AEVEX: Manufacturing Pivot Near Tampa Hub as 306.9% Revenue Surge Signals Monopsony Scale Amid Geopolitical Friction

Date : 2026-06-03

Reading : 197

AEVEX is executing a hyperscaled transition from boutique engineering to mass defense manufacturing, evidenced by a 306.9% revenue explosion in Q1 2026. However, institutional LPs must parse a structural dichotomy: unparalleled sole-source operational dominance offset by severe PE-sponsored capital extraction. While the Tampa facility readies the $645.7 million EUCOM program, the corporate Up-C architecture mandates that 100% of the $212 million primary share issuance flows directly to Madison Dearborn Partners (MDP), bypassing the balance sheet and inflating a $561.4 million Tax Receivable Agreement (TRA) liability.

Figure AEVEX Corp Strategic Analysis: Scaling Autonomous Warfare & The Capital Re-Architecture

Forensic Analysis of AEVEX Operational Leverage and Up-C Capital Extraction

Forensic Analysis of AEVEX Operational Leverage and Up-C Capital Extraction

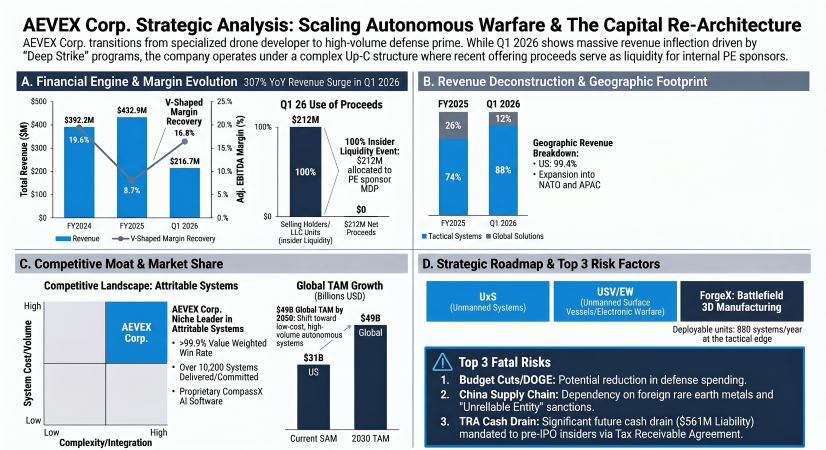

AEVEX’s financial trajectory illustrates the extreme working capital intensity required to service United States Department of War (DoW) mega-contracts. The transition from the legacy Phoenix Ghost program (4,400+ units, $581.0 million) to the active EUCOM AOR Deep Strike contract (4,800+ planned units, $645.7 million) initially compressed FY2025 margins before yielding aggressive operating leverage in early 2026.

Segmental & Baseline Financial Inventory (FY2024 – Q1 2026):

* Top-Line Velocity: Total revenue expanded 10.4% year-over-year in FY2025 to $432.9 million, before surging 306.9% YoY in Q1 2026 to $216.7 million.

* Tactical Systems Margin Expansion: The core hardware segment generated $190.8 million in Q1 2026 (88.0% of total revenue), achieving a 20.2% Segment Adjusted EBITDA margin—proving the fixed-cost absorption capabilities of at-scale production.

* Working Capital Strain (Unbilled AR): FY2025 Operating Cash Flow collapsed to $(97.6) million, driven by cost-to-cost accounting mechanisms. As of March 31, 2026, unbilled accounts receivable stood at a staggering $63.78 million (out of $85.82 million total AR), highlighting the cash drag of pre-milestone hardware procurement.

* Corporate Debt Restructuring: In April 2026, management replaced $258.5 million in punitive prior debt (Term SOFR + 6.00%, effectively yielding ~9.92% to 10.57%) with a $375.0 million Bank of America syndicated facility, slashing financing costs to SOFR + 2.25% to 3.00%.

Internal Capital Allocation & Shareholder Dilution:

AEVEX’s S-1 issuance of 8.0 million Class A shares functions strictly as a liquidity event for insiders. The 5.72 million shares issued by the company will generate approximately $212.0 million (assuming $38.47/share). Exactly 0% of this capital is allocated to R&D or CapEx. Instead, 100% is utilized to purchase Series B units from the MDP-controlled Holdings LLC, triggering a TRA that contractually mandates the public entity to pay pre-IPO insiders 85% of realized tax savings—a non-current liability capping out at $561.4 million.

Tampa-to-Edge Logistics and the Rare Earth Geopolitical Chokepoint

AEVEX operates an asset-light, highly clustered manufacturing footprint intentionally decoupled from traditional supply chain timelines, yet profoundly exposed to foreign upstream minerals.

* The Physical Footprint: Operations are anchored by a 94,000 sq. ft. primary R&D and manufacturing hub in Tampa, FL (supported by a 120-acre FAA-approved test range). Secondary integration is executed in Murrieta, CA (80,200 sq. ft.) and the Navigation and Autonomy Center (NAC) in Dayton, OH (6,410 sq. ft.). Fixed capacity currently sits at >12,000 systems annually.

* ForgeX Mobile Production Units (MPUs): Disrupting traditional logistics, AEVEX deploys containerized 3D-printing micro-factories to the tactical edge. Operated by two technicians, a 16-printer ForgeX node can additively manufacture 880 Unmanned Systems (UxS) annually, compressing order-to-delivery cycles to just nine days.

* The China-MOFCOM Geopolitical Vulnerability: AEVEX’s autonomous hardware relies extensively on Neodymium, Praseodymium, and Lanthanum. In January 2025, China's Ministry of Commerce (MOFCOM) placed AEVEX on its "Unreliable Entity List," instituting an import/export embargo. With Executive Chairman Brian Raduenz also permanently sanctioned by Russia, AEVEX faces critical raw material bottlenecks that threaten to derail its >30.0% targeted Internal Rate of Return (IRR) on new production.

