HTC Corporation: $250M Google Divestiture Near Taoyuan City as -119% Operating Margin Signals Aggressive Spatial Computing Pivot

Date : 2026-06-04

Reading : 293

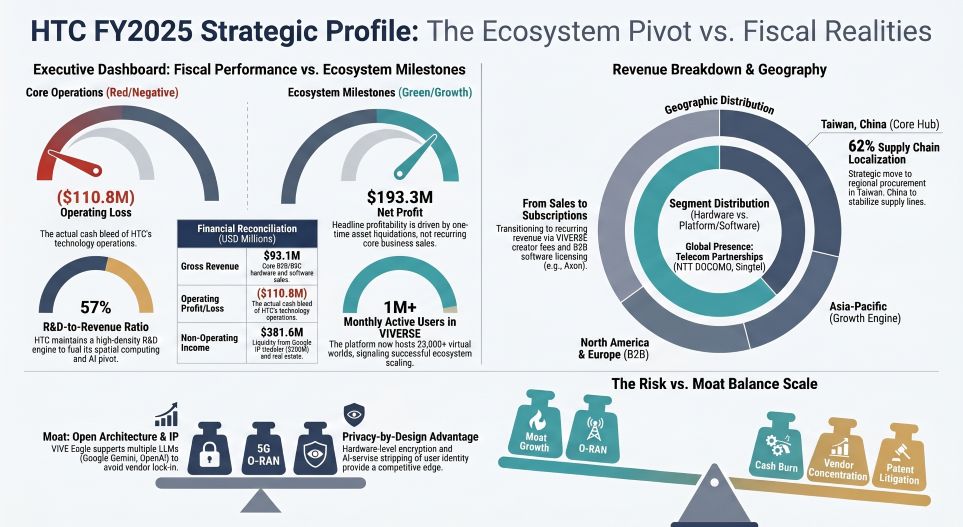

HTC Corporation's FY2025 net profit of $193.33 million masks a severe operational cash bleed, artificially inflated by a $250 million IP and personnel transfer to Google and the liquidation of its Taoyuan manufacturing footprint. With core operating margins contracting to -119.01% and an abysmal 0.0685x asset turnover, the firm is cannibalizing legacy physical assets to fund a $53.01 million R&D engine. For institutional LPs, HTC’s survival relies entirely on its 4.7-year cash runway and a high-stakes pivot toward B2B spatial computing software and O-RAN 5G ecosystems amid global macroeconomic stagnation.

Figure HTC FY2025 Strategic Profile: The Ecosystem Pivot vs Fiscal Realities

Forensic Financials & Segmental Inventory

Forensic Financials & Segmental Inventory

Our Forensic Analysis strips away the $381.64 million in extraordinary non-operating income to reveal the true unit economics of TPE: 2498. The transition from a transactional hardware manufacturer to a VIVERSE ecosystem provider has severely compressed near-term liquidity, offset only by aggressive austerity that saw global headcount slashed by 40.6% (to 1,155 employees by fiscal year-end, compressing further to 1,090 by March 31, 2026).

Unit Economics & Segmental Drivers:

* VIVERSE Creator Economy: Implemented a new revenue-sharing model (90% to creators / 10% to platform in Year 1; 80/20 subsequently). The platform achieved 1 million MAUs and 23,000 virtual worlds.

* AI Hardware Innovations: The newly launched 49g VIVE Eagle smart glasses integrate multiple Large Language Models (LLMs) (OpenAI GPT, Google Gemini) via an open architecture, paired with a 12MP camera and "VIVE AI Notes" for 12-language transcription.

* Executive Compensation: Board remuneration was halted ($0 to Chairwoman/CEO Cher Wang). A $5.39 million cash distribution was approved for employees, while VP/President compensation was restricted to 2.34% of net income.

Supply Chain Audit & Geo-Economic Moat

HTC’s physical infrastructure underwent a radical localization and liquidation cycle in FY2025, consolidating its geographic footprint to mitigate global trade barriers and Scope 3 carbon emissions.

