Wiwynn Corporation: Capacity Decentralization Near Texas and Tainan as a 163.7% Revenue Surge Signals Extreme Working Capital Stress

Date : 2026-06-06

Reading : 136

Wiwynn’s 2025 filings reveal an aggressive ODM-Direct scale-up to meet hyperscale AI compute demand, driving a 163.7% revenue explosion to $30.50 billion. However, this hyper-growth masks a structural working capital drag. The Board’s discrete reclassification of highly aged accounts receivable into "non-fund lending" exposes the delayed capex payment cycles of top-tier cloud providers. For institutional LPs, Wiwynn’s 0.00% equity dilution and 100% cash profit-sharing represent a masterclass in shareholder protection, but negative free cash flow conversion remains the absolute friction point as global capacity rolls out.

Figure Wiwynn 2025 Strategic Performance: Leading the Al infrastructure Frontier

Forensic Financials & Segmental Inventory

Forensic Financials & Segmental Inventory

While the top line validates Wiwynn (TWSE: 6669) as an apex infrastructure architect for the AI era, an audit of the underlying unit economics reveals severe price-mix variance and heavy capital commitments masked by off-balance-sheet leasing.

Quantitative Inventory & Capital Allocation Matrix (FY2025)

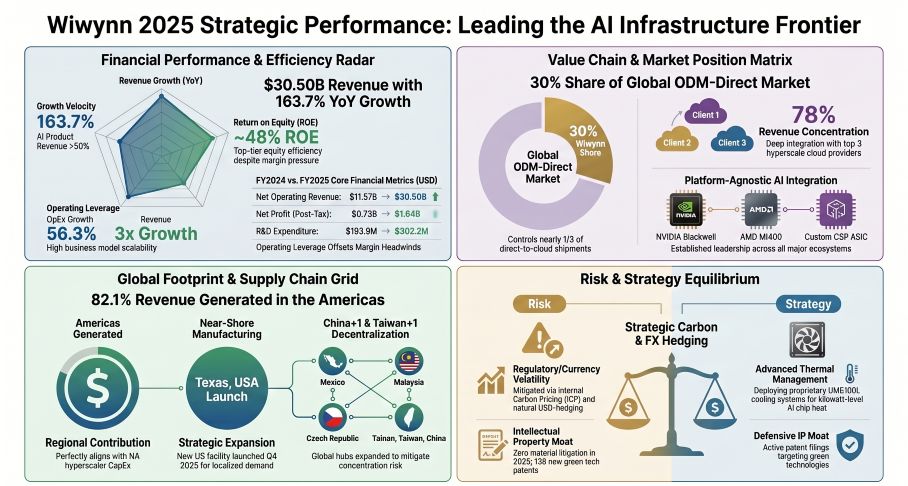

* Revenue & Operational Leverage: Net revenue hit $30.50 billion (+163.7% YoY). Operating expenses grew at merely 56.3% ($466.4 million), allowing absolute net profit to surge 124.4% to $1.64 billion.

* Margin Compression & Unit Economics: Gross Profit Margin (GPM) compressed from 10.4% in 2024 to 8.3%, reflecting the cost-heavy integration of advanced silicon from NASDAQ: NVDA and NASDAQ: AMD. Operating Margin settled at 6.7%, and Net Profit Margin at 5.4%.

* Treasury & Non-Operating Income: Exceptional earnings quality; non-operating income ($68.50 million) constitutes just 4.1% of net profit, driven entirely by $124.90 million in FX gains on USD-denominated flows, with zero reliance on government subsidies.

* R&D-to-Moat Translation: Absolute R&D surged 55.8% to $302.18 million. Despite the R&D-to-revenue ratio diluting to 0.99%, this capital funded proprietary UMS100L liquid cooling systems, Double-Wide AI Racks, and "Super Fluid" technology co-developed with NASDAQ: INTC.

* Free Cash Flow Conversion & CapEx: OCF improved to negative $20.0 million (from -$641.5 million), but CapEx exploded 217.6% to $371.2 million, resulting in an FCF bleed of -$391.2 million.

The Receivables Risk: Current assets bloated by 76.8% to $9.85 billion. Crucially, the Board formalized the reclassification of "material" accounts receivable aging past 90 days as "non-fund-lending." With Clients N, L, and A representing 41.48%, 26.03%, and 10.43% of revenue respectively, this accounting pivot suggests hyperscalers are stretching payables, shifting the structural cost of AI capex onto Wiwynn’s balance sheet.

