Lupeng Pharmaceutical: Commercial Pivot Near Guangzhou Headquarters as $101.4M Out-Licensing Signals Pre-IPO Runway Extension

Date : 2026-06-05

Reading : 104

Lupeng Pharmaceutical’s transition to a commercial-stage entity hinges on its proprietary BeyondX platform. While the 2025 headline net loss of $28.85 million appears severe, our forensic audit isolates a normalized operating burn of $20.08 million, stabilized by a $101.4 million regional out-licensing pact. For institutional LPs, the critical metric is the 21-month pre-IPO cash runway bridging the gap to the 2026 conditional NDA launch of LP-168. The firm must execute its dual-engine commercialization strategy amidst rising geopolitical supply chain constraints and an impending 2039 patent cliff.

Forensic Financials & Capital Architecture Audit

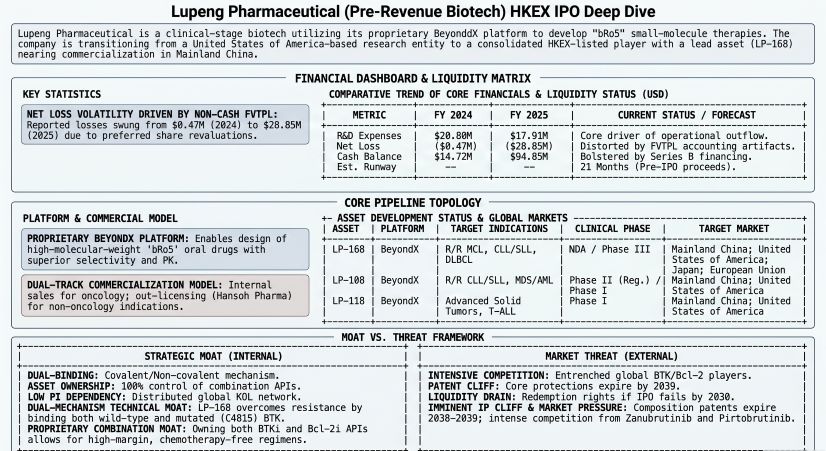

Lupeng’s pre-commercial financial profile requires strict bifurcation between statutory accounting artifacts and actual cash burn. The 2025 financial statements reflect a heavy capitalization phase, driven by late-stage clinical execution and IPO preparation.

Figure Lupeng Pharmaceutical (Pre-Revenue Biotech) HKEX IPO Deep Dive

Segmental Financial Inventory (FY24 vs. FY25)

* Top-Line Revenue: $0 in FY24 to $4,461,356 in FY25 (100% derived from the Hansoh Pharma out-licensing upfront and tech-transfer milestones).

* R&D Expenditures: Decreased 13.9% from $20,802,087 (FY24) to $17,905,530 (FY25), perfectly correlating with the December 2024 completion of the LP-168 Phase II registrational trial for R/R MCL.

* Administrative Expenses: Surged 119% from $3,543,096 to $7,774,748 in FY25, driven by professional service fees for Series B financing and IPO structuring.

* Net Cash Used in Operations: $15,781,843 (FY24) rising to $17,350,122 (FY25).

* Cash Equivalents: Scaled from $14,724,591 (FY24) to $94,849,669 (FY25).

Forensic Margin & Capital Allocation Analysis:

The headline net loss explosion—from $470,956 in 2024 to $28,852,591 in 2025—is an accounting distortion. The 2024 figure was artificially suppressed by a $22.25 million Fair Value Through Profit or Loss (FVTPL) gain on preferred shares and $961,670 in government grants, masking a true core operating deficit of ~$23.68 million. In 2025, a $10.28 million FVTPL paper loss normalized the statutory net loss.

Lupeng's balance sheet currently carries a net liability position of $148.58 million, entirely driven by $240.71 million in convertible redeemable preferred shares. Upon a successful HKEX listing, these will convert to equity, instantly stabilizing the balance sheet. However, the Series B financing was a clear down-round—post-money valuation dropped from $420.0 million (Series Pre-B) to $311.25 million in 2025 due to macroeconomic biotech headwinds. To offset this, Lupeng executed an anti-dilution adjustment, altering the Pre-B to ordinary share conversion ratio from 1:1 to 1:1.2185.

