CopperTech Metals: $2.7B Capex Expansion Near Zambian Copperbelt as Margin Compression Signals Severe Liquidity Deficit

Date : 2026-06-05

Reading : 159

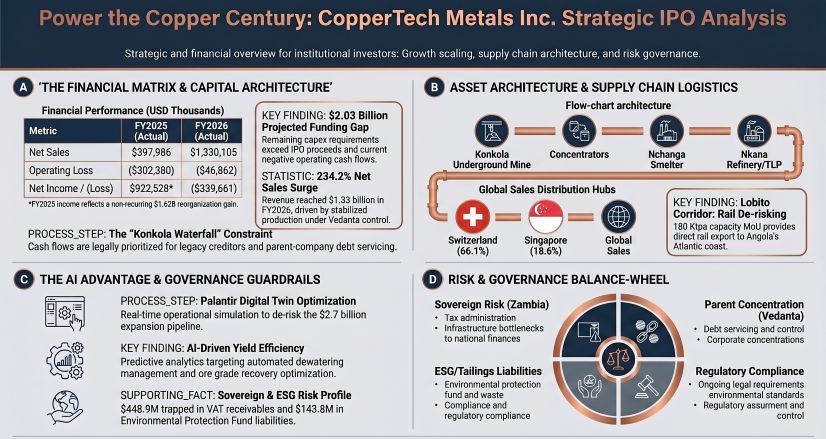

CopperTech Metals faces a severe structural paradox: a 234% FY2026 revenue surge to $1.33 billion masks a critical $339.7 million net loss and negative free cash flow conversion. While the U.S.-backed Lobito Corridor positions the Konkola asset as a vital geopolitical hedge against Chinese refining monopolies, the company’s aggressive 270 Ktpa production target is constrained by a $2.03 billion funding gap and a crippling $448.9 million Zambian VAT trap. For institutional LPs, the immediate equity narrative rests on overcoming profound hydrological dewatering costs and complex related-party debt waterfalls.

Figure Power the Copper Century: CopperTech Metals Inc Strategic lPO Analysis

Segmental Margins & Capital Structure Vulnerabilities

Segmental Margins & Capital Structure Vulnerabilities

Despite top-line expansion driven by the resumption of operational control, CopperTech Metals exhibits razor-thin unit economics and severe capital leakage. The transition from an artificially inflated FY2025 net income to a stark FY2026 loss exposes the underlying margin degradation tied to metallurgical dependencies.

Consolidated Segmental & Margin Inventory (FY2025 vs. FY2026)

* Top-Line Velocity: Net Sales increased 234.2% YoY to $1.33 billion, driven by a 173% increase in payable copper sold (278,721 thousand lbs).

* Operating Leverage & Margin Compression: FY2026 Gross Profit stood at just $32.5 million (a 2.4% gross margin), weighed down by $1.30 billion in Cost of Sales. Operating Cash Flow (OCF) remained negative at -$66.3 million.

* Unit Economics (Cost Curve): FY2026 Actual C1 Cash Cost registered at $4.32/lb with an All-In Sustaining Cost (AISC) of $4.71/lb. Management’s target to compress C1 to $2.46/lb relies entirely on economies of scale that require unfunded capital.

* FX & Debt Servicing Leaks: Net foreign exchange losses spiked 330% YoY to $240.8 million due to Kwacha/USD volatility. Finance costs drained an additional $133.2 million, primarily unwinding Scheme of Arrangement liabilities.

* Internal Capital Allocation: Out of the planned $2.7 billion capex (FY2027–2031), exactly $670.0 million from net IPO proceeds is structurally routed to Vedanta Resources Jersey Limited to fund the Konkola Deep Mine Project, leaving a $2.03 billion execution deficit.

* Regulatory & Litigation Provisions: The balance sheet carries a $143.8 million Environmental Protection Fund (EPF) liability (moratorium expires July 2026), alongside active LCIA arbitration exposure of $82.81 million to Trafigura and $29.6 million to the Copperbelt Energy Corporation (CEC).

Physical Supply Chain Audit: The Zambian Moat & Structural Bottlenecks

The operational physicality of CopperTech Metals relies on high-grade reserves but is handicapped by degraded sovereign infrastructure and localized processing constraints.

* Extraction & Hydrological Frictions: The Konkola Complex (measured/indicated at 3.8% TCu) operates at a 1,000-meter depth and requires an extreme 1:49 ore hoist-to-water pumping ratio. A $1.2 billion capital injection is required to install a 1,390-meter level pump station, mitigating the risk of catastrophic mine flooding.

* Metallurgical Blending Dependency: The native ores are excessively high in silica and magnesia. To maintain furnace stability, the Nchanga Smelter (currently operating at 41% of its 312 Ktpa capacity) is forced to import approximately 300 Ktpa of lower-margin third-party chalcopyrite concentrate via the heavily congested Kasumbalesa border with the DRC.

* Chemical & Energy Vulnerabilities: Downstream recovery at the 18.0 Mtpa Tailings Leach Plant (TLP) relies on sulfuric acid produced from pyrite sourced 400 km away at the Nampundwe mine. Furthermore, drought-induced load shedding by state utility ZESCO creates systemic power deficits, single-handedly bottlenecking the Nkana Refinery to a mere 6% utilization rate.

* The Geo-Economic Pivot (Lobito Corridor): Currently dependent on degraded road networks to Durban and Dar es Salaam, CopperTech Metals signed a strategic MoU with the Africa Finance Corporation. By 2029, this secures 180 Ktpa of rail freight capacity on the U.S.-backed Zambia Lobito Railway (ZLR), bypassing Eastern and Southern African logistics chokepoints and providing direct Atlantic access to U.S. markets exempt from Section 232 tariffs.

