LiqTech International: $20.0M Cap Table Restructuring Near Ballerup Core as 16% Debt Penalty Signals Severe Liquidity Pivot

Date : 2026-06-02

Reading : 154

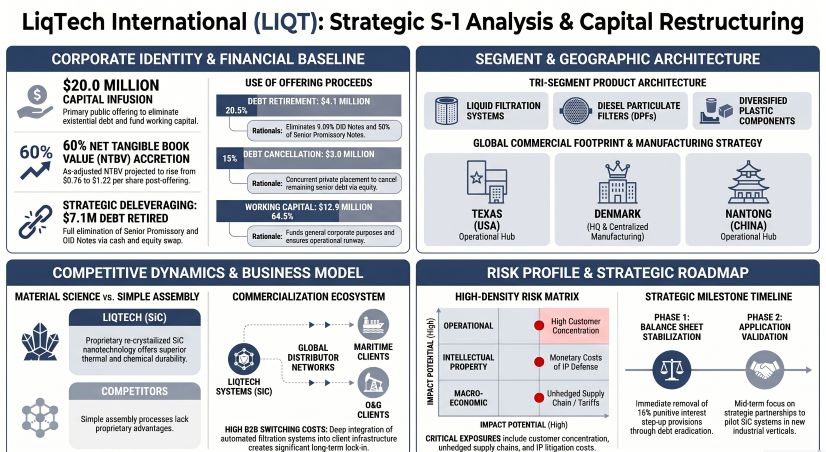

LiqTech’s aggressive $20.0 million equity raise and concurrent debt-for-equity swap is a survival-driven pivot to neutralize punitive 16% interest step-up provisions. By eradicating $7.1 million in related-party debt, the Danish material-science manufacturer secures vital operational runway to scale its proprietary silicon carbide (SiC) filtration systems. For institutional LPs, the immediate $0.58 per share dilution and massive derivative overhang reflect a steep cost of capital, but fundamentally de-risks the near-term balance sheet amid escalating global maritime emissions mandates.

Figure LiqTech International (LlQT): Strategic S-l Analysis & Capital Restructuring

LiqTech International Forensic Capitalization & Pro-Forma Deleveraging Audit

LiqTech International Forensic Capitalization & Pro-Forma Deleveraging Audit

A forensic analysis of NASDAQ: LIQT's S-1 reveals a highly dilutive financing structure engineered to circumvent near-term default risk. The financial architecture relies strictly on balance sheet restructuring rather than CapEx expansion. Because the company operates as a "smaller reporting company," standard operating leverage and exact unit economics are structurally omitted via incorporation by reference to the 2025 Form 10-K, leaving investors to price the equity solely on the pro-forma capitalization shock.

The $18.0 million in estimated net proceeds will be explicitly allocated to debt eradication ($4.1 million) and working capital ($13.9 million). The table below indexes the structural alteration of the cap table:

Physical Footprint & Silicon Carbide Supply Chain Vulnerabilities

LiqTech’s geo-economic moat relies on highly centralized production nodes supporting a decentralized global sales network. The physical nexus of the business is concentrated exclusively in Denmark. The primary manufacturing and executive hub is located at Industriparken 22C in Ballerup (Copenhagen area), supported by a secondary production facility at Benshoej Industrivej 24 in Hobro. All final filtration systems and Diesel Particulate Filters (DPFs) are shipped directly from these Danish facilities.

To maintain proximity to heavy industrial clients in the oil & gas and marine sectors, LiqTech operates international nodes in Fort Worth, Texas, and Nantong, China. However, a forensic audit of the supply chain disclosures highlights critical, unhedged vulnerabilities. The company lacks fixed-price forward contracts for its primary raw material—silicon carbide. Management acknowledges a direct operational threat stemming from an "inability to secure and source supplies of raw materials and key components in due time and at competitive prices." This exposes the centralized Danish production core to spot-market volatility, global trade tariffs, and localized energy shocks, effectively bottlenecking the scalability of the Fort Worth and Nantong commercial pipelines.

HDIN Institutional Perspective: The Control Block is the True Moat, Not Just the IP

While the S-1 frames LiqTech's competitive advantage around patented re-crystallized SiC nanotechnology and its November 2022 NESR Exclusivity Agreement, the capitalization mechanics suggest a distressed, related-party bailout that the Street hasn't fully priced in.