To bridge the gap to commercialization, management projects the historical monthly cash burn of $1.47 million will accelerate 3.1x to $4.56 million to fund the 2026 Phase III head-to-head trials. Independent of IPO proceeds, the current $94.85 million liquidity pool guarantees a 21-month operating runway.

Asset-Light Supply Chain & Trans-Pacific Clinical Infrastructure

Lupeng operates a bifurcated geographic and operational model, centralizing its global headquarters and primary R&D in Guangzhou, China, supported by satellite R&D centers in Beijing, Hangzhou, and Shanghai. US-based clinical operations are anchored by its California subsidiary, Newave.

Manufacturing & Geo-Economic Moat:

The company enforces a strictly asset-light physical footprint. While it retains internal Chemistry, Manufacturing, and Controls (CMC) for non-GMP kilo-scale lead production, it owns zero commercial manufacturing facilities. Consequently, Lupeng relies 100% on third-party Contract Development and Manufacturing Organizations (CDMOs) for clinical and commercial supply.

This total reliance on external CDMOs exposes the firm to geopolitical friction, specifically the U.S. BIOSECURE Act. If Lupeng's Tier-1 supply partners are designated as "companies of concern," the disruption to US-based Phase III trials (such as the 2L R/R CLL/SLL trial led by US KOLs) would be severe. To mitigate supply chain bottlenecks for combination therapies, Lupeng has locked in framework supply agreements with independent providers for R-CHOP, azacitidine, and ponatinib, mandating minimum supply guarantees.

Targeted Commercial Footprint:

Lupeng is currently scaling an 80-person internal commercial team for deployment by the end of 2026 across North, South, and East China. Rather than a fragmented rollout, the team is aggressively targeting a highly concentrated demographic: the top 500 Class III hospitals, with a hyper-focus on the top 100 to 150 specialized oncology centers.

HDIN Institutional Perspective: The "Dual-Engine" Valuation Dilemma

Challenge: While the Street may penalize Lupeng for the Series B down-round and its severe $148.58 million net liability position, our forensic analysis suggests the market is mispricing the structural economics of its clinical pipeline.

Lupeng’s true economic moat is not merely the standalone efficacy of LP-168 (which demonstrated an 89.3% ORR in BTKi-naive 2L MCL), but its "dual-engine" combination therapy strategy combining LP-168 (BTKi) and LP-108 (Bcl-2i). Because Lupeng internally developed and wholly owns the APIs for both compounds, it captures 100% of the unit economics. Competitors attempting similar dual-regimens must engage in cross-licensing, suffering severe royalty stacking and margin erosion.

Furthermore, the executive leadership brings highly relevant commercialization alpha. CEO Dr. Fenlai TAN's tenure as CMO at SZSE: 300558 (Betta Pharmaceuticals) and CFO Zhengqing ZHOU's financial governance experience at NASDAQ: BGNE (BeiGene) indicate a management team pre-calibrated for public market capital allocation. However, the clock is ticking: Lupeng must secure China NRDL inclusion immediately post-approval in 2026 to maximize its extraction window before the foundational composition patents for LP-168 expire in 2039.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Forensic Financials & Capital Architecture Audit

Lupeng’s pre-commercial financial profile requires strict bifurcation between statutory accounting artifacts and actual cash burn. The 2025 financial statements reflect a heavy capitalization phase, driven by late-stage clinical execution and IPO preparation.

Figure Lupeng Pharmaceutical (Pre-Revenue Biotech) HKEX IPO Deep Dive

Segmental Financial Inventory (FY24 vs. FY25)

* Top-Line Revenue: $0 in FY24 to $4,461,356 in FY25 (100% derived from the Hansoh Pharma out-licensing upfront and tech-transfer milestones).

* R&D Expenditures: Decreased 13.9% from $20,802,087 (FY24) to $17,905,530 (FY25), perfectly correlating with the December 2024 completion of the LP-168 Phase II registrational trial for R/R MCL.

* Administrative Expenses: Surged 119% from $3,543,096 to $7,774,748 in FY25, driven by professional service fees for Series B financing and IPO structuring.

* Net Cash Used in Operations: $15,781,843 (FY24) rising to $17,350,122 (FY25).

