Chengdu CRP Robot Technology: Aggressive Embodied AI Pivot Near The Chengdu Headquarters as -4.98% Net Margin Signals Severe Working Capital Constraints

Date : 2026-06-04

Reading : 263

Chengdu CRP Robot Technology’s Chapter 18C IPO filing reveals a structural divergence: a dominant 33.0% gross margin masked by chronically negative free cash flow (-$1.92M in 2025). Institutional LPs must weigh the company’s absolute leadership in China's $1.31B welding robot market against its extreme reliance on fiscal subsidies, which comprised 1,224.8% of 2023 pre-tax profit. As the firm scales its 40,000 sqm Chengdu facility to push embodied AI, the impending depreciation drag and persistent US semiconductor dependencies (ECCN 3A991) threaten to erode near-term earnings quality.

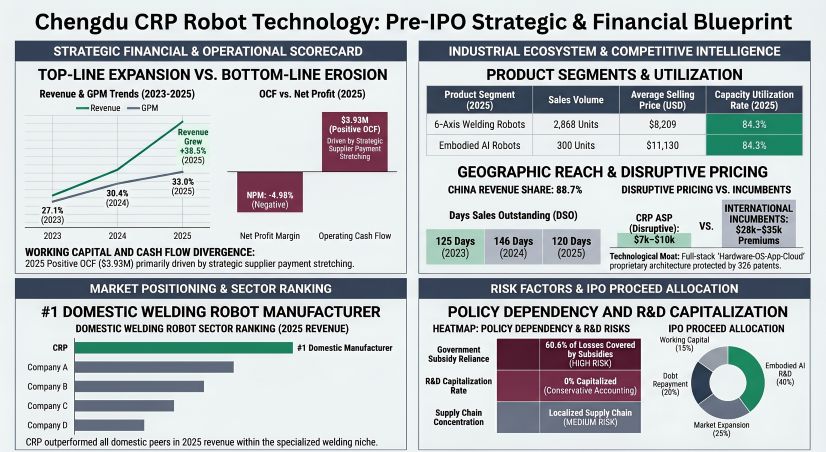

Figure Chengdu CRP Robot Technology: Pre-lPo Strategic & Financial Blueprint

Forensic Analysis of Price-Mix Variance, Capital Allocation & Profitability Metrics

Forensic Analysis of Price-Mix Variance, Capital Allocation & Profitability Metrics

The company’s transition from standard controllers to a proprietary Hardware-OS-App-Cloud ecosystem has generated robust top-line accretion, yet operating leverage remains severely compressed by customer acquisition costs and R&D intensity (15.1% of 2025 revenue).

Table: Corporate Financial Inventory & FCF Conversion (USD Millions)

*Note: Financials converted at 1 USD = 7.1875 CNY. Tax rate effectively 0% due to 15% High-Tech Enterprise status, 100% R&D deduction, and $9.45M in unrecognized tax losses.*

Unit Economics & Segmental Price-Mix Variance:

The company enforces aggressive pricing concessions to seize market share from international incumbents, leading to explicit Average Selling Price (ASP) dilution across its flagship models:

* Six-Axis Welding Robots (Core): Volume scaled from 1,893 units (2023) to 2,868 units (2025). ASP contracted from $9,183 to $8,209, driven by the rollout of the lower-priced PRO series.

* Six-Axis Multi-Functional Robots: Volume increased to 1,623 units in 2025, but ASP dropped sharply from $8,069 (2023) to $6,817 (2025) as the company aggressively penetrated the automotive and 3C electronics sectors.

* Four-Axis Robots (SCARA/Palletizing): Maintained firm pricing power (ASP: $4,591 in 2023 vs. $4,730 in 2025) on 411 units.

* Collaborative Robots (Cobots): Exponential volume growth from 7 units (2023) to 358 units (2025), with ASP accretive from $8,765 to $9,461.

* Embodied AI Robots: Volume reached 300 units in 2025. ASP plummeted from $16,000 to $11,130 following a strategic block order for a state-owned energy enterprise.

Capital Allocation & Intellectual Property Asset Base:

The company’s R&D moat is anchored by 141 engineering personnel (33.3% of the total workforce) operating at a localized cost structure of $31,489 per head. The proprietary IP ecosystem includes 326 patents, 44 software copyrights, and 114 trademarks. Core kinematics patents expire in April 2032, while next-gen AI algorithms remain protected until 2040–2043. Share-based payments accelerated to $0.92M in 2025 via the Changzhou Hongzhi ESOP, effectively front-loading compensation expenses without diluting public float structurally.

