Maxvax Biotechnology: 60,000-Sqm CAPEX Activation Near Shanghai Lingang Special Area as MKK100 NDA Progression Signals Disruption in $1.75B Premium Adult Vaccine Market

Date : 2026-06-01

Reading : 137

Maxvax Biotechnology’s 100% R&D expensing policy masks aggressive commercialization mechanics ahead of its $407.52 million IPO. With the MKK100 shingles vaccine entering NDA review, the firm is pivoting from a pre-revenue biotech reliant on veterinary adjuvant sales ($3.11 million top-line) to a biopharma challenger targeting GSK’s domestic oligopoly. For institutional LPs, the critical variable is securing the QS-21 saponin supply chain against geopolitical friction, justifying the massive capital allocation toward the Shanghai Lingang manufacturing hub to guarantee internal autonomy and batch-to-batch structural integrity.

Forensic Financials & Capital Allocation of Maxvax Biotechnology

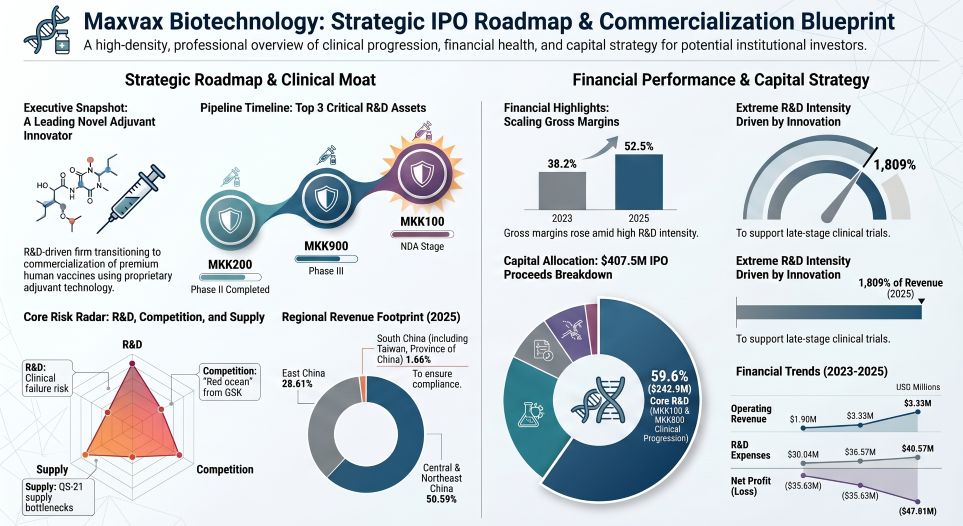

Operating under Mode A logic (Single Entity), a Forensic Analysis of Maxvax’s balance sheet reveals a structural transition. Currently, the company operates at a significant operating loss, strategically absorbed by top-tier institutional equity backing (SCGC, Hillhouse, IDG Capital). The targeted $407.52 million (CNY 2,929.06 million) IPO proceeds are rigorously earmarked for clinical acceleration and scalable manufacturing.

Figure Maxvax Biotechnology: Strategic lPO Roadmap & Commercialization Blueprint

* Top-Line & Margin Economics: Operating revenue—derived exclusively from veterinary adjuvants and culture media—recorded $1.90 million (2023), $3.33 million (2024), and $3.11 million (2025). Gross profit margins exhibited sequential expansion from 38.19% (2023) to 52.54% (2025), reflecting fixed-cost absorption in early production lines.

* Top-Line & Margin Economics: Operating revenue—derived exclusively from veterinary adjuvants and culture media—recorded $1.90 million (2023), $3.33 million (2024), and $3.11 million (2025). Gross profit margins exhibited sequential expansion from 38.19% (2023) to 52.54% (2025), reflecting fixed-cost absorption in early production lines.

* Operating Leverage & R&D Burn: Net losses expanded as late-stage trials accelerated: -$35.63 million (2023), -$47.61 million (2024), to -$69.89 million (2025). The R&D-to-revenue ratio hit an astronomical 1,809.13% in 2025 ($56.25 million).