The issuance of $1.1 million in 9.09% OID Notes to major insiders (Bleichroeder and Lytton) on May 22, 2026—just days prior to the implied S-1 filing—indicates that traditional commercial credit markets view the company's severe customer concentration as untenable. The threat of a 16% penalty interest rate forced management's hand into accepting a 128% dilution of the existing float. Consequently, the firm's immediate operational survival is entirely dependent on its 30.1% control block acting as the lender of last resort. External analysts must track whether the $13.9 million injected into working capital successfully converts targeted oil & gas and marine pilot programs into tangible purchase orders by Q4 2026; if not, the massive derivative overhang (fully diluted cap of ~35.8 million shares) will severely suppress any equity upside.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure LiqTech International (LlQT): Strategic S-l Analysis & Capital Restructuring

LiqTech International Forensic Capitalization & Pro-Forma Deleveraging AuditA forensic analysis of NASDAQ: LIQT's S-1 reveals a highly dilutive financing structure engineered to circumvent near-term default risk. The financial architecture relies strictly on balance sheet restructuring rather than CapEx expansion. Because the company operates as a "smaller reporting company," standard operating leverage and exact unit economics are structurally omitted via incorporation by reference to the 2025 Form 10-K, leaving investors to price the equity solely on the pro-forma capitalization shock.

The $18.0 million in estimated net proceeds will be explicitly allocated to debt eradication ($4.1 million) and working capital ($13.9 million). The table below indexes the structural alteration of the cap table:

Table Post-Offering Capitalization and Dilution Analysis (March–May 2026)

| Capitalization Metric (As of May/March 2026) | Stated Value / Share Impact | Strategic Context & Dilution Mechanics |

|---|---|---|

| Historical Net Tangible Book Value | $7.6 Million ($0.76/share) | Pre-offering baseline asset valuation |

| As-Adjusted NTBV | $25.6 Million ($1.22/share) | Post-offering projection; creates an immediate $0.58 per share dilution to new investors purchasing at the $1.80 target price |

| Common Shares Outstanding (Base) | 22,725,618 Shares | Expands from 9.94 million shares pre-offering, representing approximately 128% immediate dilution of the common float |

| Derivative Overhang (Pre-Funded & Standard Warrants) | 11,391,225 Warrants | Includes 5.29 million pre-funded warrants at a $0.006 strike price, effectively acting as common stock equivalents and increasing future dilution risk |

| Related-Party Debt (To Be Retired) | $7.1 Million | Retires $6.0 million senior promissory notes (via $3.0 million cash and $3.0 million equity conversion) and $1.1 million of 9.09% OID notes |

| Insider Control Block (Post-Offering) | 30.1% Voting Power | Affiliates of Bleichroeder L.P., L.W. Lytton, and Ben Andrews establish effective control over key corporate matters |

LiqTech’s geo-economic moat relies on highly centralized production nodes supporting a decentralized global sales network. The physical nexus of the business is concentrated exclusively in Denmark. The primary manufacturing and executive hub is located at Industriparken 22C in Ballerup (Copenhagen area), supported by a secondary production facility at Benshoej Industrivej 24 in Hobro. All final filtration systems and Diesel Particulate Filters (DPFs) are shipped directly from these Danish facilities.

To maintain proximity to heavy industrial clients in the oil & gas and marine sectors, LiqTech operates international nodes in Fort Worth, Texas, and Nantong, China. However, a forensic audit of the supply chain disclosures highlights critical, unhedged vulnerabilities. The company lacks fixed-price forward contracts for its primary raw material—silicon carbide. Management acknowledges a direct operational threat stemming from an "inability to secure and source supplies of raw materials and key components in due time and at competitive prices." This exposes the centralized Danish production core to spot-market volatility, global trade tariffs, and localized energy shocks, effectively bottlenecking the scalability of the Fort Worth and Nantong commercial pipelines.

HDIN Institutional Perspective: The Control Block is the True Moat, Not Just the IP

While the S-1 frames LiqTech's competitive advantage around patented re-crystallized SiC nanotechnology and its November 2022 NESR Exclusivity Agreement, the capitalization mechanics suggest a distressed, related-party bailout that the Street hasn't fully priced in.

The issuance of $1.1 million in 9.09% OID Notes to major insiders (Bleichroeder and Lytton) on May 22, 2026—just days prior to the implied S-1 filing—indicates that traditional commercial credit markets view the company's severe customer concentration as untenable. The threat of a 16% penalty interest rate forced management's hand into accepting a 128% dilution of the existing float. Consequently, the firm's immediate operational survival is entirely dependent on its 30.1% control block acting as the lender of last resort. External analysts must track whether the $13.9 million injected into working capital successfully converts targeted oil & gas and marine pilot programs into tangible purchase orders by Q4 2026; if not, the massive derivative overhang (fully diluted cap of ~35.8 million shares) will severely suppress any equity upside.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."