe automotive supply chain inflection point. Faced with collapsing internal combustion engine (ICE) tooling demand and Chinese Tungsten export controls, the company stabilized its $136.83 million top-line through customized EV-tooling adaptations and strategic cross-shareholdings with major automotive OEMs. For institutional LPs, the critical narrative lies in the divergence between a robust $5.54 million Free Cash Flow—bolstered by a Guangzhou asset divestiture—and a fragile 1.1% core operating margin. This signals that while balance sheet liquidity is pristine, core operational unit economics remain under extreme transitional pressure.

Forensic Financials & Segmental Inventory: Capital Allocation Under ICE-to-EV Stress

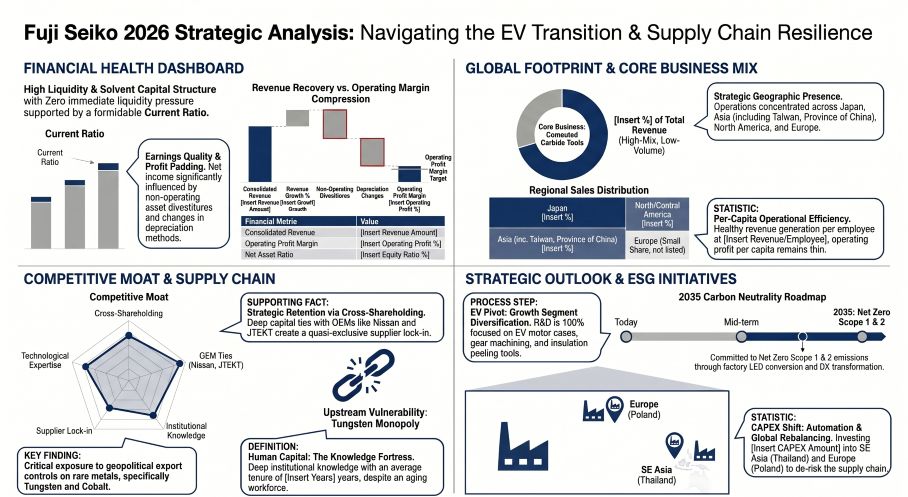

A forensic analysis of TYO: 6140 reveals a business executing heavy internal capital reallocation to mask structural decay in its legacy ICE tool segment. While the company reversed FY2025’s massive $20.85 million impairment loss to post a $4.63 million net income in FY2026, earnings quality is heavily diluted. Over 63% of the $7.49 million pre-tax profit was generated via non-operating channels, specifically a $3.38 million gain from divesting the Guangzhou subsidiary and $1.37 million from investment securities liquidation.

Operating leverage remains severely constrained by price-mix variance, as downstream automakers demand aggressive cost-downs. At a per-capita level across its 1,169-person global workforce, the company generates a healthy $117,049 in revenue but a meager $1,334 in core operating profit, highlighting intense Cost of Goods Sold (COGS) pressures (COGS currently consumes 77% of revenue).

Figure Fuji Seiko 2026 Strategic Analysis: Navigating the EV Transition & Supply Chain Resilience

FY2026 Quantitative Inventory & Segmental Unit Economics:

FY2026 Quantitative Inventory & Segmental Unit Economics:

* Segmental Revenue: Carbide Tools ($109.9M / 80.3%), Packaging Materials ($17.45M / 12.8%), Others ($7.21M / 5.3%), Auto Parts ($2.25M / 1.6%).

* Balance Sheet Liquidity: $63.89 million in Cash & Equivalents dwarfs $5.48 million in short-term borrowings, yielding a formidable Current Ratio of 5.14x.

* Inventory & Receivables: Total inventory sits at $17.09 million (62.7 turnover days), with an immaterial deferred tax effect of $0.13 million on valuation losses. Trade receivables ($23.60 million / 63.2 days) show zero structural risk, backed by a microscopic $0.26 million bad debt provision (1.1% coverage ratio).

* Internal Capital Allocation (Shareholder Returns): Dividend cut from 50 JPY to 15 JPY per share ($0.60M payout), aggressively offset by $3.13 million in buybacks (383,101 shares), a cancellation of 700,000 treasury shares ($6.55 million value) in April 2026, and a new authorization for a $3.11 million repurchase program.

