HOYA Corporation: Strategic CapEx Expansion Near Singapore and Vietnam as EUV Component Demand Signals Sustained Margin Accretion

Date : 2026-06-08

Reading : 325

HOYA Corporation’s FY2025 financial architecture reveals a fortress balance sheet, deploying $439.34 million in capital expenditures predominantly routed into Southeast Asian hubs like Singapore and Vietnam. By aggressively expanding capacity for Extreme Ultraviolet (EUV) mask blanks and 3.5-inch data center substrates, the company circumvents regional tariff vulnerabilities while solidifying its bottleneck supplier status in the AI hardware chain. For institutional allocators, HOYA’s $1.42 billion free cash flow and 25.4% ROE confirm an unleveraged capital structure engineered to offset retail margin compression through structural B2B premiumization.

Figure HOYA Corporation FY2025: Strategic Performance & Global Risk Architecture

Segmental Incremental Margins and Capital Allocation Strategies

HOYA (TYO: 7741) operates a highly cash-generative, dual-engine portfolio, entirely avoiding leveraged expansion. Reporting under IFRS, the firm translates top-line growth directly into massive shareholder distributions, exceeding its own free cash flow generation by drawing on its $3.83 billion liquidity reserves.

Quantitative Inventory & Operating Leverage

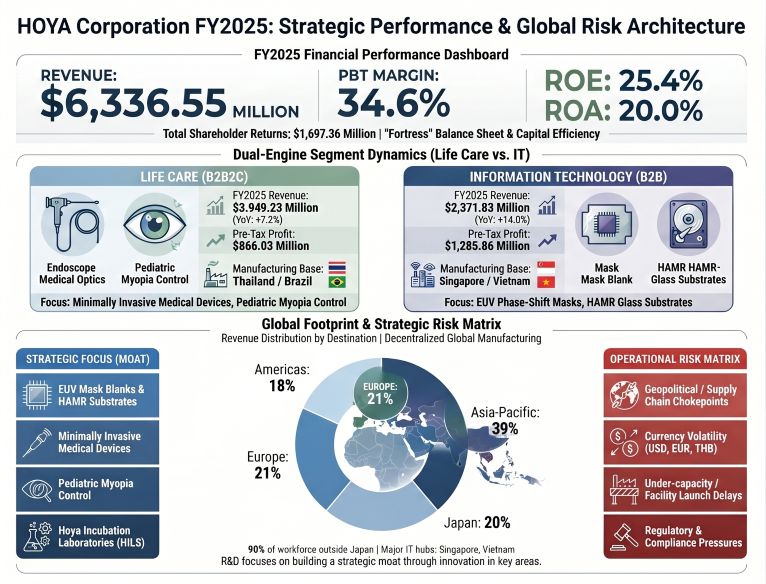

* Consolidated Top-Line & Profitability: Revenue reached $6,336.55 million (+9.4% YoY), driving a Profit Before Tax (PBT) of $2,190.75 million (+26.0% YoY). The PBT Margin expanded by 4.6 basis points to 34.6%, catapulting ROE to 25.4% (+4.6 pt) and ROA to 20.0% (+3.4 pt).

* Information/Communication (IT) Segment: Functioning as the high-margin engine, revenue hit $2,371.83 million (+14.0% YoY) with pre-tax profits at $1,285.86 million (+12.9% YoY). The electronics sub-segment generated $1,977.40 million, supported by surging EUV mask blank demand and FPD photomask ramps in China.

* Life Care Segment: Revenue landed at $3,949.23 million (+7.2% YoY) with a PBT of $866.03 million (+43.3% YoY). The healthcare sub-segment ($3,013.73 million) and medical sub-segment ($935.48 million) benefited from stabilized European endoscope sales and robust contact lens demand.

* Free Cash Flow (FCF) Conversion: Operating Cash Flow (OCF) stood at $1,861.66 million. With $439.34 million deployed to CapEx (23.6% of OCF), FCF reached $1,422.32 million—a highly efficient 76.4% conversion rate.

* Capital Allocation: Shareholder returns heavily outpaced FCF. HOYA executed $1,149.77 million in share buybacks and $547.59 million in dividends, culminating in a total payout of $1,697.36 million. Additionally, a post-balance sheet cancellation of 3,576,300 treasury shares (1.07% of outstanding stock) was executed on May 15, 2026.

* R&D-to-Moat Translation: Strict expensing of $242.64 million in R&D ($150.29 million for Life Care; $88.31 million for IT) successfully commercialized high-barrier assets, notably Extended Depth of Focus (EDOF) intraocular lenses and Heat-Assisted Magnetic Recording (HAMR) compatible glass disks.