* Geographic Liquidation & Localization: Management executed the strategic sale of Taoyuan City manufacturing facilities (Building H, TY4, Building P) in Taiwan, China. To insulate against geopolitical shocks, 62% of raw material procurement has been localized to regional Tier-1 suppliers.

* Supplier Concentration & Bottleneck Risks: Out of a $44.82 million procurement budget, 33% is consolidated into just two undisclosed vendors (Supplier A at 22% / $9.66M; Supplier B at 11% / $4.91M). Any capacity constraint here threatens hardware fulfillment.

* Qualcomm Dependency: HTC remains systemically bound to NASDAQ: QCOM via a CDMA patent license agreement. The contract contains a severe 30-day remediation covenant for material breaches, posing an existential supply chain threat to devices utilizing the Snapdragon XR2 platform.

* Global Enterprise Footprint: G REIGNS 5G private networks (O-RAN architecture deployed in 15 minutes) secured footholds in Germany and North America. VIVE Arts dominates European cultural heritage infrastructure, partnering with the Louvre and Opéra Garnier in France.

* Environmental & Legal Liabilities: HTC achieved a 76.6% recycling rate for the VIVE Eagle and a 91.26% industrial waste recycling rate across Taiwan, China operations. However, the balance sheet faces contingent liabilities in the U.S. District Court of Delaware following an October 2023 patent infringement guilty verdict brought by 3G Licensing S.A., currently under appeal with court security deposited. 38 supplier factories were audited under the RBA VAP, and 126 conformant smelters confirmed 100% conflict-mineral-free sourcing.

HDIN Institutional Perspective

While HTC’s 2025 Annual Report claims an "open-architecture" software moat, the sheer scale of the firm's non-operating maneuvers suggests a traditional hardware-intensive burn rate that the Street hasn't properly priced into its valuation. The headline 25.09% ROE is an accounting mirage funded by the cannibalization of legacy Taoyuan real estate and the $250M Google transaction. However, HTC’s 4.7-year cash runway is genuine. If management can leverage government subsidies (e.g., Taiwan Creative Content Agency funding for the 2026 VPOP ASIA and *Gloomy Eyes* LBE releases) and mature recurring B2B subscriptions (such as the North American Axon police training VR), HTC may successfully incubate its O-RAN 5G and VIVERSE IP before the liquidity buffer expires.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure HTC FY2025 Strategic Profile: The Ecosystem Pivot vs Fiscal Realities

Forensic Financials & Segmental InventoryOur Forensic Analysis strips away the $381.64 million in extraordinary non-operating income to reveal the true unit economics of TPE: 2498. The transition from a transactional hardware manufacturer to a VIVERSE ecosystem provider has severely compressed near-term liquidity, offset only by aggressive austerity that saw global headcount slashed by 40.6% (to 1,155 employees by fiscal year-end, compressing further to 1,090 by March 31, 2026).

Table FY2025 Financial Performance and Strategic Analysis

| FY2025 Financial Metric | Reported Value (USD) | YoY / Ratio | Strategic Implication |

|---|---|---|---|

| Gross Revenue | $93.07M (NT$2.90B) | -5.85% YoY | Stagnant hardware sales offset by emerging B2B SaaS solutions |

| Gross Margin | $33.40M | 35.89% | Shift toward software licensing (VIVE LBSS) supports gross baseline |

| Core Operating Loss | -$110.77M (NT$-3.45B) | -119.01% Margin | Core XR/Mobile operations remain deeply unprofitable |

| Non-Operating Income | $381.64M | N/A | Driven by $250M NASDAQ: GOOGL XR IP/staff transfer, $7.47M net interest, ~$128.38M Taoyuan real estate disposal |

| Reported Net Profit | $193.33M (NT$6.03B) | 207.73% Margin | Artificial ROE inflation (25.09%); core business is cash-negative |