* Off-Balance-Sheet & Contingencies: Zero pending litigation and zero FX derivative exposure, leaving overseas revenues fully exposed to raw JPY currency translation fluctuations.

Supply Chain Audit & Geo-Economic Moat: Evading the Tungsten Chokepoint

Fuji Seiko’s physical supply chain is currently trapped in a geopolitical crossfire. The company's highest-severity operational risk stems from absolute dependence on geographically concentrated rare earth metals—specifically Tungsten and Cobalt—for its cemented carbide tooling. Chinese export controls have injected acute instability into this procurement channel, rendering the $105.22 million COGS highly vulnerable to raw material inflation. Furthermore, the specter of 2025 US trade tariffs threatens its North American automotive clients' CAPEX cycles.

To insulate its operations, management is executing a rapid near-shoring and "friend-shoring" CAPEX realignment. FY2027 approved capital expenditures ($3.20 million) signal a direct pivot away from China.

Global Physical Footprint & CAPEX Trajectory:

* Japan (The R&D Core): $1.26 million allocated for FY2027 IT infrastructure (DX) and automated manufacturing upgrades at the Toyota City Headquarters (Aichi), alongside the Kumamoto (Ozu) and Kagoshima (Kirishima) facilities.

* Southeast Asia (The Growth Hub): $0.86 million directed to Fuji Seiko Thailand in Ayutthaya for capacity expansion slated for completion between April and August 2026, explicitly to capture Japanese OEM electric transition demands. Other active Asian nodes include Cheonan (South Korea), Indonesia, and India.

* North America & Europe (Proximity Assets): Direct localized engineering support via Lexington, Kentucky, and Aguascalientes, Mexico. In Europe, $0.45 million is earmarked for the Accurom Central Europe facility in Poland for ultra-hard tool expansion by June 2026.

* ESG Compliance Deadline: CAPEX is also aligned with the corporate mandate to achieve Scope 1 and Scope 2 Carbon Neutrality by 2035 via systemic facility upgrades.

HDIN Institutional Perspective

Management attributes its survival in the EV transition to a robust technological moat driven by innovations like the 5μm-precision centering arbors and G-one boring tools for motor case machining. However, HDIN Research assesses this claim with skepticism. The company’s R&D expenditure is a mere $0.66 million (0.5% of revenue). In a capital-intensive materials science sector, this budget is structurally incapable of engineering an alternative to Tungsten-carbide or directly challenging lithium-ion battery manufacturing equipment incumbents.

Instead, Fuji Seiko’s true defensible moat is Capital-Integrated Customer Stickiness. The company actively injects capital into the "Supplier Shareholding Associations" of core Tier-1 and OEM clients, holding $19.82 million in strategic shares of entities like TYO: 7201 (Nissan), TYO: 6473 (JTEKT), TYO: 7259 (Aisan Industry), TYO: 6470 (Taiho Kogyo), and TYO: 6218 (Enshu). It simultaneously maintains cross-shareholdings with industry peers TYO: 6136 (OSG), TYO: 5711 (Mitsubishi Materials), and TYO: 6278 (Union Tool). This embedded financial architecture—not the 0.5% R&D budget—creates quasi-exclusive transactional stickiness, providing a vital structural buffer against the ruthless OEM price wars currently reshaping the automotive supply chain.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Forensic Financials & Segmental Inventory: Capital Allocation Under ICE-to-EV Stress

A forensic analysis of TYO: 6140 reveals a business executing heavy internal capital reallocation to mask structural decay in its legacy ICE tool segment. While the company reversed FY2025’s massive $20.85 million impairment loss to post a $4.63 million net income in FY2026, earnings quality is heavily diluted. Over 63% of the $7.49 million pre-tax profit was generated via non-operating channels, specifically a $3.38 million gain from divesting the Guangzhou subsidiary and $1.37 million from investment securities liquidation.

Operating leverage remains severely constrained by price-mix variance, as downstream automakers demand aggressive cost-downs. At a per-capita level across its 1,169-person global workforce, the company generates a healthy $117,049 in revenue but a meager $1,334 in core operating profit, highlighting intense Cost of Goods Sold (COGS) pressures (COGS currently consumes 77% of revenue).

