Global Nuclear Fuel 2026 Outlook: Why Cameco, Urenco, and Uranium Energy Corp Diverge on Capital Allocation Amid Western Supply Chain Onshoring

Date : 2026-06-06

Reading : 1657

The U.S. Prohibiting Russian Uranium Imports Act has triggered a structural supply deficit, bifurcating the global nuclear fuel market. Tier-1 incumbents like Cameco and enrichment monopolist Urenco are deploying immense free cash flow to alleviate midstream bottlenecks, executing a fortress-balance-sheet approach. Conversely, North American agile extractors like Uranium Energy Corp leverage unhedged spot-market exposure to monetize cyclical peaks, funded entirely by dilutive equity. For institutional LPs, the arbitrage lies in distinguishing organic cash converters insulated by generational off-take agreements from speculative explorers surviving on external liquidity.

Figure 2025 NUCLEAR FUEL LANDSCAPE

Forensic Analysis of Earnings Quality and Segmental Operating Leverage

Forensic Analysis of Earnings Quality and Segmental Operating Leverage

A rigorous forensic audit of the 2025 financial disclosures exposes a stark divide in unit economics, earnings quality, and capital funding mechanisms across the sector.

The Cash Converters & Margin Expansions:

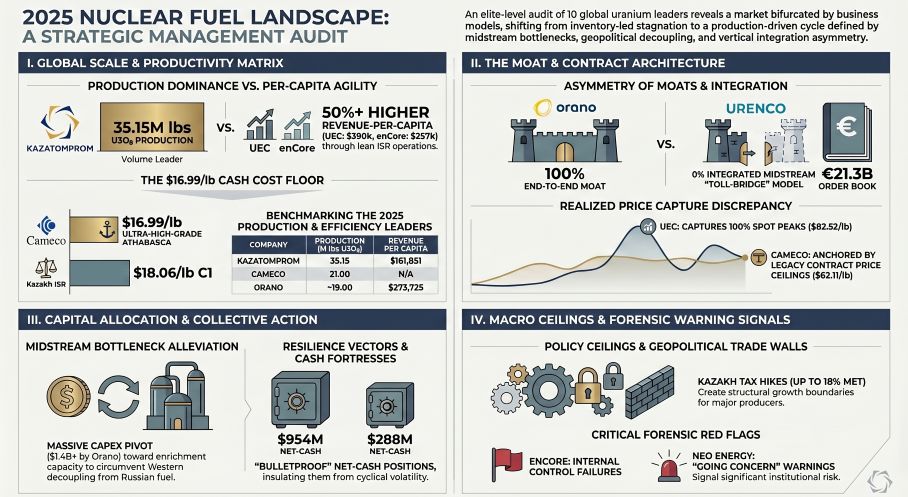

* Cameco (NYSE: CCJ): Exhibits peer-leading operational efficiency at its high-grade Canadian conventional assets. The company reported a C1 cash cost of $16.99/lb against an average realized price of $62.11/lb. Earnings quality is exceptionally robust, translating $422.2M in net income into a massive $1,007.6M in Operating Cash Flow (OCF), yielding $769.3M in self-sustaining Free Cash Flow (FCF) capable of extinguishing $200M in term debt organically.

* Urenco: Operates as a midstream toll-bridge, capturing super-normal geopolitical premiums. The company reported a 38.3% EBITDA margin ($909.0M EBITDA on $2,370.0M revenue). Its 4.2x OCF-to-Net Income conversion ratio easily funds $696.2M in enrichment CapEx while servicing a record $24.08 billion order book extending into the 2040s.

* Kazatomprom (LSE: KAP): Maintains the industry's lowest C1 cost at $18.06/lb, though margins are under assault. Operating leverage is compressing due to a 42.6% explosion in sulfuric acid costs and an aggressive Mineral Extraction Tax (MET) hike to 9% (comprising 36% of C1 costs). Total OCF matched net income at $1,668.3M, perfectly covering its $851.1M CapEx requirements.

* Arbitrage & Spot Market Capture:

* Uranium Energy Corp (NYSE: UEC): Subverts traditional mining efficiency with a 682-day Days Inventory Outstanding (DIO). By deliberately hoarding spot material and entirely avoiding legacy utility price-ceilings, UEC captured a sector-high average realized price of $82.52/lb.

* CGN Mining (HKEX: 1164): Executes an asset-light off-take model (0.79x Asset Turnover). By purchasing from Kazakh joint ventures at a guaranteed 2% spot-discount, the company posted a 204% gross profit explosion despite localized asset degradation pushing C1 costs at its Semizbay mine up to $37.00/lb.