Price-Mix Variance & Unit Economics

HOYA mitigates global inflation via aggressive price-mix optimization rather than margin-eroding discounting. In IT, unit economics reflect a structural pivot away from declining legacy 2.5-inch HDD substrates toward high-margin 3.5-inch nearline storage disks for data centers. In retail, the company absorbs mass-market pricing pressure by upselling consumers to the high-value hoyaONE private brand and Meiryo premium progressive lens coatings. The April 1, 2026, strategic spin-off of the Eyecity retail business into HOYA Eyecare Retailing LLC ($210.44 million in assets; $752.11 million FY2025 revenue) signals a deliberate structural separation to optimize B2C commercial agility.

Geographic Decentralization and Raw Material Procurement Moat

HOYA operates an aggressively decentralized manufacturing footprint, systematically distributing its 37,752-strong workforce (90% non-Japanese) to mitigate both geopolitical tariff shocks and regional climate vulnerabilities.

* Southeast Asia Volume & Precision Hubs: The primary node for semiconductor capacity expansion is HOYA ELECTRONICS SINGAPORE ($124.20 million book value), which absorbed $72.81 million in FY2025 CapEx. Vietnam serves as the essential hardware foundation, with HOYA GLASS DISK VIETNAM and VIETNAM II capturing a $51.02 million CapEx injection. HOYA Lamphun in Thailand executes medical manufacturing via an $18.08 million expansion plan.

* Domestic Core & Americas: The Akishima, Nagasaka, and Hachioji plants in Japan saw $38.08 million in combined CapEx to augment domestic IT precision manufacturing. In the Americas ($1,151.67 million revenue, 18% of total), specialized medical manufacturing is anchored by MICROLINE SURGICAL and PENTAX, supported by localized production at HOYA OPTICAL LABS OF AMERICA ($62.02 million book value).

* Supply Chain Vulnerability & ESG Execution: Procurement heavily relies on highly specialized raw materials. Management utilizes elevated safety stock and natural FX hedging (matching export receivables to local import payables) to absorb macro volatility. Environmentally, the group cut Scope 1 and 2 emissions by 23% to 404,000 t-CO2, achieving a 19% renewable energy ratio on its 2040 RE100 mandate.

HDIN Institutional Perspective: The Seagate Concentration and Tax Litigation Overhang

While management accurately touts an unassailable technological moat in AI and EUV components, the financial architecture harbors specific concentrations that institutional allocators must price into their models.

First, the $2.37 billion IT segment exhibits extreme single-client dependency. Seagate Technology LLC accounted for $744.76 million (11.75%) of HOYA's total consolidated FY2025 revenue. Consequently, the bullish thesis on HAMR glass substrates is directly tethered to the capital expenditure cycles of a single hardware manufacturer, contradicting the group’s broader thesis of structural decentralization.

Second, the "fortress balance sheet" narrative obscures a significant legal drain: $136.80 million remains locked as "Suspense payments - taxes" due to protracted transfer pricing disputes with the Tokyo Regional Taxation Bureau spanning FY2007 through FY2018. While HOYA maintains zero active IP litigation or medical device recalls, this capital entrapment degrades true ROIC. Furthermore, the explicit necessity to launch the HOYA Incubation Laboratories (HILS) in FY2026 suggests internal recognition that its current highly decentralized, B2B2C bifurcated model may lack the cross-segment R&D agility required to capture next-generation tech pipelines beyond the 2030 horizon.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

Figure HOYA Corporation FY2025: Strategic Performance & Global Risk Architecture

Segmental Incremental Margins and Capital Allocation Strategies

HOYA (TYO: 7741) operates a highly cash-generative, dual-engine portfolio, entirely avoiding leveraged expansion. Reporting under IFRS, the firm translates top-line growth directly into massive shareholder distributions, exceeding its own free cash flow generation by drawing on its $3.83 billion liquidity reserves.

Quantitative Inventory & Operating Leverage

* Consolidated Top-Line & Profitability: Revenue reached $6,336.55 million (+9.4% YoY), driving a Profit Before Tax (PBT) of $2,190.75 million (+26.0% YoY). The PBT Margin expanded by 4.6 basis points to 34.6%, catapulting ROE to 25.4% (+4.6 pt) and ROA to 20.0% (+3.4 pt).

* Information/Communication (IT) Segment: Functioning as the high-margin engine, revenue hit $2,371.83 million (+14.0% YoY) with pre-tax profits at $1,285.86 million (+12.9% YoY). The electronics sub-segment generated $1,977.40 million, supported by surging EUV mask blank demand and FPD photomask ramps in China.