Figure Fuji Seiko 2026 Strategic Analysis: Navigating the EV Transition & Supply Chain Resilience

FY2026 Quantitative Inventory & Segmental Unit Economics:* Segmental Revenue: Carbide Tools ($109.9M / 80.3%), Packaging Materials ($17.45M / 12.8%), Others ($7.21M / 5.3%), Auto Parts ($2.25M / 1.6%).

* Balance Sheet Liquidity: $63.89 million in Cash & Equivalents dwarfs $5.48 million in short-term borrowings, yielding a formidable Current Ratio of 5.14x.

* Inventory & Receivables: Total inventory sits at $17.09 million (62.7 turnover days), with an immaterial deferred tax effect of $0.13 million on valuation losses. Trade receivables ($23.60 million / 63.2 days) show zero structural risk, backed by a microscopic $0.26 million bad debt provision (1.1% coverage ratio).

* Internal Capital Allocation (Shareholder Returns): Dividend cut from 50 JPY to 15 JPY per share ($0.60M payout), aggressively offset by $3.13 million in buybacks (383,101 shares), a cancellation of 700,000 treasury shares ($6.55 million value) in April 2026, and a new authorization for a $3.11 million repurchase program.

* Off-Balance-Sheet & Contingencies: Zero pending litigation and zero FX derivative exposure, leaving overseas revenues fully exposed to raw JPY currency translation fluctuations.

Supply Chain Audit & Geo-Economic Moat: Evading the Tungsten Chokepoint

Fuji Seiko’s physical supply chain is currently trapped in a geopolitical crossfire. The company's highest-severity operational risk stems from absolute dependence on geographically concentrated rare earth metals—specifically Tungsten and Cobalt—for its cemented carbide tooling. Chinese export controls have injected acute instability into this procurement channel, rendering the $105.22 million COGS highly vulnerable to raw material inflation. Furthermore, the specter of 2025 US trade tariffs threatens its North American automotive clients' CAPEX cycles.

To insulate its operations, management is executing a rapid near-shoring and "friend-shoring" CAPEX realignment. FY2027 approved capital expenditures ($3.20 million) signal a direct pivot away from China.

Global Physical Footprint & CAPEX Trajectory:

* Japan (The R&D Core): $1.26 million allocated for FY2027 IT infrastructure (DX) and automated manufacturing upgrades at the Toyota City Headquarters (Aichi), alongside the Kumamoto (Ozu) and Kagoshima (Kirishima) facilities.

* Southeast Asia (The Growth Hub): $0.86 million directed to Fuji Seiko Thailand in Ayutthaya for capacity expansion slated for completion between April and August 2026, explicitly to capture Japanese OEM electric transition demands. Other active Asian nodes include Cheonan (South Korea), Indonesia, and India.

* North America & Europe (Proximity Assets): Direct localized engineering support via Lexington, Kentucky, and Aguascalientes, Mexico. In Europe, $0.45 million is earmarked for the Accurom Central Europe facility in Poland for ultra-hard tool expansion by June 2026.

* ESG Compliance Deadline: CAPEX is also aligned with the corporate mandate to achieve Scope 1 and Scope 2 Carbon Neutrality by 2035 via systemic facility upgrades.

HDIN Institutional Perspective

Management attributes its survival in the EV transition to a robust technological moat driven by innovations like the 5μm-precision centering arbors and G-one boring tools for motor case machining. However, HDIN Research assesses this claim with skepticism. The company’s R&D expenditure is a mere $0.66 million (0.5% of revenue). In a capital-intensive materials science sector, this budget is structurally incapable of engineering an alternative to Tungsten-carbide or directly challenging lithium-ion battery manufacturing equipment incumbents.

Instead, Fuji Seiko’s true defensible moat is Capital-Integrated Customer Stickiness. The company actively injects capital into the "Supplier Shareholding Associations" of core Tier-1 and OEM clients, holding $19.82 million in strategic shares of entities like TYO: 7201 (Nissan), TYO: 6473 (JTEKT), TYO: 7259 (Aisan Industry), TYO: 6470 (Taiho Kogyo), and TYO: 6218 (Enshu). It simultaneously maintains cross-shareholdings with industry peers TYO: 6136 (OSG), TYO: 5711 (Mitsubishi Materials), and TYO: 6278 (Union Tool). This embedded financial architecture—not the 0.5% R&D budget—creates quasi-exclusive transactional stickiness, providing a vital structural buffer against the ruthless OEM price wars currently reshaping the automotive supply chain.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."