INVO Fertility: B2C Clinic Consolidation Near Wisconsin and Georgia Hubs as Extreme Dilution Signals 2026 Solvency Risk

Date : 2026-06-05

Reading : 145

INVO Fertility's transition from an Assisted Reproductive Technology (ART) device distributor to a vertically integrated U.S. clinic operator successfully drove FY2025 revenue to $6.8 million. However, institutional investors face a structurally compromised capitalization table. Facing a massive $91.4 million accumulated deficit and systemic post-Roe legislative volatility in key markets like Alabama, management's reliance on highly dilutive financing and compounding reverse splits has yielded a 57,300% surge in share count. The enterprise's survival now hinges entirely on servicing rigid 2026 settlement liabilities against a distressed working capital deficit.

Figure INVO Fertility's Distressed Transition to Clinical Operations

Forensic Analysis of INVO Fertility Financials & Capital Structure

Forensic Analysis of INVO Fertility Financials & Capital Structure

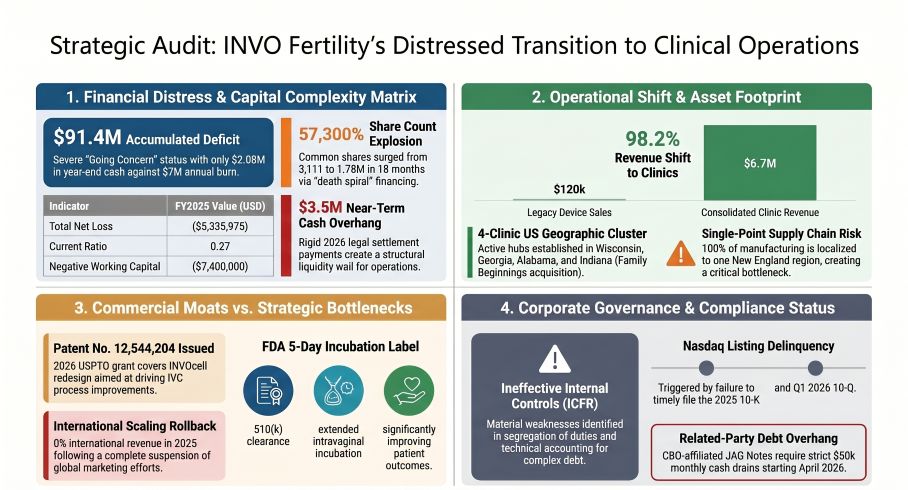

A forensic examination of NASDAQ: INVO reveals a business model fundamentally transformed, yet paralyzed by its own capitalization mechanics. The shift from low-margin device sales (yielding hundreds of dollars per unit) to full clinical cycles (yielding thousands of dollars) is complete, but extreme capital engineering has fundamentally subordinated common equityholders.

* Top-Line Architecture (FY2025): Total consolidated revenue reached $6,841,250 (+4.73% YoY). The core clinic segment generated $6,721,057, capturing 98.2% of total top-line, while legacy 3rd-party product sales collapsed to a supplementary $120,193 (1.8%). Total system-wide clinical revenue, including the unconsolidated Alabama VIE ($1,300,872), reached $8,021,929.

* Operating Leverage & Margins: Total operating expenses climbed 6.98% YoY to $14.07 million. Research & Development was zeroed out entirely (from $4,880 in 2024 to $0), while SG&A contracted 4.64% to $7.69 million. The company posted a net loss from continuing operations of $5.33 million (a 31.06% YoY improvement).

* Liquidity Wall & Solvency Crisis: The December 31, 2025, cash balance sat at an anemic $2,077,842. Against $10.33 million in current liabilities, the current ratio rests at a severely distressed 0.27 (negative working capital of $7.4 million). Operations consumed $7.0 million in cash during FY2025.

* Liabilities & 2026 Commitments: Operating cash flows are heavily encumbered by the $6.0 million Pritts Settlement tied to the Wisconsin Fertility Institute (WFI). The company faces rigid cash drain milestones of $3.5 million in 2026 ($1M on March 31, $2M on June 30, $0.5M on December 31). Additionally, a $660,000 principal JAG Multi Investments note demands $50,000 monthly sweeps starting April 2026, alongside escalating penalty multipliers (+0.30x total) on the Decathlon Revenue Loan (maturing June 2028).