* Segmental & Geographic Matrix (2025): Core revenue ($3.01 million) remains 100% domestic. Adjuvants control 86.26%, while culture media accounts for 10.19%. Geographically, East China dominates at 28.61%, followed by Central China (27.87%) and Northeast China (22.72%). Minor fractional exposure exists in Northwest & South China (including Taiwan, Province of China contextually) at 2.29% and 1.66% respectively.

* Capital Liquidity: As of 2025, cash reserves sit at $136.64 million, boosting the Current Ratio to 4.61x. A $27.83 million convertible bond from SCGC was completely converted to equity in September 2025, clearing off-balance-sheet hidden debt.

* Pipeline Technology Targets: TheMKK100 (Recombinant Shingles) utilizes the proprietaryMA105 novel adjuvant, competing directly againstGSK plc. TheMKK900 (RSV for the Elderly) couples theMA103 adjuvant with theDS-Cav1 antigen (licensed from the US NIH), currently in Phase III.

Maxvax Biotechnology Supply Chain Audit & Geo-Economic Moat

The physicality of Maxvax’s operations highlights a heavily centralized R&D infrastructure counterbalanced by a massive coastal manufacturing scaling strategy.

* Production & R&D Hubs: Pre-clinical and early-stage trials are isolated within the Chengdu Tianfu International Bio-Town via subsidiaries Chengdu Huarenkang and Chengdu Yisikang. The commercial pivot relies on the Shanghai Lingang Special Area, where a 12,000-sqm Phase I transition platform obtained its Vaccine Production License in September 2025.

* 2026 CAPEX Execution: The IPO allocates $89.89 million specifically for a 60,000-sqm scale-up industrial park in Shanghai, set for sequential activation starting in 2026. This facility utilizes advanced CHO cell expression systems where a single 500L bioreactor batch yields 6 to 8 million doses, ensuring robust economies of scale.

* Raw Material Geopolitics: Premium vaccine dependency onQS-21 (a plant-extracted natural saponin) represents the primary supply chain bottleneck. While Maxvax utilizes Tier-1 suppliers like Desert King International, the complex botanical extraction exposes the firm to geopolitical trade friction. To build a localized moat, Maxvax synthesizes other core lipids (DOTAP, DOPC, Poly IC, MPL) entirely in-house and is actively advancing semi-synthetic pathways for QS-21 to insulate against external shock.

HDIN Institutional Perspective: The R&D Expensing Lever

While standard retail analysis may fixate on Maxvax's $160.98 million accumulated unrecovered deficit and the impending regulatory risk of a strict $13.91 million revenue survival threshold by year 4 post-IPO, the Street is mispricing the company's financial governance. Maxvax applies an ultra-conservative 100% expensing policy to its R&D expenditures (0% capitalization).

By aggressively flushing $126.86 million in R&D costs through the income statement over the past three years—despite possessing an NDA-stage asset (MKK100) and a Phase III asset (MKK900)—the balance sheet is structurally protected from intangible asset bloat. Once the Lingang facility initiates its commercial shipments, the absence of heavy capitalized R&D amortization will cause post-commercialization ROIC and gross margins to artificially spike. Furthermore, securing expiration horizons extending to 2039-2045 for core formulation patents guarantees commercial exclusivity, providing the precise unit economics needed to undercut multinational incumbents while defending premium margin spreads.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

Forensic Financials & Capital Allocation of Maxvax Biotechnology

Operating under Mode A logic (Single Entity), a Forensic Analysis of Maxvax’s balance sheet reveals a structural transition. Currently, the company operates at a significant operating loss, strategically absorbed by top-tier institutional equity backing (SCGC, Hillhouse, IDG Capital). The targeted $407.52 million (CNY 2,929.06 million) IPO proceeds are rigorously earmarked for clinical acceleration and scalable manufacturing.

