Kodiak AI: Asset-Light DaaS Pivot Near Permian Basin as 82% Single-Client Concentration Signals Precarious Q2 2027 Runway

Date : 2026-06-04

Reading : 136

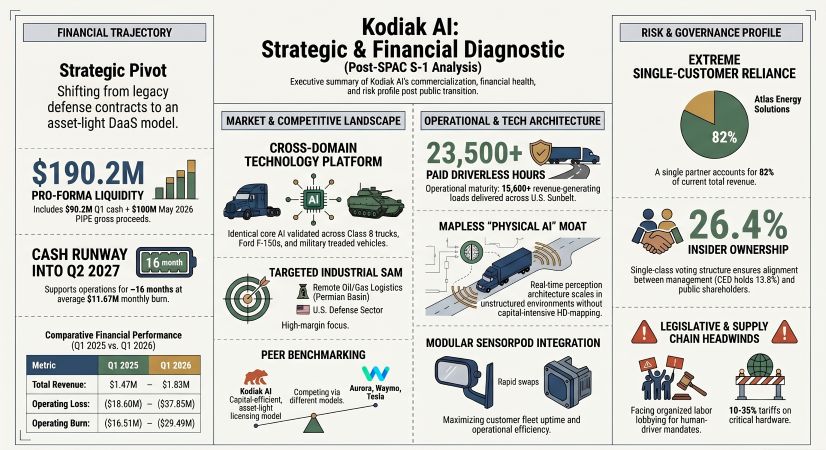

Kodiak AI’s shift to a Driver-as-a-Service (DaaS) model pivots the firm from episodic defense contracts to recurring software licensing. Yet, our forensic analysis reveals an acute vulnerability: an 82% revenue dependency on a single partner, Atlas Energy Solutions, in the Permian Basin. Despite a recent $100 million PIPE, the $9.8 million monthly cash burn and 10-35% supply chain tariffs dictate a rigid Q2 2027 survival deadline. For institutional LPs, executing Atlas’s 100-truck mandate is not merely a growth vector—it is an existential requirement.

DaaS Margin Inversion & Capital Runway Dynamics

Kodiak AI is executing a structural revenue migration, intentionally shedding asset-heavy military logistics (which historically represented 89% of FY 2023/2024 revenue) to capture high-margin, predictable DaaS subscriptions. While Q1 2026 top-line revenue demonstrated a 24% year-over-year recovery to $1.83 million, the fundamental unit economics remain deeply inverted.

The firm’s conservative accounting mandate—expensing 100% of R&D and software development costs—obscures the underlying technological capitalization but exposes a severe cash burn trajectory. Operations currently consume roughly $9.8 million per month. The balance sheet exhibits extreme leverage against future equity raises, necessitating the $100.0 million May 2026 Private Investment in Public Equity (PIPE) to stave off a "going concern" audit qualification.

Kodiak AI Segmental & Financial Inventory

* Top-Line Variance: FY 2025 total revenue contracted 75% YoY to $3.80 million, driven by a $12.3 million erosion in U.S. Army contracts. DaaS revenue subsequently surged, capturing 82% of the Q1 2026 revenue mix.

* Operating Leverage & Margin Deficit: The FY 2025 operating loss widened to $(112.63) million, yielding an operating margin of -2,966%. The Q1 2026 operating loss of $(37.85) million (-2,068% margin) highlights the severe near-term friction of scaling the physical fleet infrastructure.

* Capital Runway & Warrant Calculus: Baseline Q1 2026 liquidity of $90.19 million plus the $100.0 million May PIPE establishes a pro-forma baseline of ~$190.2 million, mathematically exhausting by Q2 2027. Full cash exercise of the 15,384,609 2026 PIPE Warrants (at a $6.00 strike) would inject an additional $92.3 million, extending survival to Q1 2028.

* Insider Debt Friction: The capital structure is burdened by a $10.0 million insider Second Lien Loan (held by a SPAC sponsor affiliate) maturing in October 2026, which accrues paid-in-kind (PIK) interest at an aggressively punitive rate of Prime + 9.00% (currently 16.50%).

