Lifemotion: Strategic Pivot Near Shenzhen Bao'an Headquarters as 163.89% Consumables Volume Growth Signals Transition to Razor-and-Blades Unit Economics

Date : 2026-06-06

Reading : 92

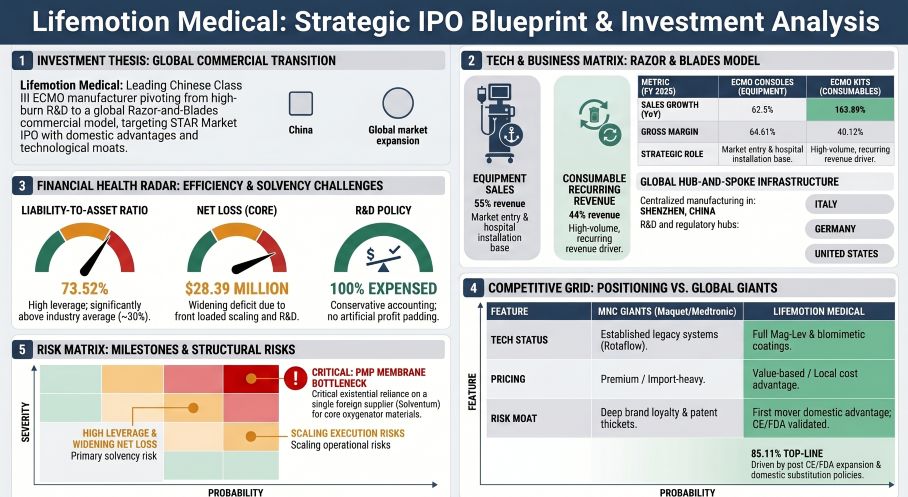

Lifemotion's S-1 filing reveals a textbook transition from R&D-heavy capital equipment sales to a recurring high-margin consumables model. Despite an 85.11% YoY revenue surge to USD 12.83 million in 2025, structural unprofitability persists, highlighted by a severe USD 19.86 million operating cash burn. For institutional LPs, the critical friction point isn’t domestic hospital demand—which is artificially buoyed by localized procurement mandates—but an existential supply chain bottleneck. Complete reliance on a single German supplier for critical polymethylpentene membranes threatens to derail its 2028 break-even trajectory amid intensifying geopolitical trade fragmentation.

Figure Lifemotion Medical: Strategic lPO Blueprint & Investment Analysis

Operating Leverage & Unit Economics Dislocation

Operating Leverage & Unit Economics Dislocation

Lifemotion’s financial architecture exposes the massive capital intensity required for Class III Extracorporeal Membrane Oxygenation (ECMO) commercialization. Internal capital allocation strictly prioritizes the scaling of consumables to capture recurring revenue.

* Top-Line & Price-Mix Variance: Total revenue scaled to USD 12.83M in 2025 (85.11% YoY). This was driven by a product mix shift; ECMO Consumable Kits surged to 44.59% of core revenue (USD 5.70M), representing a 163.89% YoY sales volume jump to 2,974 units. Capital equipment (ECMO Consoles) fell to 55.41% of revenue (USD 7.08M) on 130 units sold.

* Margin Dislocation: Consolidated gross margins expanded from 33.37% (2023) to 53.76% (2025). Counterintuitively, the "razor" (ECMO Consoles) yields a higher gross margin (64.61%) than the "blades" (ECMO Consumables at 40.12%), confirming the consumables manufacturing base has not yet breached optimal scale to dilute the cost of imported raw materials.

* FCF Conversion & Liquidity Drain: Operating Cash Flow (OCF) plummeted to USD -19.86M in 2025. The company carries a massive unrecovered deficit of USD 87.68M. Return on Equity (ROE) remains heavily distressed at -144.70%.

* Leverage & Capital Structure: To bridge the gap to a projected 2028 break-even, long-term debt spiked from USD 4.16M (2024) to USD 23.71M (2025), driving the liability-to-asset ratio to an elevated 73.52%. However, short-term liquidity remains adequately covered with a Current Ratio of 2.36.

* R&D-to-Moat Translation: R&D expenditure—strictly expensed at 100% (USD 14.97M in 2025)—funded proprietary Biomimetic Phosphorylcholine Coating developments, clinically validated by a 37-subject trial achieving a 91.43% 7-day survival rate and a subsequent 158-patient real-world study achieving a 77.2% 24-hour weaning survival rate.

Geo-Economic Moat & Supply Chain Architecture: The Physical Bottleneck

The company operates a decentralized global regulatory footprint anchored by a structurally vulnerable manufacturing core.

* Global Footprint & Regulatory Hubs: Operations span a 33,000 sq.m manufacturing footprint at the Shenzhen Bao'an District Headquarters, supported by the Mirandola, Italy (Lifemotion S.r.l.) R&D center, and a regulatory hub in Los Angeles, USA. This tri-node structure secured the January 2025 CE MDR certification and the critical March 2026 FDA clearance for oxygenators.

* Critical Upstream Chokepoint: Lifemotion exhibits extreme supplier concentration risk. Procurement of Polymethlypentene (PMP) membranes—the core component of the oxygenator—relies 100% on a single entity: Solventum Germany GmbH (formerly 3M). In 2025, this accounted for 19.47% of total procurement (USD 1.36M).

* CapEx Realignment: The USD 140.18M IPO target aggressively addresses capacity constraints. USD 27.92M (19.92%) is earmarked for a 36-month automated manufacturing base build-out, while USD 69.97M (49.91%) targets a 6-year R&D pipeline, and USD 34.78M bridges working capital deficits.

