American Superconductor Corporation: Inorganic Expansion Near Paraná Manufacturing Hub as 34% Top-Line Growth Signals Margin Inflection

Date : 2026-06-01

Reading : 115

American Superconductor Corporation's FY2026 transition to positive operating margins masks a complex structural reality. While a $118.4 million deferred tax valuation reversal signals internal confidence in sustained profitability, a dismal 0.17x earnings-to-cash conversion ratio exposes tight working capital dynamics. For institutional LPs, the immediate value driver is physical capacity expansion in South America, not legacy proprietary moats. However, structural counterparty vulnerabilities—specifically a 15% revenue concentration with India-based Inox Wind and punitive U.S. defense contracting penalty exposures—threaten backlog realization amid the looming February 2026 global tariff implementation.

Forensic Financials & Segmental Margin Architecture

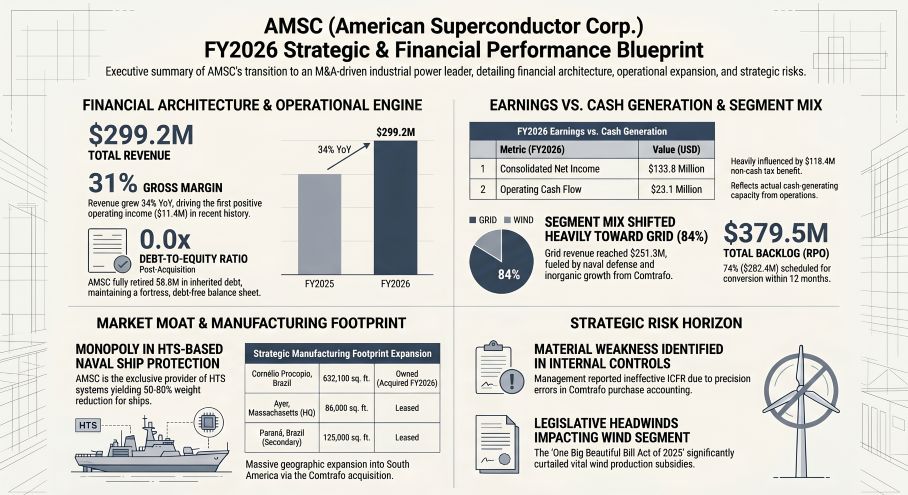

A Forensic Analysis of NASDAQ: AMSC reveals a highly bifurcated operating model heavily skewed toward its Grid segment following the strategic $202.9 million acquisition of Comtrafo and the $61.4 million acquisition of NWL. Top-line expansion demonstrates robust operating leverage, yet statutory Net Income drastically overstates current operational cash generation due to M&A accounting and structural tax shield integrations.

Figure AMSC (American Superconductor Corp)-FY2026 Strategic & Financial Performance Blueprint

FY2026 Segmental Inventory & Profitability Baseline:

FY2026 Segmental Inventory & Profitability Baseline:

* Consolidated Revenue: $299.2 million (+105% aggregate increase since FY2024; +34% YoY).

* Grid Segment (84% of Mix): Generated $251.3 million (+34% YoY) with an operating income of $8.47 million.

* Wind Segment (16% of Mix): Generated $47.8 million (+34% YoY) with an operating income of $7.15 million.

* Operating Leverage: Gross margins expanded by 630 bps over a three-year horizon, reaching 30.5% in FY2026. Consolidated operating margins flipped from -0.5% (FY2025) to +3.8% (FY2026), generating $11.4 million in operating income despite a 34% surge in SG&A to $57.6 million.

* Quality of Earnings & FCF Conversion: Net Income printed at an artificially inflated $133.8 million, driven almost entirely by a $118.4 million non-cash deferred income tax benefit following the release of valuation allowances against U.S. Deferred Tax Assets (DTAs). Actual Operating Cash Flow (OCF) stood at just $23.1 million, resulting in a weak 0.17x cash conversion ratio.

* Capital Structure & Solvency: The balance sheet operates with a 0.0x Debt-to-Equity ratio. The June 2025 public offering injected $124.6 million in net proceeds, yielding a highly liquid Current Ratio of 2.39x ($331.7 million in current assets).