* Commercial Validation Metrics: The network currently supports 28 customer-owned driverless vehicles, accumulating over 23,500 paid driverless hours and clearing 15,600+ revenue-generating loads across a 25,000-mile mapped network.

Figure Kodiak Al: Strategic & Financial Diagnostic

Supply Chain Audit: Permian Basin Integration & Tier-1 Tariff Exposure

Supply Chain Audit: Permian Basin Integration & Tier-1 Tariff Exposure

Kodiak AI's strategic moat relies on its "Mapless" real-time perception software and proprietary SensorPods, deliberately avoiding the brittle nature of High-Definition (HD) maps utilized by legacy competitors. However, the physical architecture required to support this physical AI ecosystem exposes the firm to acute geographical and geopolitical friction.

The commercial footprint is heavily concentrated in the U.S. Sunbelt. Operations are anchored by a 45,000 sq. ft. headquarters in Mountain View, California, a 75,000 sq. ft. main operational hub in Lancaster, Texas, and an 18,000 sq. ft. industrial staging facility in Odessa, Texas, purpose-built for Permian Basin oil and gas deployments.

Despite the software-centric DaaS model, Kodiak operates a highly vulnerable physical supply chain. The company relies on Bosch for Tier-1 hardware industrialization and Roush Industries for chassis upfitting. Silicon compute heavily depends on NXP Semiconductors (NASDAQ: NXPI), while cloud infrastructure and AI model training are locked into Amazon (NASDAQ: AMZN) AWS architectures spanning data centers in Santa Clara and Dallas.

Critically, single-source dependencies for LiDAR and radar components located in China, the EU, and Mexico expose the company to recent 10-35% U.S. import tariffs. This geographic exposure directly threatens the per-unit cost reduction required to achieve breakeven hardware margins. Furthermore, union-backed legislative lobbying in California, Colorado, and Maryland poses an existential threat to interstate scaling, attempting to mandate the physical presence of human drivers and effectively legislate the core Total Addressable Market (TAM) out of existence.

HDIN Institutional Perspective: Challenging the 'Asset-Light' Narrative

While management heavily markets the DaaS framework as a capital-efficient, software-first moat, our forensic audit of the S-1 suggests a traditional, hardware-intensive burn rate that the Street has not adequately priced in. The 107% year-over-year surge in "Truck & Freight Operations" expenses ($8.31 million in Q1 2026) indicates that the operational friction of deploying third-party upfitted vehicles remains extraordinarily high.

More alarmingly, Kodiak AI’s near-term viability is precariously tethered to a single counterparty. Atlas Energy Solutions accounts for 82% of current revenue and 73% of accounts receivable. With Atlas scheduled to evaluate a new truck platform in Q3 2026, the 100-truck deployment mandate faces a high probability of structural delay into 2027. If this anchor client churns or pauses procurement, Kodiak’s multi-phase Partner Deployment Program (PDP) pipeline lacks the immediate density to absorb the shock, threatening to exhaust the firm's $190.2 million pro-forma liquidity before sustainable unit economics can be realized.

Presentation Download & Video Access:

*Presentation Download:* Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

*Video Link:* Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

DaaS Margin Inversion & Capital Runway Dynamics

Kodiak AI is executing a structural revenue migration, intentionally shedding asset-heavy military logistics (which historically represented 89% of FY 2023/2024 revenue) to capture high-margin, predictable DaaS subscriptions. While Q1 2026 top-line revenue demonstrated a 24% year-over-year recovery to $1.83 million, the fundamental unit economics remain deeply inverted.

The firm’s conservative accounting mandate—expensing 100% of R&D and software development costs—obscures the underlying technological capitalization but exposes a severe cash burn trajectory. Operations currently consume roughly $9.8 million per month. The balance sheet exhibits extreme leverage against future equity raises, necessitating the $100.0 million May 2026 Private Investment in Public Equity (PIPE) to stave off a "going concern" audit qualification.

Kodiak AI Segmental & Financial Inventory

* Top-Line Variance: FY 2025 total revenue contracted 75% YoY to $3.80 million, driven by a $12.3 million erosion in U.S. Army contracts. DaaS revenue subsequently surged, capturing 82% of the Q1 2026 revenue mix.