* Asset & Title Anomalies: Domestically, 15 out of 17 leased properties lack formal real estate registration, and 8 specific facilities (including specific underground units at the Bao'an Headquarters) lack formal ownership certificates, though direct disruption risk to the primary manufacturing line remains minimal. Furthermore, the indirect 0.6140% stake held by the Board Secretary via the Hannuo Partnership platform is currently under judicial freeze.

HDIN Institutional Perspective: The VAM Revival Threat

While the Street views Lifemotion's 99.04% distributor-led channel and highly favorable "payment-before-delivery" working capital cycle (driving AR turnover down to 29.94) as a defensive cash-flow moat, we maintain a differentiated viewpoint on its equity stability. The market has mispriced the latent execution risk embedded in the company's Valuation Adjustment Mechanism (VAM). Although these special shareholder rights were conditionally suspended prior to the IPO, a strict revival clause remains active. Should the company fail to submit its A-share application by December 31, 2025, or fail to secure exchange acceptance by February 28, 2026, draconian redemption rights will retroactively trigger against the founders. Combined with a 73.52% leverage ratio and deep operational unprofitability, any regulatory delay in the 36-month CAPEX deployment could catalyze an immediate liquidity crisis at the controlling shareholder level.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Lifemotion Medical: Strategic lPO Blueprint & Investment Analysis

Operating Leverage & Unit Economics DislocationLifemotion’s financial architecture exposes the massive capital intensity required for Class III Extracorporeal Membrane Oxygenation (ECMO) commercialization. Internal capital allocation strictly prioritizes the scaling of consumables to capture recurring revenue.

* Top-Line & Price-Mix Variance: Total revenue scaled to USD 12.83M in 2025 (85.11% YoY). This was driven by a product mix shift; ECMO Consumable Kits surged to 44.59% of core revenue (USD 5.70M), representing a 163.89% YoY sales volume jump to 2,974 units. Capital equipment (ECMO Consoles) fell to 55.41% of revenue (USD 7.08M) on 130 units sold.

* Margin Dislocation: Consolidated gross margins expanded from 33.37% (2023) to 53.76% (2025). Counterintuitively, the "razor" (ECMO Consoles) yields a higher gross margin (64.61%) than the "blades" (ECMO Consumables at 40.12%), confirming the consumables manufacturing base has not yet breached optimal scale to dilute the cost of imported raw materials.

* FCF Conversion & Liquidity Drain: Operating Cash Flow (OCF) plummeted to USD -19.86M in 2025. The company carries a massive unrecovered deficit of USD 87.68M. Return on Equity (ROE) remains heavily distressed at -144.70%.

* Leverage & Capital Structure: To bridge the gap to a projected 2028 break-even, long-term debt spiked from USD 4.16M (2024) to USD 23.71M (2025), driving the liability-to-asset ratio to an elevated 73.52%. However, short-term liquidity remains adequately covered with a Current Ratio of 2.36.

* R&D-to-Moat Translation: R&D expenditure—strictly expensed at 100% (USD 14.97M in 2025)—funded proprietary Biomimetic Phosphorylcholine Coating developments, clinically validated by a 37-subject trial achieving a 91.43% 7-day survival rate and a subsequent 158-patient real-world study achieving a 77.2% 24-hour weaning survival rate.

Geo-Economic Moat & Supply Chain Architecture: The Physical Bottleneck

The company operates a decentralized global regulatory footprint anchored by a structurally vulnerable manufacturing core.

* Global Footprint & Regulatory Hubs: Operations span a 33,000 sq.m manufacturing footprint at the Shenzhen Bao'an District Headquarters, supported by the Mirandola, Italy (Lifemotion S.r.l.) R&D center, and a regulatory hub in Los Angeles, USA. This tri-node structure secured the January 2025 CE MDR certification and the critical March 2026 FDA clearance for oxygenators.

* Critical Upstream Chokepoint: Lifemotion exhibits extreme supplier concentration risk. Procurement of Polymethlypentene (PMP) membranes—the core component of the oxygenator—relies 100% on a single entity: Solventum Germany GmbH (formerly 3M). In 2025, this accounted for 19.47% of total procurement (USD 1.36M).

* CapEx Realignment: The USD 140.18M IPO target aggressively addresses capacity constraints. USD 27.92M (19.92%) is earmarked for a 36-month automated manufacturing base build-out, while USD 69.97M (49.91%) targets a 6-year R&D pipeline, and USD 34.78M bridges working capital deficits.

* Asset & Title Anomalies: Domestically, 15 out of 17 leased properties lack formal real estate registration, and 8 specific facilities (including specific underground units at the Bao'an Headquarters) lack formal ownership certificates, though direct disruption risk to the primary manufacturing line remains minimal. Furthermore, the indirect 0.6140% stake held by the Board Secretary via the Hannuo Partnership platform is currently under judicial freeze.

HDIN Institutional Perspective: The VAM Revival Threat

While the Street views Lifemotion's 99.04% distributor-led channel and highly favorable "payment-before-delivery" working capital cycle (driving AR turnover down to 29.94) as a defensive cash-flow moat, we maintain a differentiated viewpoint on its equity stability. The market has mispriced the latent execution risk embedded in the company's Valuation Adjustment Mechanism (VAM). Although these special shareholder rights were conditionally suspended prior to the IPO, a strict revival clause remains active. Should the company fail to submit its A-share application by December 31, 2025, or fail to secure exchange acceptance by February 28, 2026, draconian redemption rights will retroactively trigger against the founders. Combined with a 73.52% leverage ratio and deep operational unprofitability, any regulatory delay in the 36-month CAPEX deployment could catalyze an immediate liquidity crisis at the controlling shareholder level.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."