* Backlog Conversion Risk: The $379.5 million Remaining Performance Obligation (RPO) is highly front-loaded, with $282.4 million slated for recognition within 12 months. However, unbilled accounts receivable surged 133% to $14.88 million, indicating an increased reliance on cost-to-cost percentage-of-completion revenue recognition ahead of customer billing.

Supply Chain Audit & Geo-Economic Moat: The Brazilian Realignment

AMSC is aggressively pivoting away from a strictly North American, asset-light assembly model toward a heavy-industrial, distributed global footprint. This physicality fundamentally alters the company's risk matrix and supply chain dependencies.

* Manufacturing Real Estate Footprint: The operational center of gravity for heavy transformer manufacturing has shifted to the Cornélio Procópio Tier-1 Facility in Paraná, Brazil. Following the Comtrafo integration, AMSC controls a 632,100 sq. ft. owned facility and a 125,000 sq. ft. leased site, fortified by post-acquisition real estate cash deployments totaling $6.66 million (37.2 million BRL) in May 2026.

* Intellectual & Engineering Hubs: R&D and core engineering are isolated geographically at the Ayer, MA Headquarters, the Richland, WA systems facility, and the Klagenfurt Engineering Hub in Austria, which supports European wind turbine design.

* Critical Input Bottlenecks: The production of the proprietary Amperium high-temperature superconductor (YBCO) wire and power electronics relies heavily on constrained strategic metals: nickel, silver, yttrium, copper, brass, and stainless steel, alongside complex subassemblies like insulated gate bi-polar transistors (IGBTs).

* Geo-Economic Headwinds: The supply chain faces existential margin threats from the invocation of the U.S. Trade Act of 1974. The planned imposition of a 10% global import tariff in February 2026 will directly inflate the cost of goods sold for imported raw materials. Concurrently, geopolitical conflicts in the Middle East and Eastern Europe continue to sustain premium pricing for copper and nickel.

HDIN Institutional Perspective

While the FY2026 filings project extreme optimism regarding AI-driven grid modernization and naval defense contracts—specifically the integration of Ship Protection Systems (SPS) across the 364-ship U.S. Navy expansion plan—the Street is fundamentally mispricing the downside regulatory risks attached to this revenue.

Our Differentiated Viewpoint confirms that AMSC’s pivot to physical industrial capacity (via Comtrafo) is strategically sound for gross margin protection, but the Wind segment faces near-terminal legislative headwinds. The passage of the U.S. "One Big Beautiful Bill Act of 2025" (OBBBA), which gutted the Production Tax Credit (PTC) and Inflation Reduction Act (IRA) subsidies, destroys the organic domestic growth thesis for the Wind division. Furthermore, the January 2026 U.S. Executive Order, "Prioritizing the Warfighter in Defense Contracting," exposes AMSC to severe, unprecedented penalties—including stock repurchase bans and executive salary caps—should the Secretary of Defense classify AMSC as "Underperforming." Coupled with a formally recognized material weakness in Internal Control over Financial Reporting (ICFR) regarding Comtrafo's purchase accounting, institutional capital must aggressively discount AMSC’s $379.5 million backlog for execution risk.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

Forensic Financials & Segmental Margin Architecture

A Forensic Analysis of NASDAQ: AMSC reveals a highly bifurcated operating model heavily skewed toward its Grid segment following the strategic $202.9 million acquisition of Comtrafo and the $61.4 million acquisition of NWL. Top-line expansion demonstrates robust operating leverage, yet statutory Net Income drastically overstates current operational cash generation due to M&A accounting and structural tax shield integrations.

Figure AMSC (American Superconductor Corp)-FY2026 Strategic & Financial Performance Blueprint

FY2026 Segmental Inventory & Profitability Baseline:* Consolidated Revenue: $299.2 million (+105% aggregate increase since FY2024; +34% YoY).

* Grid Segment (84% of Mix): Generated $251.3 million (+34% YoY) with an operating income of $8.47 million.

* Wind Segment (16% of Mix): Generated $47.8 million (+34% YoY) with an operating income of $7.15 million.

