Modine Manufacturing Company: Pivot to AI Thermal Infrastructure Near North American Hubs as Massive Capital Deployment Signals Structural Value Creation

Date : 2026-06-02

Reading : 82

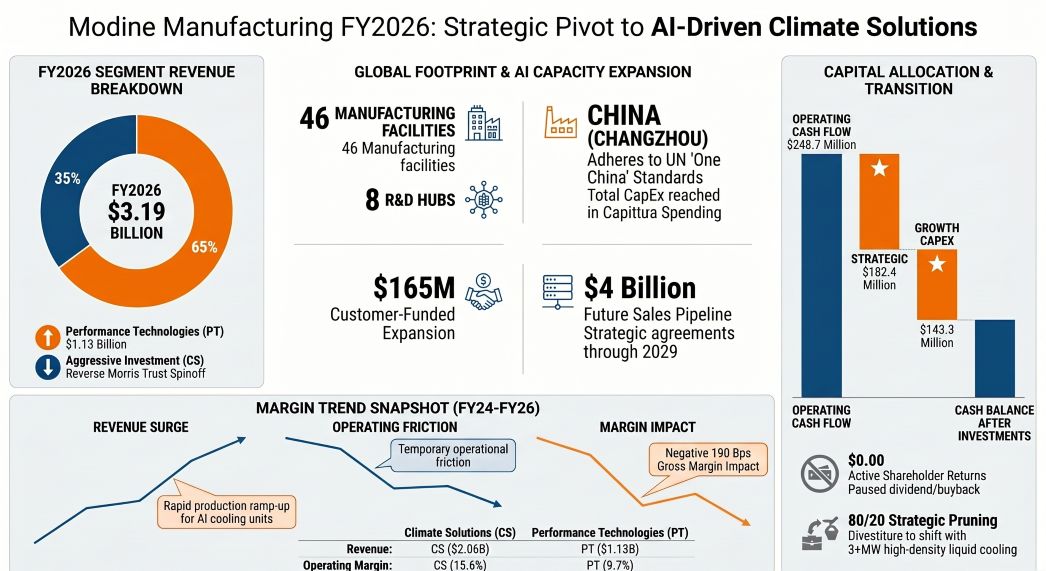

Modine’s FY2026 filings reveal a ruthless 80/20 capital reallocation. By structurally exiting the low-margin commercial vehicle thermal space via a Reverse Morris Trust spin-off to Gentherm, Modine is aggressively rotating its balance sheet toward high-density AI data center cooling. The statutory 1000 bps ROE compression is an accounting artifact driven by a $116.1M U.S. pension termination charge. For institutional LPs, the critical variable is the $165M zero-interest customer deposit underwriting a $4B capacity pipeline through 2029, effectively de-risking its $143.3M CapEx surge.

Figure Modine Manufacturing FY2026: Strategic Pivot to Al-Driven Climate Solutions

Forensic Financials & Segmental Inventory

Forensic Financials & Segmental Inventory

A Forensic Analysis of the FY2026 consolidated statements reveals a severe dichotomy between statutory optical deterioration and actual core operating leverage expansion. NYSE: MOD is sacrificing short-term asset turnover (falling from 1.35x to 1.19x) to finance a generational infrastructure moat.

Consolidated Top-Line & Segmental Margins (FY2026)

* Total Net Sales: $3.18 billion (+23.1% YoY).

* Consolidated Operating Income: $342.4 million (Core Operating Income expanded 20.8% excluding the pension settlement artifact, net of $88.4 million in corporate eliminations).

* Climate Solutions (CS): Generated $2.06 billion (65% of consolidated sales). This segment operates as the core profit engine, yielding an operating income of $321.1 million at a robust 15.6% margin.

* Performance Technologies (PT): Generated $1.13 billion (35% of sales) with a structurally inferior operating margin of 9.7% ($109.7 million operating income).

Product Group Unit Economics & Demand Drivers

* Data Centers: $1.11 billion (35%). The hyper-growth engine driven by the proprietary TurboChill™ 3+MW chiller and immersion cooling assimilation.

* On-Highway Applications: $716.4 million (23%). Stagnating traditional powertrain cooling footprint.