HDIN Institutional Perspective

While the filing models a 45-year mine life, our forensic analysis reveals that 59% of the resources backing this projection are strictly 'Inferred'—a geologically speculative category lacking demonstrated economic viability. Furthermore, the Street is mispricing the structural capital trap inherent in the "Konkola Waterfall." Even if the $670 million IPO injection successfully deepens Shaft 4, the resulting cash flows are legally subordinated to legacy Zambian vendor payables and Vedanta parent-company scheme loans.

Coupled with a $448.9 million sovereign VAT receivable that management admits is functionally illiquid, internal cash conversion is paralyzed. The governance architecture—featuring an NYSE "controlled company" exemption and an anomalous, immediate-vesting $1,000,000 IPO equity award for the Vice Chairperson—signals a platform designed for parent-company debt offloading rather than minority shareholder yield generation.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Power the Copper Century: CopperTech Metals Inc Strategic lPO Analysis

Segmental Margins & Capital Structure VulnerabilitiesDespite top-line expansion driven by the resumption of operational control, CopperTech Metals exhibits razor-thin unit economics and severe capital leakage. The transition from an artificially inflated FY2025 net income to a stark FY2026 loss exposes the underlying margin degradation tied to metallurgical dependencies.

Consolidated Segmental & Margin Inventory (FY2025 vs. FY2026)

* Top-Line Velocity: Net Sales increased 234.2% YoY to $1.33 billion, driven by a 173% increase in payable copper sold (278,721 thousand lbs).

* Operating Leverage & Margin Compression: FY2026 Gross Profit stood at just $32.5 million (a 2.4% gross margin), weighed down by $1.30 billion in Cost of Sales. Operating Cash Flow (OCF) remained negative at -$66.3 million.

* Unit Economics (Cost Curve): FY2026 Actual C1 Cash Cost registered at $4.32/lb with an All-In Sustaining Cost (AISC) of $4.71/lb. Management’s target to compress C1 to $2.46/lb relies entirely on economies of scale that require unfunded capital.

* FX & Debt Servicing Leaks: Net foreign exchange losses spiked 330% YoY to $240.8 million due to Kwacha/USD volatility. Finance costs drained an additional $133.2 million, primarily unwinding Scheme of Arrangement liabilities.

* Internal Capital Allocation: Out of the planned $2.7 billion capex (FY2027–2031), exactly $670.0 million from net IPO proceeds is structurally routed to Vedanta Resources Jersey Limited to fund the Konkola Deep Mine Project, leaving a $2.03 billion execution deficit.

* Regulatory & Litigation Provisions: The balance sheet carries a $143.8 million Environmental Protection Fund (EPF) liability (moratorium expires July 2026), alongside active LCIA arbitration exposure of $82.81 million to Trafigura and $29.6 million to the Copperbelt Energy Corporation (CEC).

Physical Supply Chain Audit: The Zambian Moat & Structural Bottlenecks

The operational physicality of CopperTech Metals relies on high-grade reserves but is handicapped by degraded sovereign infrastructure and localized processing constraints.

* Extraction & Hydrological Frictions: The Konkola Complex (measured/indicated at 3.8% TCu) operates at a 1,000-meter depth and requires an extreme 1:49 ore hoist-to-water pumping ratio. A $1.2 billion capital injection is required to install a 1,390-meter level pump station, mitigating the risk of catastrophic mine flooding.

* Metallurgical Blending Dependency: The native ores are excessively high in silica and magnesia. To maintain furnace stability, the Nchanga Smelter (currently operating at 41% of its 312 Ktpa capacity) is forced to import approximately 300 Ktpa of lower-margin third-party chalcopyrite concentrate via the heavily congested Kasumbalesa border with the DRC.

* Chemical & Energy Vulnerabilities: Downstream recovery at the 18.0 Mtpa Tailings Leach Plant (TLP) relies on sulfuric acid produced from pyrite sourced 400 km away at the Nampundwe mine. Furthermore, drought-induced load shedding by state utility ZESCO creates systemic power deficits, single-handedly bottlenecking the Nkana Refinery to a mere 6% utilization rate.

* The Geo-Economic Pivot (Lobito Corridor): Currently dependent on degraded road networks to Durban and Dar es Salaam, CopperTech Metals signed a strategic MoU with the Africa Finance Corporation. By 2029, this secures 180 Ktpa of rail freight capacity on the U.S.-backed Zambia Lobito Railway (ZLR), bypassing Eastern and Southern African logistics chokepoints and providing direct Atlantic access to U.S. markets exempt from Section 232 tariffs.

HDIN Institutional Perspective

While the filing models a 45-year mine life, our forensic analysis reveals that 59% of the resources backing this projection are strictly 'Inferred'—a geologically speculative category lacking demonstrated economic viability. Furthermore, the Street is mispricing the structural capital trap inherent in the "Konkola Waterfall." Even if the $670 million IPO injection successfully deepens Shaft 4, the resulting cash flows are legally subordinated to legacy Zambian vendor payables and Vedanta parent-company scheme loans.

Coupled with a $448.9 million sovereign VAT receivable that management admits is functionally illiquid, internal cash conversion is paralyzed. The governance architecture—featuring an NYSE "controlled company" exemption and an anomalous, immediate-vesting $1,000,000 IPO equity award for the Vice Chairperson—signals a platform designed for parent-company debt offloading rather than minority shareholder yield generation.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."