* Operating Leverage & Margin Deficit: The FY 2025 operating loss widened to $(112.63) million, yielding an operating margin of -2,966%. The Q1 2026 operating loss of $(37.85) million (-2,068% margin) highlights the severe near-term friction of scaling the physical fleet infrastructure.

* Capital Runway & Warrant Calculus: Baseline Q1 2026 liquidity of $90.19 million plus the $100.0 million May PIPE establishes a pro-forma baseline of ~$190.2 million, mathematically exhausting by Q2 2027. Full cash exercise of the 15,384,609 2026 PIPE Warrants (at a $6.00 strike) would inject an additional $92.3 million, extending survival to Q1 2028.

* Insider Debt Friction: The capital structure is burdened by a $10.0 million insider Second Lien Loan (held by a SPAC sponsor affiliate) maturing in October 2026, which accrues paid-in-kind (PIK) interest at an aggressively punitive rate of Prime + 9.00% (currently 16.50%).

* Commercial Validation Metrics: The network currently supports 28 customer-owned driverless vehicles, accumulating over 23,500 paid driverless hours and clearing 15,600+ revenue-generating loads across a 25,000-mile mapped network.

Figure Kodiak Al: Strategic & Financial Diagnostic

Supply Chain Audit: Permian Basin Integration & Tier-1 Tariff ExposureKodiak AI's strategic moat relies on its "Mapless" real-time perception software and proprietary SensorPods, deliberately avoiding the brittle nature of High-Definition (HD) maps utilized by legacy competitors. However, the physical architecture required to support this physical AI ecosystem exposes the firm to acute geographical and geopolitical friction.

The commercial footprint is heavily concentrated in the U.S. Sunbelt. Operations are anchored by a 45,000 sq. ft. headquarters in Mountain View, California, a 75,000 sq. ft. main operational hub in Lancaster, Texas, and an 18,000 sq. ft. industrial staging facility in Odessa, Texas, purpose-built for Permian Basin oil and gas deployments.

Despite the software-centric DaaS model, Kodiak operates a highly vulnerable physical supply chain. The company relies on Bosch for Tier-1 hardware industrialization and Roush Industries for chassis upfitting. Silicon compute heavily depends on NXP Semiconductors (NASDAQ: NXPI), while cloud infrastructure and AI model training are locked into Amazon (NASDAQ: AMZN) AWS architectures spanning data centers in Santa Clara and Dallas.

Critically, single-source dependencies for LiDAR and radar components located in China, the EU, and Mexico expose the company to recent 10-35% U.S. import tariffs. This geographic exposure directly threatens the per-unit cost reduction required to achieve breakeven hardware margins. Furthermore, union-backed legislative lobbying in California, Colorado, and Maryland poses an existential threat to interstate scaling, attempting to mandate the physical presence of human drivers and effectively legislate the core Total Addressable Market (TAM) out of existence.

HDIN Institutional Perspective: Challenging the 'Asset-Light' Narrative

While management heavily markets the DaaS framework as a capital-efficient, software-first moat, our forensic audit of the S-1 suggests a traditional, hardware-intensive burn rate that the Street has not adequately priced in. The 107% year-over-year surge in "Truck & Freight Operations" expenses ($8.31 million in Q1 2026) indicates that the operational friction of deploying third-party upfitted vehicles remains extraordinarily high.

More alarmingly, Kodiak AI’s near-term viability is precariously tethered to a single counterparty. Atlas Energy Solutions accounts for 82% of current revenue and 73% of accounts receivable. With Atlas scheduled to evaluate a new truck platform in Q3 2026, the 100-truck deployment mandate faces a high probability of structural delay into 2027. If this anchor client churns or pauses procurement, Kodiak’s multi-phase Partner Deployment Program (PDP) pipeline lacks the immediate density to absorb the shock, threatening to exhaust the firm's $190.2 million pro-forma liquidity before sustainable unit economics can be realized.

Presentation Download & Video Access:

*Presentation Download:* Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

*Video Link:* Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*