* Life Care Segment: Revenue landed at $3,949.23 million (+7.2% YoY) with a PBT of $866.03 million (+43.3% YoY). The healthcare sub-segment ($3,013.73 million) and medical sub-segment ($935.48 million) benefited from stabilized European endoscope sales and robust contact lens demand.

* Free Cash Flow (FCF) Conversion: Operating Cash Flow (OCF) stood at $1,861.66 million. With $439.34 million deployed to CapEx (23.6% of OCF), FCF reached $1,422.32 million—a highly efficient 76.4% conversion rate.

* Capital Allocation: Shareholder returns heavily outpaced FCF. HOYA executed $1,149.77 million in share buybacks and $547.59 million in dividends, culminating in a total payout of $1,697.36 million. Additionally, a post-balance sheet cancellation of 3,576,300 treasury shares (1.07% of outstanding stock) was executed on May 15, 2026.

* R&D-to-Moat Translation: Strict expensing of $242.64 million in R&D ($150.29 million for Life Care; $88.31 million for IT) successfully commercialized high-barrier assets, notably Extended Depth of Focus (EDOF) intraocular lenses and Heat-Assisted Magnetic Recording (HAMR) compatible glass disks.

Price-Mix Variance & Unit Economics

HOYA mitigates global inflation via aggressive price-mix optimization rather than margin-eroding discounting. In IT, unit economics reflect a structural pivot away from declining legacy 2.5-inch HDD substrates toward high-margin 3.5-inch nearline storage disks for data centers. In retail, the company absorbs mass-market pricing pressure by upselling consumers to the high-value hoyaONE private brand and Meiryo premium progressive lens coatings. The April 1, 2026, strategic spin-off of the Eyecity retail business into HOYA Eyecare Retailing LLC ($210.44 million in assets; $752.11 million FY2025 revenue) signals a deliberate structural separation to optimize B2C commercial agility.

Geographic Decentralization and Raw Material Procurement Moat

HOYA operates an aggressively decentralized manufacturing footprint, systematically distributing its 37,752-strong workforce (90% non-Japanese) to mitigate both geopolitical tariff shocks and regional climate vulnerabilities.

* Southeast Asia Volume & Precision Hubs: The primary node for semiconductor capacity expansion is HOYA ELECTRONICS SINGAPORE ($124.20 million book value), which absorbed $72.81 million in FY2025 CapEx. Vietnam serves as the essential hardware foundation, with HOYA GLASS DISK VIETNAM and VIETNAM II capturing a $51.02 million CapEx injection. HOYA Lamphun in Thailand executes medical manufacturing via an $18.08 million expansion plan.

* Domestic Core & Americas: The Akishima, Nagasaka, and Hachioji plants in Japan saw $38.08 million in combined CapEx to augment domestic IT precision manufacturing. In the Americas ($1,151.67 million revenue, 18% of total), specialized medical manufacturing is anchored by MICROLINE SURGICAL and PENTAX, supported by localized production at HOYA OPTICAL LABS OF AMERICA ($62.02 million book value).

* Supply Chain Vulnerability & ESG Execution: Procurement heavily relies on highly specialized raw materials. Management utilizes elevated safety stock and natural FX hedging (matching export receivables to local import payables) to absorb macro volatility. Environmentally, the group cut Scope 1 and 2 emissions by 23% to 404,000 t-CO2, achieving a 19% renewable energy ratio on its 2040 RE100 mandate.

HDIN Institutional Perspective: The Seagate Concentration and Tax Litigation Overhang

While management accurately touts an unassailable technological moat in AI and EUV components, the financial architecture harbors specific concentrations that institutional allocators must price into their models.

First, the $2.37 billion IT segment exhibits extreme single-client dependency. Seagate Technology LLC accounted for $744.76 million (11.75%) of HOYA's total consolidated FY2025 revenue. Consequently, the bullish thesis on HAMR glass substrates is directly tethered to the capital expenditure cycles of a single hardware manufacturer, contradicting the group’s broader thesis of structural decentralization.

Second, the "fortress balance sheet" narrative obscures a significant legal drain: $136.80 million remains locked as "Suspense payments - taxes" due to protracted transfer pricing disputes with the Tokyo Regional Taxation Bureau spanning FY2007 through FY2018. While HOYA maintains zero active IP litigation or medical device recalls, this capital entrapment degrades true ROIC. Furthermore, the explicit necessity to launch the HOYA Incubation Laboratories (HILS) in FY2026 suggests internal recognition that its current highly decentralized, B2B2C bifurcated model may lack the cross-segment R&D agility required to capture next-generation tech pipelines beyond the 2030 horizon.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*