HDIN Institutional Perspective

While AEVEX projects a software-like >99.9% retention rate anchored by its proprietary CompassX autonomy suite, the underlying economics confirm a hyper-traditional, working-capital-intensive hardware burn. The optical $356.6 million funded backlog masks severe monopsony risk (the U.S. Government accounted for 88.0% of Q1 2026 revenue), exposing the company to systemic shocks if the newly established Department of Government Efficiency (DOGE) initiates defense procurement audits. More critically, the S-1 reveals an ultimate liquidity trap: public shareholders are funding a $212.0 million direct exit for the PE sponsor while inheriting a half-billion-dollar TRA obligation. For institutional allocators, AEVEX offers unmatched visibility into NATO's $49.0 billion 2030 TAM, but the Up-C governance structure severely limits the free cash flow available for future strategic M&A.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure AEVEX Corp Strategic Analysis: Scaling Autonomous Warfare & The Capital Re-Architecture

Forensic Analysis of AEVEX Operational Leverage and Up-C Capital ExtractionAEVEX’s financial trajectory illustrates the extreme working capital intensity required to service United States Department of War (DoW) mega-contracts. The transition from the legacy Phoenix Ghost program (4,400+ units, $581.0 million) to the active EUCOM AOR Deep Strike contract (4,800+ planned units, $645.7 million) initially compressed FY2025 margins before yielding aggressive operating leverage in early 2026.

Segmental & Baseline Financial Inventory (FY2024 – Q1 2026):

* Top-Line Velocity: Total revenue expanded 10.4% year-over-year in FY2025 to $432.9 million, before surging 306.9% YoY in Q1 2026 to $216.7 million.

* Tactical Systems Margin Expansion: The core hardware segment generated $190.8 million in Q1 2026 (88.0% of total revenue), achieving a 20.2% Segment Adjusted EBITDA margin—proving the fixed-cost absorption capabilities of at-scale production.

* Working Capital Strain (Unbilled AR): FY2025 Operating Cash Flow collapsed to $(97.6) million, driven by cost-to-cost accounting mechanisms. As of March 31, 2026, unbilled accounts receivable stood at a staggering $63.78 million (out of $85.82 million total AR), highlighting the cash drag of pre-milestone hardware procurement.

* Corporate Debt Restructuring: In April 2026, management replaced $258.5 million in punitive prior debt (Term SOFR + 6.00%, effectively yielding ~9.92% to 10.57%) with a $375.0 million Bank of America syndicated facility, slashing financing costs to SOFR + 2.25% to 3.00%.

Internal Capital Allocation & Shareholder Dilution:

AEVEX’s S-1 issuance of 8.0 million Class A shares functions strictly as a liquidity event for insiders. The 5.72 million shares issued by the company will generate approximately $212.0 million (assuming $38.47/share). Exactly 0% of this capital is allocated to R&D or CapEx. Instead, 100% is utilized to purchase Series B units from the MDP-controlled Holdings LLC, triggering a TRA that contractually mandates the public entity to pay pre-IPO insiders 85% of realized tax savings—a non-current liability capping out at $561.4 million.

Tampa-to-Edge Logistics and the Rare Earth Geopolitical Chokepoint

AEVEX operates an asset-light, highly clustered manufacturing footprint intentionally decoupled from traditional supply chain timelines, yet profoundly exposed to foreign upstream minerals.

* The Physical Footprint: Operations are anchored by a 94,000 sq. ft. primary R&D and manufacturing hub in Tampa, FL (supported by a 120-acre FAA-approved test range). Secondary integration is executed in Murrieta, CA (80,200 sq. ft.) and the Navigation and Autonomy Center (NAC) in Dayton, OH (6,410 sq. ft.). Fixed capacity currently sits at >12,000 systems annually.

* ForgeX Mobile Production Units (MPUs): Disrupting traditional logistics, AEVEX deploys containerized 3D-printing micro-factories to the tactical edge. Operated by two technicians, a 16-printer ForgeX node can additively manufacture 880 Unmanned Systems (UxS) annually, compressing order-to-delivery cycles to just nine days.

* The China-MOFCOM Geopolitical Vulnerability: AEVEX’s autonomous hardware relies extensively on Neodymium, Praseodymium, and Lanthanum. In January 2025, China's Ministry of Commerce (MOFCOM) placed AEVEX on its "Unreliable Entity List," instituting an import/export embargo. With Executive Chairman Brian Raduenz also permanently sanctioned by Russia, AEVEX faces critical raw material bottlenecks that threaten to derail its >30.0% targeted Internal Rate of Return (IRR) on new production.

HDIN Institutional Perspective

While AEVEX projects a software-like >99.9% retention rate anchored by its proprietary CompassX autonomy suite, the underlying economics confirm a hyper-traditional, working-capital-intensive hardware burn. The optical $356.6 million funded backlog masks severe monopsony risk (the U.S. Government accounted for 88.0% of Q1 2026 revenue), exposing the company to systemic shocks if the newly established Department of Government Efficiency (DOGE) initiates defense procurement audits. More critically, the S-1 reveals an ultimate liquidity trap: public shareholders are funding a $212.0 million direct exit for the PE sponsor while inheriting a half-billion-dollar TRA obligation. For institutional allocators, AEVEX offers unmatched visibility into NATO's $49.0 billion 2030 TAM, but the Up-C governance structure severely limits the free cash flow available for future strategic M&A.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."