* Hyper-Dilution Mechanics: To survive, the company utilized four compounding reverse stock splits (1-for-12, 1-for-3, 1-for-8, 1-for-5) alongside continuous warrant inducements (including a $7.5 million January 2026 capital injection at $7.95/share) and Series C-2 Preferred extinguishments. Outstanding common shares exploded from 3,111 in December 2024 to 1,786,035 by June 2026—a ~57,300% increase.

* Deconsolidation of NAYA Therapeutics (NTI): Divesting its 80.1% stake in NTI in June 2025 triggered a $16.45 million loss from discontinued operations (including a $14.64 million goodwill impairment), successfully cleansing the balance sheet of speculative In-Process R&D. INVO retained a 19.9% minority stake and a $4.8 million secured convertible note maturing November 2026.

Supply Chain Audit & Geo-Economic Moat

INVO Fertility has entirely localized its operations, abandoning its historically fragmented international distribution (zero sales outside the US in FY2025). This insulates the company from global freight volatility but centralizes clinical exposure within distinct US territories.

* Clinical Footprint: The enterprise generates its primary cash flow from the wholly-owned Wisconsin Fertility Institute (a 9,680 sq. ft. facility in Middleton, WI) and its Bloom INVO LLC joint venture in Atlanta, Georgia. Expanding its geographic reach, the company executed a post-balance-sheet acquisition of Family Beginnings in Indianapolis, Indiana (a 4,387 sq. ft. leased facility) on February 18, 2026, for $760,000. It also guarantees a $300,000 lease liability for its unconsolidated Birmingham, Alabama clinic.

* Physical Single-Point-of-Failure: The manufacturing of the proprietary INVOcell device is 100% localized within the New England region. The company operates a highly concentrated supply chain reliant entirely on NextPhase Medical Devices for final assembly, alongside molded component suppliers R.E.C. Manufacturing Corporation and Casco Bay Molding. Any disruption here threatens the entire clinic network's Intravaginal Culture (IVC) procedural capacity.

* Regulatory & IP Defensibility: On February 10, 2026, the USPTO granted Patent No. 12,544,204 for an IVC device redesign, fortifying a moat previously widened by an FDA 510(k) clearance allowing a 5-day incubation period. However, operations remain acutely vulnerable to shifting embryo personhood laws, explicitly highlighted by the 2024 Alabama Supreme Court ruling, which arbitrarily injects legal risk into regional ART services.

HDIN Institutional Perspective

While management aggressively touts the margin expansion of owning domestic fertility clinics and capturing thousands of dollars per full fertility cycle, the underlying execution has fatally compromised the balance sheet. The capitalization table is a textbook example of "death spiral" financing. The $7.0 million historical operating cash burn, compounded by ineffective internal controls triggering April and May 2026 Nasdaq delinquency notices, dictates that any future top-line growth is functionally subordinated to predatory convertible debt. The rigid 2026 obligations—specifically the $3.5 million Pritts settlement and callable executive/related-party demand notes—leave no margin for error. Despite shedding the massive operational drag of NAYA Therapeutics, the core fertility entity remains structurally insolvent without continuous, value-destructive equity liquidations.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure INVO Fertility's Distressed Transition to Clinical Operations

Forensic Analysis of INVO Fertility Financials & Capital StructureA forensic examination of NASDAQ: INVO reveals a business model fundamentally transformed, yet paralyzed by its own capitalization mechanics. The shift from low-margin device sales (yielding hundreds of dollars per unit) to full clinical cycles (yielding thousands of dollars) is complete, but extreme capital engineering has fundamentally subordinated common equityholders.

* Top-Line Architecture (FY2025): Total consolidated revenue reached $6,841,250 (+4.73% YoY). The core clinic segment generated $6,721,057, capturing 98.2% of total top-line, while legacy 3rd-party product sales collapsed to a supplementary $120,193 (1.8%). Total system-wide clinical revenue, including the unconsolidated Alabama VIE ($1,300,872), reached $8,021,929.