| Capital Expenditures | $13.83M (NT$430.95M) | N/A | Constrained CAPEX environment as production is outsourced |

| Free Cash Flow (FCF) | -$150.93M (Estimated) | N/A | Operating Cash Flow (-$137.10M) minus CAPEX ($13.83M) |

| R&D Expenditure | $53.01M (NT$1.65B) | 57% of Revenue | Down from 86% YoY, but indicates heavy tech capitalization burden |

| Balance Sheet Solvency | Current Assets: $646.54M | D/E Ratio: 0.45 | Represents ~4.7-year cash runway to execute VIVERSE turnaround |

* VIVERSE Creator Economy: Implemented a new revenue-sharing model (90% to creators / 10% to platform in Year 1; 80/20 subsequently). The platform achieved 1 million MAUs and 23,000 virtual worlds.

* AI Hardware Innovations: The newly launched 49g VIVE Eagle smart glasses integrate multiple Large Language Models (LLMs) (OpenAI GPT, Google Gemini) via an open architecture, paired with a 12MP camera and "VIVE AI Notes" for 12-language transcription.

* Executive Compensation: Board remuneration was halted ($0 to Chairwoman/CEO Cher Wang). A $5.39 million cash distribution was approved for employees, while VP/President compensation was restricted to 2.34% of net income.

Supply Chain Audit & Geo-Economic Moat

HTC’s physical infrastructure underwent a radical localization and liquidation cycle in FY2025, consolidating its geographic footprint to mitigate global trade barriers and Scope 3 carbon emissions.

* Geographic Liquidation & Localization: Management executed the strategic sale of Taoyuan City manufacturing facilities (Building H, TY4, Building P) in Taiwan, China. To insulate against geopolitical shocks, 62% of raw material procurement has been localized to regional Tier-1 suppliers.

* Supplier Concentration & Bottleneck Risks: Out of a $44.82 million procurement budget, 33% is consolidated into just two undisclosed vendors (Supplier A at 22% / $9.66M; Supplier B at 11% / $4.91M). Any capacity constraint here threatens hardware fulfillment.

* Qualcomm Dependency: HTC remains systemically bound to NASDAQ: QCOM via a CDMA patent license agreement. The contract contains a severe 30-day remediation covenant for material breaches, posing an existential supply chain threat to devices utilizing the Snapdragon XR2 platform.

* Global Enterprise Footprint: G REIGNS 5G private networks (O-RAN architecture deployed in 15 minutes) secured footholds in Germany and North America. VIVE Arts dominates European cultural heritage infrastructure, partnering with the Louvre and Opéra Garnier in France.

* Environmental & Legal Liabilities: HTC achieved a 76.6% recycling rate for the VIVE Eagle and a 91.26% industrial waste recycling rate across Taiwan, China operations. However, the balance sheet faces contingent liabilities in the U.S. District Court of Delaware following an October 2023 patent infringement guilty verdict brought by 3G Licensing S.A., currently under appeal with court security deposited. 38 supplier factories were audited under the RBA VAP, and 126 conformant smelters confirmed 100% conflict-mineral-free sourcing.

HDIN Institutional Perspective

While HTC’s 2025 Annual Report claims an "open-architecture" software moat, the sheer scale of the firm's non-operating maneuvers suggests a traditional hardware-intensive burn rate that the Street hasn't properly priced into its valuation. The headline 25.09% ROE is an accounting mirage funded by the cannibalization of legacy Taoyuan real estate and the $250M Google transaction. However, HTC’s 4.7-year cash runway is genuine. If management can leverage government subsidies (e.g., Taiwan Creative Content Agency funding for the 2026 VPOP ASIA and *Gloomy Eyes* LBE releases) and mature recurring B2B subscriptions (such as the North American Axon police training VR), HTC may successfully incubate its O-RAN 5G and VIVERSE IP before the liquidity buffer expires.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."