Supply Chain Audit & Geo-Economic Moat

Wiwynn is aggressively physically decoupling from centralized manufacturing to insulate its hyperscale clientele from geopolitical friction. The company’s geographic footprint and human capital logistics illustrate a "Taiwan+1" physicality built to absorb localized shocks.

* Manufacturing Physicality & CapEx Realignment: In 2025, Wiwynn finalized its North American near-shoring strategy by launching production at its new Texas facility, complementing massive operations in Mexico. Additional hubs in Malaysia, the Czech Republic, and the Tainan Science Park Phase III (Taiwan, China) form the core of its L10/L11 rack-level delivery pipeline.

* Real Estate & Lease Liabilities: Rather than purchasing land, Wiwynn utilizes "Right-of-Use" land leases for its new Neihu Tanmei headquarters (Taipei) and Tainan expansions, inflating right-of-use assets by 32.3% to $325.19 million—locking the firm into rigid, long-term lease liabilities.

* Tier-1 Procurement Physics: Sourcing is heavily customer-directed. "Supplier F" alone controls 33.34% ($9.79 billion) of total procurement. To buffer capacity, Wiwynn outsourced $2.38 billion (8.09% of purchases) to its parent entity, Wistron Corporation (TWSE: 3231).

* Human Capital Expansion & Dilution Armor: Global headcount scaled 49.4% to 15,891 (12,460 direct labor; 2,498 R&D; 810 Ops; 123 Sales). The 45.9% degreed workforce saw average tenure drop to 2.41 years due to hyper-expansion. Management executed a 100% cash-based profit-sharing pool of $112.3 million (5.18% of pre-tax profit), issuing zero ESOPs or RSUs in 2025 to block shareholder dilution. (Note: The Board approved a 2026 RSU reintroduction on February 26, 2026). Retention is fortified by a ~$1,925 childbirth subsidy and $70/capita (34 hours) training investments.

* Regulatory & ESG Moat: The firm achieved an 80.09% renewable energy baseline and filed 138 new patents (102 green). It suffered an immaterial $4,813 in subsidiary-level labor/safety fines. Anticipating the EU’s Carbon Border Adjustment Mechanism (CBAM), Wiwynn proactively embedded an Internal Carbon Pricing (ICP) mechanism into its capital allocation models.

HDIN Institutional Perspective

Challenge: While the Street fixates on Wiwynn's impressive ~48.0% Return on Equity (ROE) and its dominance in the NVIDIA GB300 NVL72 cycle, the underlying balance sheet mechanics reveal a highly cash-consumptive profile. The ODM-Direct model forces Wiwynn to act as the primary shock absorber for the AI hardware cycle. The Q1/Q2 2025 Board resolutions reclassifying late-stage receivables indicate that cloud service providers are weaponizing their purchasing scale, squeezing Wiwynn’s working capital velocity.

Confirm: Wiwynn’s execution of its strategic decentralization is flawless. Bypassing traditional OEM intermediaries allows Wiwynn to capture a near 30% ODM-Direct market share. Their proactive deployment of Internal Carbon Pricing against CBAM, zero reliance on policy-driven government subsidies, and ruthless protection of equity via $112.3 million in cash-only bonuses demonstrate an elite, defensively engineered corporate governance framework. As long as external debt markets remain liquid to fund the -$391.2 million FCF gap, Wiwynn's engineering moats in 800V HVDC power architectures and Direct Liquid Cooling render them practically irreplaceable to North American hyperscalers.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Wiwynn 2025 Strategic Performance: Leading the Al infrastructure Frontier

Forensic Financials & Segmental InventoryWhile the top line validates Wiwynn (TWSE: 6669) as an apex infrastructure architect for the AI era, an audit of the underlying unit economics reveals severe price-mix variance and heavy capital commitments masked by off-balance-sheet leasing.

Quantitative Inventory & Capital Allocation Matrix (FY2025)

* Revenue & Operational Leverage: Net revenue hit $30.50 billion (+163.7% YoY). Operating expenses grew at merely 56.3% ($466.4 million), allowing absolute net profit to surge 124.4% to $1.64 billion.

* Margin Compression & Unit Economics: Gross Profit Margin (GPM) compressed from 10.4% in 2024 to 8.3%, reflecting the cost-heavy integration of advanced silicon from NASDAQ: NVDA and NASDAQ: AMD. Operating Margin settled at 6.7%, and Net Profit Margin at 5.4%.

* Treasury & Non-Operating Income: Exceptional earnings quality; non-operating income ($68.50 million) constitutes just 4.1% of net profit, driven entirely by $124.90 million in FX gains on USD-denominated flows, with zero reliance on government subsidies.

