T3 Defense Inc.: Aggressive M&A Pivot Near Petach-Tikva Hub as -$69M Working Capital Signals Severe Liquidity Squeeze

Date : 2026-06-08

Reading : 120

T3 Defense Inc.’s transition from fintech to aerospace represents a critical structural hazard for institutional LPs. Despite a $12.1 million backlog, strict ASC 606 revenue deferral rules compound a severe -$69 million working capital deficit. Geographically concentrated in Israel amidst the "Swords of Iron" conflict, the firm’s reliance on Firm-Fixed-Price (FFP) contracts without DCAA-compliant accounting guarantees forward margin compression. This exposes common equity to a toxic "death spiral" financing loop, fundamentally challenging the viability of its projected 2026 operational turnaround.

Figure T3 Defense Inc: Strategic S-1 Analysis & Forensic Diagnostic

Forensic Financials & Segmental Inventory

Forensic Financials & Segmental Inventory

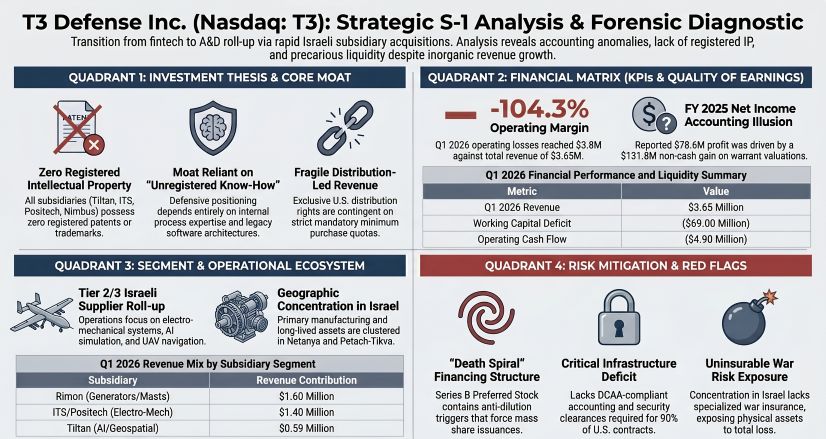

A Forensic Analysis of the T3 Defense Inc. (subject to NASDAQ minimum bid deficiency) balance sheet reveals an extreme optical divergence between reported net income and underlying operational cash burn. Historical comparisons are rendered void due to discontinued operations, and the capitalization table represents a severe dilution hazard.

* Top-Line & Earnings Mirage: Q1 2026 revenue stood at $3.65 million, generating a perilously thin gross margin of 10.1% ($370,000). The reported FY 2025 net income of $78.6 million is an accounting anomaly driven entirely by a $131.8 million non-cash gain from the fair value change in stock purchase warrant liabilities. The actual FY 2025 operating loss was $32.6 million on $0 of continuing operations revenue.

* Operating Leverage & Unit Economics: The firm is structurally incapable of absorbing general and administrative overhead, evidenced by a (104.3%) Q1 2026 operating margin. The cash conversion cycle is highly distressed; Accounts Receivable ($3.64 million) and Inventory ($3.50 million) effectively eclipse total Q1 top-line revenue, forcing the firm to finance the entire production cycle upfront.

* Segmental Incremental Margins (Q1 2026):

* Rimon: $1.60 million revenue; 20.3% gross margin.

* Tiltan: $592,000 revenue; 41.0% gross margin.

* I.T.S. / Positech: $1.40 million revenue; operating at a gross loss of $212,000.

* Other (Nimbus): $57,000 revenue.

* Capital Allocation & Intangible Overhang: Of total assets, $100.15 million is classified as Goodwill, alongside $12.54 million in intangibles. Management applies an aggressively subjective 15-year useful life to acquired AI technology, shielding the P&L from near-term amortization while introducing severe "impairment cliff" risks. R&D spending was just $274,000 (7.5% of Q1 2026 revenue), yielding strictly zero registered patents across all subsidiaries.