* Cash Equivalents: Scaled from $14,724,591 (FY24) to $94,849,669 (FY25).

Forensic Margin & Capital Allocation Analysis:

The headline net loss explosion—from $470,956 in 2024 to $28,852,591 in 2025—is an accounting distortion. The 2024 figure was artificially suppressed by a $22.25 million Fair Value Through Profit or Loss (FVTPL) gain on preferred shares and $961,670 in government grants, masking a true core operating deficit of ~$23.68 million. In 2025, a $10.28 million FVTPL paper loss normalized the statutory net loss.

Lupeng's balance sheet currently carries a net liability position of $148.58 million, entirely driven by $240.71 million in convertible redeemable preferred shares. Upon a successful HKEX listing, these will convert to equity, instantly stabilizing the balance sheet. However, the Series B financing was a clear down-round—post-money valuation dropped from $420.0 million (Series Pre-B) to $311.25 million in 2025 due to macroeconomic biotech headwinds. To offset this, Lupeng executed an anti-dilution adjustment, altering the Pre-B to ordinary share conversion ratio from 1:1 to 1:1.2185.

To bridge the gap to commercialization, management projects the historical monthly cash burn of $1.47 million will accelerate 3.1x to $4.56 million to fund the 2026 Phase III head-to-head trials. Independent of IPO proceeds, the current $94.85 million liquidity pool guarantees a 21-month operating runway.

Asset-Light Supply Chain & Trans-Pacific Clinical Infrastructure

Lupeng operates a bifurcated geographic and operational model, centralizing its global headquarters and primary R&D in Guangzhou, China, supported by satellite R&D centers in Beijing, Hangzhou, and Shanghai. US-based clinical operations are anchored by its California subsidiary, Newave.

Manufacturing & Geo-Economic Moat:

The company enforces a strictly asset-light physical footprint. While it retains internal Chemistry, Manufacturing, and Controls (CMC) for non-GMP kilo-scale lead production, it owns zero commercial manufacturing facilities. Consequently, Lupeng relies 100% on third-party Contract Development and Manufacturing Organizations (CDMOs) for clinical and commercial supply.

This total reliance on external CDMOs exposes the firm to geopolitical friction, specifically the U.S. BIOSECURE Act. If Lupeng's Tier-1 supply partners are designated as "companies of concern," the disruption to US-based Phase III trials (such as the 2L R/R CLL/SLL trial led by US KOLs) would be severe. To mitigate supply chain bottlenecks for combination therapies, Lupeng has locked in framework supply agreements with independent providers for R-CHOP, azacitidine, and ponatinib, mandating minimum supply guarantees.

Targeted Commercial Footprint:

Lupeng is currently scaling an 80-person internal commercial team for deployment by the end of 2026 across North, South, and East China. Rather than a fragmented rollout, the team is aggressively targeting a highly concentrated demographic: the top 500 Class III hospitals, with a hyper-focus on the top 100 to 150 specialized oncology centers.

HDIN Institutional Perspective: The "Dual-Engine" Valuation Dilemma

Challenge: While the Street may penalize Lupeng for the Series B down-round and its severe $148.58 million net liability position, our forensic analysis suggests the market is mispricing the structural economics of its clinical pipeline.

Lupeng’s true economic moat is not merely the standalone efficacy of LP-168 (which demonstrated an 89.3% ORR in BTKi-naive 2L MCL), but its "dual-engine" combination therapy strategy combining LP-168 (BTKi) and LP-108 (Bcl-2i). Because Lupeng internally developed and wholly owns the APIs for both compounds, it captures 100% of the unit economics. Competitors attempting similar dual-regimens must engage in cross-licensing, suffering severe royalty stacking and margin erosion.

Furthermore, the executive leadership brings highly relevant commercialization alpha. CEO Dr. Fenlai TAN's tenure as CMO at SZSE: 300558 (Betta Pharmaceuticals) and CFO Zhengqing ZHOU's financial governance experience at NASDAQ: BGNE (BeiGene) indicate a management team pre-calibrated for public market capital allocation. However, the clock is ticking: Lupeng must secure China NRDL inclusion immediately post-approval in 2026 to maximize its extraction window before the foundational composition patents for LP-168 expire in 2039.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."