* Operating Leverage: Gross margins expanded by 630 bps over a three-year horizon, reaching 30.5% in FY2026. Consolidated operating margins flipped from -0.5% (FY2025) to +3.8% (FY2026), generating $11.4 million in operating income despite a 34% surge in SG&A to $57.6 million.

* Quality of Earnings & FCF Conversion: Net Income printed at an artificially inflated $133.8 million, driven almost entirely by a $118.4 million non-cash deferred income tax benefit following the release of valuation allowances against U.S. Deferred Tax Assets (DTAs). Actual Operating Cash Flow (OCF) stood at just $23.1 million, resulting in a weak 0.17x cash conversion ratio.

* Capital Structure & Solvency: The balance sheet operates with a 0.0x Debt-to-Equity ratio. The June 2025 public offering injected $124.6 million in net proceeds, yielding a highly liquid Current Ratio of 2.39x ($331.7 million in current assets).

* Backlog Conversion Risk: The $379.5 million Remaining Performance Obligation (RPO) is highly front-loaded, with $282.4 million slated for recognition within 12 months. However, unbilled accounts receivable surged 133% to $14.88 million, indicating an increased reliance on cost-to-cost percentage-of-completion revenue recognition ahead of customer billing.

Supply Chain Audit & Geo-Economic Moat: The Brazilian Realignment

AMSC is aggressively pivoting away from a strictly North American, asset-light assembly model toward a heavy-industrial, distributed global footprint. This physicality fundamentally alters the company's risk matrix and supply chain dependencies.

* Manufacturing Real Estate Footprint: The operational center of gravity for heavy transformer manufacturing has shifted to the Cornélio Procópio Tier-1 Facility in Paraná, Brazil. Following the Comtrafo integration, AMSC controls a 632,100 sq. ft. owned facility and a 125,000 sq. ft. leased site, fortified by post-acquisition real estate cash deployments totaling $6.66 million (37.2 million BRL) in May 2026.

* Intellectual & Engineering Hubs: R&D and core engineering are isolated geographically at the Ayer, MA Headquarters, the Richland, WA systems facility, and the Klagenfurt Engineering Hub in Austria, which supports European wind turbine design.

* Critical Input Bottlenecks: The production of the proprietary Amperium high-temperature superconductor (YBCO) wire and power electronics relies heavily on constrained strategic metals: nickel, silver, yttrium, copper, brass, and stainless steel, alongside complex subassemblies like insulated gate bi-polar transistors (IGBTs).

* Geo-Economic Headwinds: The supply chain faces existential margin threats from the invocation of the U.S. Trade Act of 1974. The planned imposition of a 10% global import tariff in February 2026 will directly inflate the cost of goods sold for imported raw materials. Concurrently, geopolitical conflicts in the Middle East and Eastern Europe continue to sustain premium pricing for copper and nickel.

HDIN Institutional Perspective

While the FY2026 filings project extreme optimism regarding AI-driven grid modernization and naval defense contracts—specifically the integration of Ship Protection Systems (SPS) across the 364-ship U.S. Navy expansion plan—the Street is fundamentally mispricing the downside regulatory risks attached to this revenue.

Our Differentiated Viewpoint confirms that AMSC’s pivot to physical industrial capacity (via Comtrafo) is strategically sound for gross margin protection, but the Wind segment faces near-terminal legislative headwinds. The passage of the U.S. "One Big Beautiful Bill Act of 2025" (OBBBA), which gutted the Production Tax Credit (PTC) and Inflation Reduction Act (IRA) subsidies, destroys the organic domestic growth thesis for the Wind division. Furthermore, the January 2026 U.S. Executive Order, "Prioritizing the Warfighter in Defense Contracting," exposes AMSC to severe, unprecedented penalties—including stock repurchase bans and executive salary caps—should the Secretary of Defense classify AMSC as "Underperforming." Coupled with a formally recognized material weakness in Internal Control over Financial Reporting (ICFR) regarding Comtrafo's purchase accounting, institutional capital must aggressively discount AMSC’s $379.5 million backlog for execution risk.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*