Figure Maxvax Biotechnology: Strategic lPO Roadmap & Commercialization Blueprint

* Top-Line & Margin Economics: Operating revenue—derived exclusively from veterinary adjuvants and culture media—recorded $1.90 million (2023), $3.33 million (2024), and $3.11 million (2025). Gross profit margins exhibited sequential expansion from 38.19% (2023) to 52.54% (2025), reflecting fixed-cost absorption in early production lines.* Operating Leverage & R&D Burn: Net losses expanded as late-stage trials accelerated: -$35.63 million (2023), -$47.61 million (2024), to -$69.89 million (2025). The R&D-to-revenue ratio hit an astronomical 1,809.13% in 2025 ($56.25 million).

* Segmental & Geographic Matrix (2025): Core revenue ($3.01 million) remains 100% domestic. Adjuvants control 86.26%, while culture media accounts for 10.19%. Geographically, East China dominates at 28.61%, followed by Central China (27.87%) and Northeast China (22.72%). Minor fractional exposure exists in Northwest & South China (including Taiwan, Province of China contextually) at 2.29% and 1.66% respectively.

* Capital Liquidity: As of 2025, cash reserves sit at $136.64 million, boosting the Current Ratio to 4.61x. A $27.83 million convertible bond from SCGC was completely converted to equity in September 2025, clearing off-balance-sheet hidden debt.

* Pipeline Technology Targets: TheMKK100 (Recombinant Shingles) utilizes the proprietaryMA105 novel adjuvant, competing directly againstGSK plc. TheMKK900 (RSV for the Elderly) couples theMA103 adjuvant with theDS-Cav1 antigen (licensed from the US NIH), currently in Phase III.

Maxvax Biotechnology Supply Chain Audit & Geo-Economic Moat

The physicality of Maxvax’s operations highlights a heavily centralized R&D infrastructure counterbalanced by a massive coastal manufacturing scaling strategy.

* Production & R&D Hubs: Pre-clinical and early-stage trials are isolated within the Chengdu Tianfu International Bio-Town via subsidiaries Chengdu Huarenkang and Chengdu Yisikang. The commercial pivot relies on the Shanghai Lingang Special Area, where a 12,000-sqm Phase I transition platform obtained its Vaccine Production License in September 2025.

* 2026 CAPEX Execution: The IPO allocates $89.89 million specifically for a 60,000-sqm scale-up industrial park in Shanghai, set for sequential activation starting in 2026. This facility utilizes advanced CHO cell expression systems where a single 500L bioreactor batch yields 6 to 8 million doses, ensuring robust economies of scale.

* Raw Material Geopolitics: Premium vaccine dependency onQS-21 (a plant-extracted natural saponin) represents the primary supply chain bottleneck. While Maxvax utilizes Tier-1 suppliers like Desert King International, the complex botanical extraction exposes the firm to geopolitical trade friction. To build a localized moat, Maxvax synthesizes other core lipids (DOTAP, DOPC, Poly IC, MPL) entirely in-house and is actively advancing semi-synthetic pathways for QS-21 to insulate against external shock.

HDIN Institutional Perspective: The R&D Expensing Lever

While standard retail analysis may fixate on Maxvax's $160.98 million accumulated unrecovered deficit and the impending regulatory risk of a strict $13.91 million revenue survival threshold by year 4 post-IPO, the Street is mispricing the company's financial governance. Maxvax applies an ultra-conservative 100% expensing policy to its R&D expenditures (0% capitalization).

By aggressively flushing $126.86 million in R&D costs through the income statement over the past three years—despite possessing an NDA-stage asset (MKK100) and a Phase III asset (MKK900)—the balance sheet is structurally protected from intangible asset bloat. Once the Lingang facility initiates its commercial shipments, the absence of heavy capitalized R&D amortization will cause post-commercialization ROIC and gross margins to artificially spike. Furthermore, securing expiration horizons extending to 2039-2045 for core formulation patents guarantees commercial exclusivity, providing the precise unit economics needed to undercut multinational incumbents while defending premium margin spreads.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*