* R&D-to-Moat Translation: Absolute R&D surged 55.8% to $302.18 million. Despite the R&D-to-revenue ratio diluting to 0.99%, this capital funded proprietary UMS100L liquid cooling systems, Double-Wide AI Racks, and "Super Fluid" technology co-developed with NASDAQ: INTC.

* Free Cash Flow Conversion & CapEx: OCF improved to negative $20.0 million (from -$641.5 million), but CapEx exploded 217.6% to $371.2 million, resulting in an FCF bleed of -$391.2 million.

The Receivables Risk: Current assets bloated by 76.8% to $9.85 billion. Crucially, the Board formalized the reclassification of "material" accounts receivable aging past 90 days as "non-fund-lending." With Clients N, L, and A representing 41.48%, 26.03%, and 10.43% of revenue respectively, this accounting pivot suggests hyperscalers are stretching payables, shifting the structural cost of AI capex onto Wiwynn’s balance sheet.

Supply Chain Audit & Geo-Economic Moat

Wiwynn is aggressively physically decoupling from centralized manufacturing to insulate its hyperscale clientele from geopolitical friction. The company’s geographic footprint and human capital logistics illustrate a "Taiwan+1" physicality built to absorb localized shocks.

* Manufacturing Physicality & CapEx Realignment: In 2025, Wiwynn finalized its North American near-shoring strategy by launching production at its new Texas facility, complementing massive operations in Mexico. Additional hubs in Malaysia, the Czech Republic, and the Tainan Science Park Phase III (Taiwan, China) form the core of its L10/L11 rack-level delivery pipeline.

* Real Estate & Lease Liabilities: Rather than purchasing land, Wiwynn utilizes "Right-of-Use" land leases for its new Neihu Tanmei headquarters (Taipei) and Tainan expansions, inflating right-of-use assets by 32.3% to $325.19 million—locking the firm into rigid, long-term lease liabilities.

* Tier-1 Procurement Physics: Sourcing is heavily customer-directed. "Supplier F" alone controls 33.34% ($9.79 billion) of total procurement. To buffer capacity, Wiwynn outsourced $2.38 billion (8.09% of purchases) to its parent entity, Wistron Corporation (TWSE: 3231).

* Human Capital Expansion & Dilution Armor: Global headcount scaled 49.4% to 15,891 (12,460 direct labor; 2,498 R&D; 810 Ops; 123 Sales). The 45.9% degreed workforce saw average tenure drop to 2.41 years due to hyper-expansion. Management executed a 100% cash-based profit-sharing pool of $112.3 million (5.18% of pre-tax profit), issuing zero ESOPs or RSUs in 2025 to block shareholder dilution. (Note: The Board approved a 2026 RSU reintroduction on February 26, 2026). Retention is fortified by a ~$1,925 childbirth subsidy and $70/capita (34 hours) training investments.

* Regulatory & ESG Moat: The firm achieved an 80.09% renewable energy baseline and filed 138 new patents (102 green). It suffered an immaterial $4,813 in subsidiary-level labor/safety fines. Anticipating the EU’s Carbon Border Adjustment Mechanism (CBAM), Wiwynn proactively embedded an Internal Carbon Pricing (ICP) mechanism into its capital allocation models.

HDIN Institutional Perspective

Challenge: While the Street fixates on Wiwynn's impressive ~48.0% Return on Equity (ROE) and its dominance in the NVIDIA GB300 NVL72 cycle, the underlying balance sheet mechanics reveal a highly cash-consumptive profile. The ODM-Direct model forces Wiwynn to act as the primary shock absorber for the AI hardware cycle. The Q1/Q2 2025 Board resolutions reclassifying late-stage receivables indicate that cloud service providers are weaponizing their purchasing scale, squeezing Wiwynn’s working capital velocity.

Confirm: Wiwynn’s execution of its strategic decentralization is flawless. Bypassing traditional OEM intermediaries allows Wiwynn to capture a near 30% ODM-Direct market share. Their proactive deployment of Internal Carbon Pricing against CBAM, zero reliance on policy-driven government subsidies, and ruthless protection of equity via $112.3 million in cash-only bonuses demonstrate an elite, defensively engineered corporate governance framework. As long as external debt markets remain liquid to fund the -$391.2 million FCF gap, Wiwynn's engineering moats in 800V HVDC power architectures and Direct Liquid Cooling render them practically irreplaceable to North American hyperscalers.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."