Sub-Tier Supplier Exfiltration & Chengdu-Malaysia Geopolitical Routing

Physicality & Geographic Footprint:

The company’s operational nerve center is located in Chengdu, Sichuan Province, currently utilizing 35,155.85 sqm of floor space. To mitigate international friction, the firm established CRP Robot Malaysia Sdn. Bhd. (a 205 sqm facility) as its Southeast Asia hub. Over 88.7% of 2025 revenue ($39.99M) was domestic, driven by demand clusters in Guangdong, Jiangsu, and Shandong. Overseas expansion outlines localized centers across Delhi, Chennai, Italy, Germany, and Mexico by 2026.

Supply Chain Dependencies & EAR Export Controls:

* Tier-1 Localization: 95.0% of procurement value is domestic. Top 5 suppliers accounted for 37.9% ($12.13M) of 2025 purchases.

* Related-Party Sourcing: Zhejiang Huandong Robot Joint Technology (Supplier A)—a subsidiary of minority shareholder Shuanghuan Transmission—is the primary vendor for RV reducers, accounting for $6.46M in 2025 on arm’s-length terms.

* Silicon Bottleneck: The critical risk node lies in imported US-origin Digital Signal Processing (DSP) chips classified under ECCN 3A991. While currently comprising only 0.65% of finished product value (avoiding the 25% US EAR de minimis threshold), management targets complete domestic substitution by 2026.

Litigation & Compliance Liabilities:

The balance sheet lacks formal litigation provisions, yet carries a latent $3.53M social security and housing fund arrears shortfall, posing a maximum administrative penalty risk of $8.64M. Further, two domestic leased properties lack proper master lease registrations, exposing the entity to minor $2,782 fines.

HDIN Differentiated Viewpoint: The "Positive OCF" Accounting Mirage & 157% Capacity Trap

While the S-1 prospectus emphasizes a triumphant turnaround to a positive $3.93M Operating Cash Flow in 2025, HDIN Research challenges this as an accounting artifact. The underlying cash conversion cycle reveals a severe working capital squeeze: Days Sales Outstanding (DSO) remains bloated at 120 days, and the 2025 OCF was artificially salvaged by a massive $10.69M spike in trade and notes payables (stretching DPO to 80 days). The company is not organically generating cash; it is aggressively deferring supplier payments to mask the $5.71M drain from uncollected receivables and a $3.49M inventory accumulation (heavily skewed toward raw materials at $11.54M).

Furthermore, the structural viability of the CapEx pipeline is highly questionable. Management aims to increase design capacity from 7,000 units (running at 84.3% utilization) to 15,000 units by 2026, and 18,000 units by 2030 via a new 40,000 sqm Chengdu facility. This 157% capacity surge far outpaces the 14.8% projected CAGR of the broader Chinese industrial robotics sector. If macroeconomic CapEx tightening limits market digestion, the resulting unabsorbed fixed costs and immediate depreciation drag will fundamentally break the company's near-term profitability, negating the premium margins of its Embodied AI rollout.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Chengdu CRP Robot Technology: Pre-lPo Strategic & Financial Blueprint

Forensic Analysis of Price-Mix Variance, Capital Allocation & Profitability MetricsThe company’s transition from standard controllers to a proprietary Hardware-OS-App-Cloud ecosystem has generated robust top-line accretion, yet operating leverage remains severely compressed by customer acquisition costs and R&D intensity (15.1% of 2025 revenue).

Table: Corporate Financial Inventory & FCF Conversion (USD Millions)

| Metric | 2023 | 2024 | 2025 | YoY '25 |

|---|---|---|---|---|

| Total Revenue | $30.94M | $32.56M | $45.11M | +38.5% |

| Gross Profit (Margin) | $8.38M (27.1%) | $9.91M (30.4%) | $14.87M (33.0%) | +50.0% |

| Net Profit / (Loss) | $0.23M | ($1.80M) | ($2.25M) | N/A |

| Pre-Tax Profit (NPBT) | $0.23M | ($1.80M) | ($2.25M) | N/A |

| Government Subsidies | $2.88M | $1.41M | $1.36M | -3.5% |

| Subsidies as % of NPBT | 1224.8% | 78.3% | 60.6% | N/A |

| R&D Expenditure | $5.00M | $5.01M | $6.80M | +35.9% |

| R&D Capitalization | $0.09M | $0.00 | $0.10M | N/A |

| Operating Cash Flow (OCF) | ($4.30M) | ($2.47M) | $3.93M | N/A |

| Capital Expenditure (CapEx) | $0.60M | $1.24M | $5.86M | +372.5% |

| Free Cash Flow (FCF) | ($4.89M) | ($3.71M) | ($1.92M) | N/A |

Unit Economics & Segmental Price-Mix Variance:

The company enforces aggressive pricing concessions to seize market share from international incumbents, leading to explicit Average Selling Price (ASP) dilution across its flagship models:

* Six-Axis Welding Robots (Core): Volume scaled from 1,893 units (2023) to 2,868 units (2025). ASP contracted from $9,183 to $8,209, driven by the rollout of the lower-priced PRO series.