* Heat Transfer Solutions: $584.1 million (18%). Boosted by $182.4 million M&A deployment acquiring L.B. White, Climate by Design, and AbsolutAire.

* Heavy-Duty Equipment: $409.3 million (13%).

* HVAC Technologies: $359.2 million (11%).

Margin Compression Audit: Gross margins contracted 190 bps to 23.0%, while Net Profit Margins fell 340 bps to 3.8%. This friction is traced directly to $28.0 million in raw material (aluminum, copper, steel) and tariff cost inflation, compounded by temporary operating inefficiencies during the aggressive capacity ramp-up across North American operations.

Supply Chain Audit & Geo-Economic Moat

Modine's geographic revenue remains overwhelmingly Western-centric, with $1.68 billion flowing from the United States, $332.6 million from Canada, and $838.2 million spread across Europe (heavily anchored by Italy at $226.8 million and the UK at $192.7 million).

The Physicality of the R&D and Manufacturing Base

The Company operates a decentralized network of 46 physical manufacturing facilities (Americas: 24, Europe: 14, Asia: 8). To transition from a parts supplier to a mission-critical thermal architect, Modine leverages specific global R&D and technical support hubs. Key nodes include the World Headquarters in Racine, Wisconsin, supported by specialized R&D sites in Grenada, Mississippi; Allen, Texas; Leeds, United Kingdom; Pocenia, Italy; Guadalajara, Spain; Söderköping, Sweden; Mezökövesd, Hungary; Sao Paulo, Brazil; Changzhou, China; and the Chennai Tier-1 Facility in India.

Forensic Risk & Backlog Assessment

The most critical threat embedded in the 10-K is a localized supply chain rupture. Critical component demand for data center liquid cooling is officially outpacing Tier-1 supplier capacity. This shortage, which materialized in Q4 FY2026, is explicitly flagged by management as negatively impacting production schedules for Q1 FY2027.

Furthermore, the balance sheet carries a $12.7 million environmental remediation provision covering legacy soil and groundwater contamination, alongside unquantified exposure to the regulatory phase-out of fluorinated gases (PFAS), forcing capital rotation toward Low-GWP natural gas and CO2 cooling solutions. IT and Cloud Infrastructure operational commitments are heavily backloaded, totaling $30.0 million from FY2027 through FY2030.

HDIN Institutional Perspective: Confirming the Strategic Pivot, Challenging the Supply Chain Resilience.

While the Street has priced in the 23.1% revenue growth, HDIN analysts assess that the market severely misunderstands Modine’s capital efficiency. The Company successfully engineered a zero-cash return to shareholders policy (0% buybacks, $0 dividends) without institutional revolt. Why? Because the $105.4 million Free Cash Flow print is artificially suppressed by a brilliant capital maneuver: Modine secured a $165.0 million up-front customer deposit to lock in a $4.0 billion sales pipeline through 2029. This is zero-interest, non-dilutive customer financing underwriting the $143.3 million CapEx surge.

However, HDIN challenges the elasticity of the Company’s procurement network. The 190 bps gross margin contraction proves that Modine’s LME-indexed forward contracts are failing to absorb localized "metals premiums" and fabrication cost spikes. The strategic divestiture of the Performance Technologies unit via the Gentherm Reverse Morris Trust is a masterful balance sheet cleansing, but if Modine fails to qualify new component vendors for its data center chillers by Q2 FY2027, the resulting unfulfilled order backlog will materially compress its AI infrastructure premium.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Modine Manufacturing FY2026: Strategic Pivot to Al-Driven Climate Solutions

Forensic Financials & Segmental InventoryA Forensic Analysis of the FY2026 consolidated statements reveals a severe dichotomy between statutory optical deterioration and actual core operating leverage expansion. NYSE: MOD is sacrificing short-term asset turnover (falling from 1.35x to 1.19x) to finance a generational infrastructure moat.

Consolidated Top-Line & Segmental Margins (FY2026)

* Total Net Sales: $3.18 billion (+23.1% YoY).

* Consolidated Operating Income: $342.4 million (Core Operating Income expanded 20.8% excluding the pension settlement artifact, net of $88.4 million in corporate eliminations).

