Tata Steel: Aggressive Green Capital Allocation Near Port Talbot and Kalinganagar as 243% Net Profit Surge Signals Margin Insulation Against Chinese Overcapacity

Date : 2026-06-06

Reading : 103

While Tata Steel’s $1.25 billion profit expansion signals robust Indian operational leverage, the real story lies in its geographic divergence. The zero liquid steel output at Port Talbot and the €22 million environmental penalty provision at IJmuiden expose the acute frictional costs of European decarbonization. For institutional LPs, the $2.30 billion FY2027 CapEx ring-fenced primarily for Indian organic growth confirms a deliberate structural pivot: leveraging India's bottom-quartile cost curve to cross-subsidize Europe's capital-intensive, state-backed transition amid EU CBAM regulatory tightening and Red Sea logistical choke points.

Figure Tata Steel FY2025 Strategic Performance & Low-Carbon Transition Blueprint

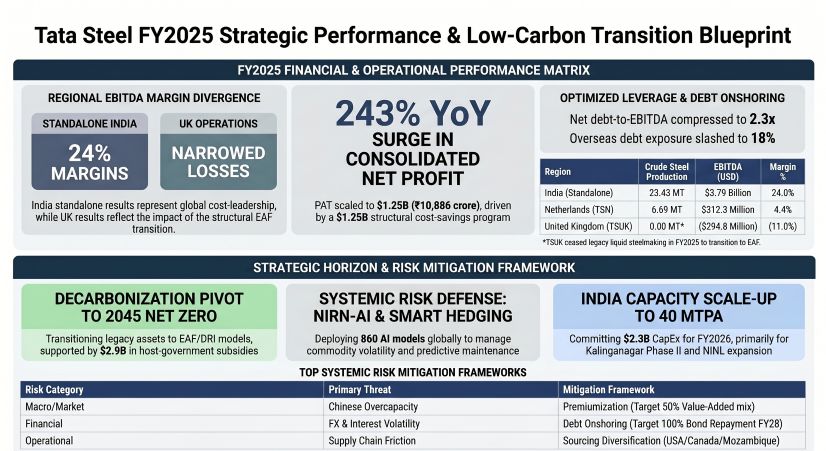

Operating Leverage and Geographic Margin Divergence

Operating Leverage and Geographic Margin Divergence

The NSE: TATASTEEL consolidated financial anatomy reveals a bifurcated margin profile, strictly driven by localized raw material autonomy and asymmetrical regulatory environments.

* Global Topline & Margin Expansion: Consolidated revenue reached $26.64 billion (+6% YoY) on total crude steel production of 31.67 MT. EBITDA surged 35% to $4.00 billion, expanding margins by 320 bps to 15.01%, structurally supported by a $1.25 billion internal cost-transformation program.

* India (The Cash Engine): The domestic segment operates at an elite 24% EBITDA margin, generating $3.79 billion in standalone EBITDA. By moving 22.53 MT of deliveries—where 41% was captured by high-margin B2C/SME platforms like Tata Tiscon and Tata Steelium—India remains the primary capital generator for the global group.

* The European Transitional Void: The United Kingdom posted an EBITDA loss of -$294.8 million. Due to the complete closure of primary blast furnaces at Port Talbot, liquid steel production flatlined at 0.00 MT, forcing total reliance on 2.21 MT of processed downstream deliveries. Conversely, the Netherlands (IJmuiden) tripled its EBITDA to $312.3 million on 6.69 MT of liquid steel, despite heavy regulatory headwinds.

* Deleveraging & FX Shielding: The Net Debt-to-EBITDA ratio compressed to an investment-grade 2.3x ($9.20 billion net debt). By aggressively onshoring debt—reducing overseas currency exposure from 50% in FY21 to 18% in FY26—management bypassed an estimated $1.43 billion in translation depreciation impacts.

* Working Capital Extraction: Inventory turnover was squeezed from 80 to 73 days, and Days Sales Outstanding (DSO) maintained an elite 8-day profile. Concurrently, Days Payable Outstanding (DPO) was stretched to 87 days via aggressive 180-day supplier financing, successfully extracting a $624 million direct cash release.

Physical Asset Audit and Geo-Economic Moat Vulnerabilities

Tata Steel's physicality is currently dictated by extreme supply chain realignment and massive state-subsidized asset restructuring.

* Upstream Autonomy vs. Import Reliance: Indian operations are anchored by 100% captive iron ore integration (43.5 MT sourced from the Noamundi and Joda East mines). However, the enterprise imports ~80% of its coking coal. Middle Eastern geopolitical friction has injected 10-14 days of maritime delay into Asia-Europe lanes. To mitigate this, procurement has structurally pivoted away from Australia toward Tier-1 nodes in the USA, Canada, Mozambique, and Indonesia, utilizing alternative routing via the Salalah and Dibba ports.

* European EAF Subsidization: The UK’s $1.65 billion (£1.25 billion) transition to a 3.2 MTPA Electric Arc Furnace (EAF) is fundamentally tethered to a $659.6 million (£500 million) Grant Funding Agreement. Without this, auditors indicate material uncertainty regarding the UK entity's going concern status. Similarly, the Netherlands division is positioning for a $2.26 billion (€2 billion) state-subsidized Direct Reduced Iron (DRI) pivot to abandon legacy carbon-intensive infrastructure.