* Capital Structure Toxicity: The balance sheet is overwhelmed by $91.6 million in current liabilities, including $56.2 million in warrant liabilities. Operations are funded via highly dilutive Equity Lines of Credit (ELOC) and Series B Preferred Stock containing price-based anti-dilution mechanisms, setting the conditions for a continuous equity "death spiral."

Supply Chain Audit & Geo-Economic Moat

The physical footprint of T3 Defense Inc. exposes it to extreme, localized geopolitical vulnerability and strict regulatory bottlenecks. The corporate headquarters is nominally situated at 575 Fifth Ave, New York, but true operational physicality is anchored entirely in Israel.

* Geographic Footprint & Chokepoints: Serial manufacturing and R&D occur primarily at the 5 Hagvish facility in Netanya and the 2 Granit leased facility in Petach-Tikva. Nimbus operations are centered in Jerusalem. This hyper-concentration within a multi-front conflict zone leaves the supply chain exposed to uninsurable war risks and sudden labor shortages, as mandatory military reserve call-ups threaten up to 40% of the localized workforce.

* Tier-1 Vendor Dependency: Procurement relies heavily on exclusive, high-risk third-party distribution agreements. The Blade Ranger payload contract mandates strict purchase quotas (5 units in Year 1, 10 in Year 2, and 15 in Year 3). Failure to absorb this inventory results in the loss of exclusivity.

* Logistics Expansion Pivot: The firm is attempting to build a NATO-compliant logistics hub in Riga, Latvia via the Mandragola Aviation joint venture to support licensed maintenance, repair, and overhaul (MRO) and aircraft de-icing technology, requiring capital expenditures the firm currently lacks.

* Regulatory & Macro Vulnerabilities: The firm completely lacks Defense Contract Audit Agency (DCAA) compliant infrastructure and facility security clearances, precluding participation in 90% of U.S. defense contracts. Hardware manufacturing remains heavily dependent on rare earth minerals and drone components vulnerable to Chinese export controls, while ITAR/EAR compliance mechanisms are virtually non-existent.

HDIN Institutional Perspective

While retail investors may interpret the $12.1 million funded backlog and the FY 2025 "profitability" as indicators of a successful M&A integration, HDIN Research identifies a fundamentally mispriced asset operating on a broken commercial engine.

The core vulnerability lies in contract risk allocation. T3 Defense Inc.’s backlog is heavily skewed toward Firm-Fixed-Price (FFP) manufacturing agreements. For an organization publicly acknowledging zero historical cost estimation modeling capabilities, FFP exposure guarantees the firm will absorb 100% of supply chain inflation and labor escalation.

Furthermore, the corporate governance structure facilitates value extraction. CEO Menachem Shalom’s strategic debt-to-equity conversions—pricing 4.17 million shares at $0.5124 (drastically below the recent $1.50 warrant exercise threshold)—coupled with external consulting payments to Billio Ltd., demonstrate a severe misalignment with minority shareholders. Until the $69 million working capital deficit is resolved with non-dilutive capital, the operational integration of these Tier-2 Israeli assets remains mathematically unviable.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure T3 Defense Inc: Strategic S-1 Analysis & Forensic Diagnostic

Forensic Financials & Segmental InventoryA Forensic Analysis of the T3 Defense Inc. (subject to NASDAQ minimum bid deficiency) balance sheet reveals an extreme optical divergence between reported net income and underlying operational cash burn. Historical comparisons are rendered void due to discontinued operations, and the capitalization table represents a severe dilution hazard.

* Top-Line & Earnings Mirage: Q1 2026 revenue stood at $3.65 million, generating a perilously thin gross margin of 10.1% ($370,000). The reported FY 2025 net income of $78.6 million is an accounting anomaly driven entirely by a $131.8 million non-cash gain from the fair value change in stock purchase warrant liabilities. The actual FY 2025 operating loss was $32.6 million on $0 of continuing operations revenue.