The Cash-Burning Speculators & Forensic Triggers:

* enCore Energy (NASDAQ: EU): Despite pushing an aggressive In-Situ Recovery (ISR) narrative, the entity is bleeding cash (negative $25.0M OCF on a $63.0M net loss) and survives strictly via $110.0M in convertible notes. Crucially, management disclosed material weaknesses in internal controls and acknowledged extracting from assets with zero SEC-compliant S-K 1300 "Mineral Reserves."

* Neo Energy Metals (LSE: NEO): Triggered a critical "Going Concern" warning from independent auditors. The exploration entity reported £19,065 in cash against a £6.1 million operational burn rate, rendering its £3.1 million in subsidiary investments highly susceptible to impairment.

* China National Uranium: Displays a severe accounting discrepancy. Despite reporting $183.8M in net profit, the state-backed entity hemorrhaged -$356.7M in operating cash flows, indicating massive working capital drag or aggressive revenue recognition.

Global Supply Chain Restructuring and Regional Economic Moats

The physicality of the 2025 uranium market is defined by severe jurisdictional risk and aggressive capital redirection toward secure geopolitical corridors.

* Enrichment Monopolies and Midstream Onshoring: Western capital is aggressively flowing into Front-End choke points. Orano is deploying $1,492 million in CapEx, primarily targeting the capacity extension of the Georges Besse II enrichment plant in France and securing $900 million in US Department of Energy (DOE) funding for the IKE project in Oak Ridge, Tennessee. Urenco is expanding the Eunice (New Mexico) facility, alongside European expansions at Almelo and Gronau, effectively commercializing LEU+ capabilities to service hyperscaler AI data center demands.

* Bypassing the Russian Transport Chokepoint: Central Asian producers face acute logistics risks. To circumvent the traditional St. Petersburg export route and avoid Western sanctions, Kazatomprom successfully rerouted 48% of its Western-bound U3O8 shipments through the Trans-Caspian International Transport Route (TITR). Furthermore, producers are executing location-based "swap agreements" at Western conversion facilities like Malvési (France) and Port Hope (Canada) to entirely eliminate transit exposure.

* Jurisdictional Expropriation vs. Tier-1 Technological Fortification: Resource nationalism in emerging markets actively destroyed operator value in 2025, culminating in Orano's loss of operational control at the Somaïr mine in Niger. In stark contrast, North American operators are deploying advanced proprietary technology to reinforce their local moats. Cameco and Orano successfully commercialized the SABRE method at the McClean Lake joint venture in the Athabasca Basin, allowing for non-invasive, surface-borehole extraction of ultra-high-grade deposits without conventional shaft construction. Simultaneously, UEC executed the $175.4 million Sweetwater Acquisition in Wyoming to localize its US-centric ISR hub-and-spoke model.

HDIN Institutional Perspective

While retail momentum blindly rewards North American ISR operators for their geopolitical safety premiums, a forensic analysis reveals a severe disconnect between narrative and earnings quality. The Street continues to price Uranium Energy Corp and enCore Energy as steady-state producers; however, their financial architecture relies on highly dilutive At-The-Market (ATM) equity issuance ($287.5M for UEC) and external debt rather than organic extraction margins. We challenge the prevailing consensus that "domestic jurisdiction" equates to a standalone economic moat. True capital insulation in the 2026-2030 cycle strictly belongs to entities controlling physical midstream bottlenecks (Urenco) or generating self-sustaining, debt-extinguishing free cash flows from ultra-low-cost geology (Cameco, Kazatomprom). Junior explorers currently lack both the balance sheet and the SEC-compliant reserves required to survive localized supply chain disruptions.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure 2025 NUCLEAR FUEL LANDSCAPE

Forensic Analysis of Earnings Quality and Segmental Operating LeverageA rigorous forensic audit of the 2025 financial disclosures exposes a stark divide in unit economics, earnings quality, and capital funding mechanisms across the sector.

The Cash Converters & Margin Expansions:

* Cameco (NYSE: CCJ): Exhibits peer-leading operational efficiency at its high-grade Canadian conventional assets. The company reported a C1 cash cost of $16.99/lb against an average realized price of $62.11/lb. Earnings quality is exceptionally robust, translating $422.2M in net income into a massive $1,007.6M in Operating Cash Flow (OCF), yielding $769.3M in self-sustaining Free Cash Flow (FCF) capable of extinguishing $200M in term debt organically.

* Urenco: Operates as a midstream toll-bridge, capturing super-normal geopolitical premiums. The company reported a 38.3% EBITDA margin ($909.0M EBITDA on $2,370.0M revenue). Its 4.2x OCF-to-Net Income conversion ratio easily funds $696.2M in enrichment CapEx while servicing a record $24.08 billion order book extending into the 2040s.