* Regulatory Friction: Operations at IJmuiden are actively constrained by local environmental agencies. The firm recognized a $24.87 million (€22 million) provision against a total $30.53 million exposure for legacy Coke and Gas Plant emissions, with an additional $11.31 million (€10 million) penalty risk lingering over LD steel slag classifications.

HDIN Institutional Perspective

While management attributes European EBITDA compression to the "green transition phase," the forensic reality reveals an enterprise fundamentally reliant on host-nation sovereign subsidies to maintain solvency in the UK and the EU. The $1.25 billion in structural cost savings and the elite 24% EBITDA margin in India are effectively serving as a financial bridge to cover European regulatory penalties and $114.09 million in redundancy provisions. Institutional investors must price NSE: TATASTEEL not as a unified global steelmaker, but as a highly lucrative, backward-integrated Indian monopoly temporarily burdened by a European distressed-asset restructuring play. With $2.30 billion in FY2027 CapEx overwhelmingly routed to domestic facilities like the Kalinganagar Phase II and Ludhiana EAF, the long-term ROI overwhelmingly favors the Indian macro-infrastructure narrative.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Tata Steel FY2025 Strategic Performance & Low-Carbon Transition Blueprint

Operating Leverage and Geographic Margin DivergenceThe NSE: TATASTEEL consolidated financial anatomy reveals a bifurcated margin profile, strictly driven by localized raw material autonomy and asymmetrical regulatory environments.

* Global Topline & Margin Expansion: Consolidated revenue reached $26.64 billion (+6% YoY) on total crude steel production of 31.67 MT. EBITDA surged 35% to $4.00 billion, expanding margins by 320 bps to 15.01%, structurally supported by a $1.25 billion internal cost-transformation program.

* India (The Cash Engine): The domestic segment operates at an elite 24% EBITDA margin, generating $3.79 billion in standalone EBITDA. By moving 22.53 MT of deliveries—where 41% was captured by high-margin B2C/SME platforms like Tata Tiscon and Tata Steelium—India remains the primary capital generator for the global group.

* The European Transitional Void: The United Kingdom posted an EBITDA loss of -$294.8 million. Due to the complete closure of primary blast furnaces at Port Talbot, liquid steel production flatlined at 0.00 MT, forcing total reliance on 2.21 MT of processed downstream deliveries. Conversely, the Netherlands (IJmuiden) tripled its EBITDA to $312.3 million on 6.69 MT of liquid steel, despite heavy regulatory headwinds.

* Deleveraging & FX Shielding: The Net Debt-to-EBITDA ratio compressed to an investment-grade 2.3x ($9.20 billion net debt). By aggressively onshoring debt—reducing overseas currency exposure from 50% in FY21 to 18% in FY26—management bypassed an estimated $1.43 billion in translation depreciation impacts.

* Working Capital Extraction: Inventory turnover was squeezed from 80 to 73 days, and Days Sales Outstanding (DSO) maintained an elite 8-day profile. Concurrently, Days Payable Outstanding (DPO) was stretched to 87 days via aggressive 180-day supplier financing, successfully extracting a $624 million direct cash release.

Physical Asset Audit and Geo-Economic Moat Vulnerabilities

Tata Steel's physicality is currently dictated by extreme supply chain realignment and massive state-subsidized asset restructuring.

* Upstream Autonomy vs. Import Reliance: Indian operations are anchored by 100% captive iron ore integration (43.5 MT sourced from the Noamundi and Joda East mines). However, the enterprise imports ~80% of its coking coal. Middle Eastern geopolitical friction has injected 10-14 days of maritime delay into Asia-Europe lanes. To mitigate this, procurement has structurally pivoted away from Australia toward Tier-1 nodes in the USA, Canada, Mozambique, and Indonesia, utilizing alternative routing via the Salalah and Dibba ports.

* European EAF Subsidization: The UK’s $1.65 billion (£1.25 billion) transition to a 3.2 MTPA Electric Arc Furnace (EAF) is fundamentally tethered to a $659.6 million (£500 million) Grant Funding Agreement. Without this, auditors indicate material uncertainty regarding the UK entity's going concern status. Similarly, the Netherlands division is positioning for a $2.26 billion (€2 billion) state-subsidized Direct Reduced Iron (DRI) pivot to abandon legacy carbon-intensive infrastructure.

* Regulatory Friction: Operations at IJmuiden are actively constrained by local environmental agencies. The firm recognized a $24.87 million (€22 million) provision against a total $30.53 million exposure for legacy Coke and Gas Plant emissions, with an additional $11.31 million (€10 million) penalty risk lingering over LD steel slag classifications.

HDIN Institutional Perspective

While management attributes European EBITDA compression to the "green transition phase," the forensic reality reveals an enterprise fundamentally reliant on host-nation sovereign subsidies to maintain solvency in the UK and the EU. The $1.25 billion in structural cost savings and the elite 24% EBITDA margin in India are effectively serving as a financial bridge to cover European regulatory penalties and $114.09 million in redundancy provisions. Institutional investors must price NSE: TATASTEEL not as a unified global steelmaker, but as a highly lucrative, backward-integrated Indian monopoly temporarily burdened by a European distressed-asset restructuring play. With $2.30 billion in FY2027 CapEx overwhelmingly routed to domestic facilities like the Kalinganagar Phase II and Ludhiana EAF, the long-term ROI overwhelmingly favors the Indian macro-infrastructure narrative.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."