* Operating Leverage & Unit Economics: The firm is structurally incapable of absorbing general and administrative overhead, evidenced by a (104.3%) Q1 2026 operating margin. The cash conversion cycle is highly distressed; Accounts Receivable ($3.64 million) and Inventory ($3.50 million) effectively eclipse total Q1 top-line revenue, forcing the firm to finance the entire production cycle upfront.

* Segmental Incremental Margins (Q1 2026):

* Rimon: $1.60 million revenue; 20.3% gross margin.

* Tiltan: $592,000 revenue; 41.0% gross margin.

* I.T.S. / Positech: $1.40 million revenue; operating at a gross loss of $212,000.

* Other (Nimbus): $57,000 revenue.

* Capital Allocation & Intangible Overhang: Of total assets, $100.15 million is classified as Goodwill, alongside $12.54 million in intangibles. Management applies an aggressively subjective 15-year useful life to acquired AI technology, shielding the P&L from near-term amortization while introducing severe "impairment cliff" risks. R&D spending was just $274,000 (7.5% of Q1 2026 revenue), yielding strictly zero registered patents across all subsidiaries.

* Capital Structure Toxicity: The balance sheet is overwhelmed by $91.6 million in current liabilities, including $56.2 million in warrant liabilities. Operations are funded via highly dilutive Equity Lines of Credit (ELOC) and Series B Preferred Stock containing price-based anti-dilution mechanisms, setting the conditions for a continuous equity "death spiral."

Supply Chain Audit & Geo-Economic Moat

The physical footprint of T3 Defense Inc. exposes it to extreme, localized geopolitical vulnerability and strict regulatory bottlenecks. The corporate headquarters is nominally situated at 575 Fifth Ave, New York, but true operational physicality is anchored entirely in Israel.

* Geographic Footprint & Chokepoints: Serial manufacturing and R&D occur primarily at the 5 Hagvish facility in Netanya and the 2 Granit leased facility in Petach-Tikva. Nimbus operations are centered in Jerusalem. This hyper-concentration within a multi-front conflict zone leaves the supply chain exposed to uninsurable war risks and sudden labor shortages, as mandatory military reserve call-ups threaten up to 40% of the localized workforce.

* Tier-1 Vendor Dependency: Procurement relies heavily on exclusive, high-risk third-party distribution agreements. The Blade Ranger payload contract mandates strict purchase quotas (5 units in Year 1, 10 in Year 2, and 15 in Year 3). Failure to absorb this inventory results in the loss of exclusivity.

* Logistics Expansion Pivot: The firm is attempting to build a NATO-compliant logistics hub in Riga, Latvia via the Mandragola Aviation joint venture to support licensed maintenance, repair, and overhaul (MRO) and aircraft de-icing technology, requiring capital expenditures the firm currently lacks.

* Regulatory & Macro Vulnerabilities: The firm completely lacks Defense Contract Audit Agency (DCAA) compliant infrastructure and facility security clearances, precluding participation in 90% of U.S. defense contracts. Hardware manufacturing remains heavily dependent on rare earth minerals and drone components vulnerable to Chinese export controls, while ITAR/EAR compliance mechanisms are virtually non-existent.

HDIN Institutional Perspective

While retail investors may interpret the $12.1 million funded backlog and the FY 2025 "profitability" as indicators of a successful M&A integration, HDIN Research identifies a fundamentally mispriced asset operating on a broken commercial engine.

The core vulnerability lies in contract risk allocation. T3 Defense Inc.’s backlog is heavily skewed toward Firm-Fixed-Price (FFP) manufacturing agreements. For an organization publicly acknowledging zero historical cost estimation modeling capabilities, FFP exposure guarantees the firm will absorb 100% of supply chain inflation and labor escalation.

Furthermore, the corporate governance structure facilitates value extraction. CEO Menachem Shalom’s strategic debt-to-equity conversions—pricing 4.17 million shares at $0.5124 (drastically below the recent $1.50 warrant exercise threshold)—coupled with external consulting payments to Billio Ltd., demonstrate a severe misalignment with minority shareholders. Until the $69 million working capital deficit is resolved with non-dilutive capital, the operational integration of these Tier-2 Israeli assets remains mathematically unviable.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."