* Kazatomprom (LSE: KAP): Maintains the industry's lowest C1 cost at $18.06/lb, though margins are under assault. Operating leverage is compressing due to a 42.6% explosion in sulfuric acid costs and an aggressive Mineral Extraction Tax (MET) hike to 9% (comprising 36% of C1 costs). Total OCF matched net income at $1,668.3M, perfectly covering its $851.1M CapEx requirements.

* Arbitrage & Spot Market Capture:

* Uranium Energy Corp (NYSE: UEC): Subverts traditional mining efficiency with a 682-day Days Inventory Outstanding (DIO). By deliberately hoarding spot material and entirely avoiding legacy utility price-ceilings, UEC captured a sector-high average realized price of $82.52/lb.

* CGN Mining (HKEX: 1164): Executes an asset-light off-take model (0.79x Asset Turnover). By purchasing from Kazakh joint ventures at a guaranteed 2% spot-discount, the company posted a 204% gross profit explosion despite localized asset degradation pushing C1 costs at its Semizbay mine up to $37.00/lb.

The Cash-Burning Speculators & Forensic Triggers:

* enCore Energy (NASDAQ: EU): Despite pushing an aggressive In-Situ Recovery (ISR) narrative, the entity is bleeding cash (negative $25.0M OCF on a $63.0M net loss) and survives strictly via $110.0M in convertible notes. Crucially, management disclosed material weaknesses in internal controls and acknowledged extracting from assets with zero SEC-compliant S-K 1300 "Mineral Reserves."

* Neo Energy Metals (LSE: NEO): Triggered a critical "Going Concern" warning from independent auditors. The exploration entity reported £19,065 in cash against a £6.1 million operational burn rate, rendering its £3.1 million in subsidiary investments highly susceptible to impairment.

* China National Uranium: Displays a severe accounting discrepancy. Despite reporting $183.8M in net profit, the state-backed entity hemorrhaged -$356.7M in operating cash flows, indicating massive working capital drag or aggressive revenue recognition.

Global Supply Chain Restructuring and Regional Economic Moats

The physicality of the 2025 uranium market is defined by severe jurisdictional risk and aggressive capital redirection toward secure geopolitical corridors.

* Enrichment Monopolies and Midstream Onshoring: Western capital is aggressively flowing into Front-End choke points. Orano is deploying $1,492 million in CapEx, primarily targeting the capacity extension of the Georges Besse II enrichment plant in France and securing $900 million in US Department of Energy (DOE) funding for the IKE project in Oak Ridge, Tennessee. Urenco is expanding the Eunice (New Mexico) facility, alongside European expansions at Almelo and Gronau, effectively commercializing LEU+ capabilities to service hyperscaler AI data center demands.

* Bypassing the Russian Transport Chokepoint: Central Asian producers face acute logistics risks. To circumvent the traditional St. Petersburg export route and avoid Western sanctions, Kazatomprom successfully rerouted 48% of its Western-bound U3O8 shipments through the Trans-Caspian International Transport Route (TITR). Furthermore, producers are executing location-based "swap agreements" at Western conversion facilities like Malvési (France) and Port Hope (Canada) to entirely eliminate transit exposure.

* Jurisdictional Expropriation vs. Tier-1 Technological Fortification: Resource nationalism in emerging markets actively destroyed operator value in 2025, culminating in Orano's loss of operational control at the Somaïr mine in Niger. In stark contrast, North American operators are deploying advanced proprietary technology to reinforce their local moats. Cameco and Orano successfully commercialized the SABRE method at the McClean Lake joint venture in the Athabasca Basin, allowing for non-invasive, surface-borehole extraction of ultra-high-grade deposits without conventional shaft construction. Simultaneously, UEC executed the $175.4 million Sweetwater Acquisition in Wyoming to localize its US-centric ISR hub-and-spoke model.

HDIN Institutional Perspective

While retail momentum blindly rewards North American ISR operators for their geopolitical safety premiums, a forensic analysis reveals a severe disconnect between narrative and earnings quality. The Street continues to price Uranium Energy Corp and enCore Energy as steady-state producers; however, their financial architecture relies on highly dilutive At-The-Market (ATM) equity issuance ($287.5M for UEC) and external debt rather than organic extraction margins. We challenge the prevailing consensus that "domestic jurisdiction" equates to a standalone economic moat. True capital insulation in the 2026-2030 cycle strictly belongs to entities controlling physical midstream bottlenecks (Urenco) or generating self-sustaining, debt-extinguishing free cash flows from ultra-low-cost geology (Cameco, Kazatomprom). Junior explorers currently lack both the balance sheet and the SEC-compliant reserves required to survive localized supply chain disruptions.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."