* Climate Solutions (CS): Generated $2.06 billion (65% of consolidated sales). This segment operates as the core profit engine, yielding an operating income of $321.1 million at a robust 15.6% margin.

* Performance Technologies (PT): Generated $1.13 billion (35% of sales) with a structurally inferior operating margin of 9.7% ($109.7 million operating income).

Product Group Unit Economics & Demand Drivers

* Data Centers: $1.11 billion (35%). The hyper-growth engine driven by the proprietary TurboChill™ 3+MW chiller and immersion cooling assimilation.

* On-Highway Applications: $716.4 million (23%). Stagnating traditional powertrain cooling footprint.

* Heat Transfer Solutions: $584.1 million (18%). Boosted by $182.4 million M&A deployment acquiring L.B. White, Climate by Design, and AbsolutAire.

* Heavy-Duty Equipment: $409.3 million (13%).

* HVAC Technologies: $359.2 million (11%).

Margin Compression Audit: Gross margins contracted 190 bps to 23.0%, while Net Profit Margins fell 340 bps to 3.8%. This friction is traced directly to $28.0 million in raw material (aluminum, copper, steel) and tariff cost inflation, compounded by temporary operating inefficiencies during the aggressive capacity ramp-up across North American operations.

Supply Chain Audit & Geo-Economic Moat

Modine's geographic revenue remains overwhelmingly Western-centric, with $1.68 billion flowing from the United States, $332.6 million from Canada, and $838.2 million spread across Europe (heavily anchored by Italy at $226.8 million and the UK at $192.7 million).

The Physicality of the R&D and Manufacturing Base

The Company operates a decentralized network of 46 physical manufacturing facilities (Americas: 24, Europe: 14, Asia: 8). To transition from a parts supplier to a mission-critical thermal architect, Modine leverages specific global R&D and technical support hubs. Key nodes include the World Headquarters in Racine, Wisconsin, supported by specialized R&D sites in Grenada, Mississippi; Allen, Texas; Leeds, United Kingdom; Pocenia, Italy; Guadalajara, Spain; Söderköping, Sweden; Mezökövesd, Hungary; Sao Paulo, Brazil; Changzhou, China; and the Chennai Tier-1 Facility in India.

Forensic Risk & Backlog Assessment

The most critical threat embedded in the 10-K is a localized supply chain rupture. Critical component demand for data center liquid cooling is officially outpacing Tier-1 supplier capacity. This shortage, which materialized in Q4 FY2026, is explicitly flagged by management as negatively impacting production schedules for Q1 FY2027.

Furthermore, the balance sheet carries a $12.7 million environmental remediation provision covering legacy soil and groundwater contamination, alongside unquantified exposure to the regulatory phase-out of fluorinated gases (PFAS), forcing capital rotation toward Low-GWP natural gas and CO2 cooling solutions. IT and Cloud Infrastructure operational commitments are heavily backloaded, totaling $30.0 million from FY2027 through FY2030.

HDIN Institutional Perspective: Confirming the Strategic Pivot, Challenging the Supply Chain Resilience.

While the Street has priced in the 23.1% revenue growth, HDIN analysts assess that the market severely misunderstands Modine’s capital efficiency. The Company successfully engineered a zero-cash return to shareholders policy (0% buybacks, $0 dividends) without institutional revolt. Why? Because the $105.4 million Free Cash Flow print is artificially suppressed by a brilliant capital maneuver: Modine secured a $165.0 million up-front customer deposit to lock in a $4.0 billion sales pipeline through 2029. This is zero-interest, non-dilutive customer financing underwriting the $143.3 million CapEx surge.

However, HDIN challenges the elasticity of the Company’s procurement network. The 190 bps gross margin contraction proves that Modine’s LME-indexed forward contracts are failing to absorb localized "metals premiums" and fabrication cost spikes. The strategic divestiture of the Performance Technologies unit via the Gentherm Reverse Morris Trust is a masterful balance sheet cleansing, but if Modine fails to qualify new component vendors for its data center chillers by Q2 FY2027, the resulting unfulfilled order backlog will materially compress its AI infrastructure premium.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."