* Operating Leverage & Margins: Total operating expenses climbed 6.98% YoY to $14.07 million. Research & Development was zeroed out entirely (from $4,880 in 2024 to $0), while SG&A contracted 4.64% to $7.69 million. The company posted a net loss from continuing operations of $5.33 million (a 31.06% YoY improvement).

* Liquidity Wall & Solvency Crisis: The December 31, 2025, cash balance sat at an anemic $2,077,842. Against $10.33 million in current liabilities, the current ratio rests at a severely distressed 0.27 (negative working capital of $7.4 million). Operations consumed $7.0 million in cash during FY2025.

* Liabilities & 2026 Commitments: Operating cash flows are heavily encumbered by the $6.0 million Pritts Settlement tied to the Wisconsin Fertility Institute (WFI). The company faces rigid cash drain milestones of $3.5 million in 2026 ($1M on March 31, $2M on June 30, $0.5M on December 31). Additionally, a $660,000 principal JAG Multi Investments note demands $50,000 monthly sweeps starting April 2026, alongside escalating penalty multipliers (+0.30x total) on the Decathlon Revenue Loan (maturing June 2028).

* Hyper-Dilution Mechanics: To survive, the company utilized four compounding reverse stock splits (1-for-12, 1-for-3, 1-for-8, 1-for-5) alongside continuous warrant inducements (including a $7.5 million January 2026 capital injection at $7.95/share) and Series C-2 Preferred extinguishments. Outstanding common shares exploded from 3,111 in December 2024 to 1,786,035 by June 2026—a ~57,300% increase.

* Deconsolidation of NAYA Therapeutics (NTI): Divesting its 80.1% stake in NTI in June 2025 triggered a $16.45 million loss from discontinued operations (including a $14.64 million goodwill impairment), successfully cleansing the balance sheet of speculative In-Process R&D. INVO retained a 19.9% minority stake and a $4.8 million secured convertible note maturing November 2026.

Supply Chain Audit & Geo-Economic Moat

INVO Fertility has entirely localized its operations, abandoning its historically fragmented international distribution (zero sales outside the US in FY2025). This insulates the company from global freight volatility but centralizes clinical exposure within distinct US territories.

* Clinical Footprint: The enterprise generates its primary cash flow from the wholly-owned Wisconsin Fertility Institute (a 9,680 sq. ft. facility in Middleton, WI) and its Bloom INVO LLC joint venture in Atlanta, Georgia. Expanding its geographic reach, the company executed a post-balance-sheet acquisition of Family Beginnings in Indianapolis, Indiana (a 4,387 sq. ft. leased facility) on February 18, 2026, for $760,000. It also guarantees a $300,000 lease liability for its unconsolidated Birmingham, Alabama clinic.

* Physical Single-Point-of-Failure: The manufacturing of the proprietary INVOcell device is 100% localized within the New England region. The company operates a highly concentrated supply chain reliant entirely on NextPhase Medical Devices for final assembly, alongside molded component suppliers R.E.C. Manufacturing Corporation and Casco Bay Molding. Any disruption here threatens the entire clinic network's Intravaginal Culture (IVC) procedural capacity.

* Regulatory & IP Defensibility: On February 10, 2026, the USPTO granted Patent No. 12,544,204 for an IVC device redesign, fortifying a moat previously widened by an FDA 510(k) clearance allowing a 5-day incubation period. However, operations remain acutely vulnerable to shifting embryo personhood laws, explicitly highlighted by the 2024 Alabama Supreme Court ruling, which arbitrarily injects legal risk into regional ART services.

HDIN Institutional Perspective

While management aggressively touts the margin expansion of owning domestic fertility clinics and capturing thousands of dollars per full fertility cycle, the underlying execution has fatally compromised the balance sheet. The capitalization table is a textbook example of "death spiral" financing. The $7.0 million historical operating cash burn, compounded by ineffective internal controls triggering April and May 2026 Nasdaq delinquency notices, dictates that any future top-line growth is functionally subordinated to predatory convertible debt. The rigid 2026 obligations—specifically the $3.5 million Pritts settlement and callable executive/related-party demand notes—leave no margin for error. Despite shedding the massive operational drag of NAYA Therapeutics, the core fertility entity remains structurally insolvent without continuous, value-destructive equity liquidations.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."