* Six-Axis Multi-Functional Robots: Volume increased to 1,623 units in 2025, but ASP dropped sharply from $8,069 (2023) to $6,817 (2025) as the company aggressively penetrated the automotive and 3C electronics sectors.

* Four-Axis Robots (SCARA/Palletizing): Maintained firm pricing power (ASP: $4,591 in 2023 vs. $4,730 in 2025) on 411 units.

* Collaborative Robots (Cobots): Exponential volume growth from 7 units (2023) to 358 units (2025), with ASP accretive from $8,765 to $9,461.

* Embodied AI Robots: Volume reached 300 units in 2025. ASP plummeted from $16,000 to $11,130 following a strategic block order for a state-owned energy enterprise.

Capital Allocation & Intellectual Property Asset Base:

The company’s R&D moat is anchored by 141 engineering personnel (33.3% of the total workforce) operating at a localized cost structure of $31,489 per head. The proprietary IP ecosystem includes 326 patents, 44 software copyrights, and 114 trademarks. Core kinematics patents expire in April 2032, while next-gen AI algorithms remain protected until 2040–2043. Share-based payments accelerated to $0.92M in 2025 via the Changzhou Hongzhi ESOP, effectively front-loading compensation expenses without diluting public float structurally.

Sub-Tier Supplier Exfiltration & Chengdu-Malaysia Geopolitical Routing

Physicality & Geographic Footprint:

The company’s operational nerve center is located in Chengdu, Sichuan Province, currently utilizing 35,155.85 sqm of floor space. To mitigate international friction, the firm established CRP Robot Malaysia Sdn. Bhd. (a 205 sqm facility) as its Southeast Asia hub. Over 88.7% of 2025 revenue ($39.99M) was domestic, driven by demand clusters in Guangdong, Jiangsu, and Shandong. Overseas expansion outlines localized centers across Delhi, Chennai, Italy, Germany, and Mexico by 2026.

Supply Chain Dependencies & EAR Export Controls:

* Tier-1 Localization: 95.0% of procurement value is domestic. Top 5 suppliers accounted for 37.9% ($12.13M) of 2025 purchases.

* Related-Party Sourcing: Zhejiang Huandong Robot Joint Technology (Supplier A)—a subsidiary of minority shareholder Shuanghuan Transmission—is the primary vendor for RV reducers, accounting for $6.46M in 2025 on arm’s-length terms.

* Silicon Bottleneck: The critical risk node lies in imported US-origin Digital Signal Processing (DSP) chips classified under ECCN 3A991. While currently comprising only 0.65% of finished product value (avoiding the 25% US EAR de minimis threshold), management targets complete domestic substitution by 2026.

Litigation & Compliance Liabilities:

The balance sheet lacks formal litigation provisions, yet carries a latent $3.53M social security and housing fund arrears shortfall, posing a maximum administrative penalty risk of $8.64M. Further, two domestic leased properties lack proper master lease registrations, exposing the entity to minor $2,782 fines.

HDIN Differentiated Viewpoint: The "Positive OCF" Accounting Mirage & 157% Capacity Trap

While the S-1 prospectus emphasizes a triumphant turnaround to a positive $3.93M Operating Cash Flow in 2025, HDIN Research challenges this as an accounting artifact. The underlying cash conversion cycle reveals a severe working capital squeeze: Days Sales Outstanding (DSO) remains bloated at 120 days, and the 2025 OCF was artificially salvaged by a massive $10.69M spike in trade and notes payables (stretching DPO to 80 days). The company is not organically generating cash; it is aggressively deferring supplier payments to mask the $5.71M drain from uncollected receivables and a $3.49M inventory accumulation (heavily skewed toward raw materials at $11.54M).

Furthermore, the structural viability of the CapEx pipeline is highly questionable. Management aims to increase design capacity from 7,000 units (running at 84.3% utilization) to 15,000 units by 2026, and 18,000 units by 2030 via a new 40,000 sqm Chengdu facility. This 157% capacity surge far outpaces the 14.8% projected CAGR of the broader Chinese industrial robotics sector. If macroeconomic CapEx tightening limits market digestion, the resulting unabsorbed fixed costs and immediate depreciation drag will fundamentally break the company's near-term profitability, negating the premium margins of its Embodied AI rollout.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."