Global Tobacco Intermediaries 2026 Outlook: Why Universal Corporation and Pyxus International Diverge on Capital Allocation Amid Southern Hemisphere Oversupply

Date : 2026-06-08

Reading : 460

As Southern Hemisphere crop yields surged in FY2026—driving global burley production up 54%—Universal Corporation and Pyxus International shifted from managing undersupply to defending against severe inventory bloat. While Universal mitigates combustible tobacco’s 2% secular decline through its capital-intensive plant-based Ingredients diversification in Pennsylvania, Pyxus leans on highly leveraged, pure-play logistics. The critical divergence lies in balance sheet resilience: Universal locks in long-term supply via $196 million in direct farmer advances, whereas Pyxus relies on off-balance-sheet guarantees ahead of a looming 2027 maturity wall.

Figure Global Tobacco Intermediaries: 2025-2026 Strategic Benchmarking Report

Forensic Financials & Segmental Dislocation

Forensic Financials & Segmental Dislocation

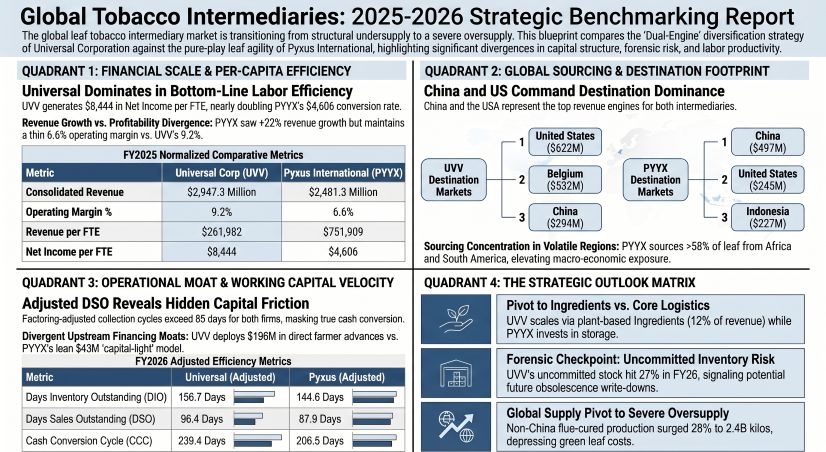

A Forensic Analysis of the FY2025/FY2026 filings reveals a structural anomaly across the sector: revenue growth is a poor proxy for operational volume. Pass-through pricing dynamics mean top-line fluctuations mechanically reflect green tobacco commodity costs rather than throughput. In FY2026, Pyxus processed 381.7 million kilos (a mere 0.4% YoY decline), yet product revenues fell 4.3% due to a 3.8% drop in the average price per kilo ($5.86), while its gross profit per kilo remained remarkably rigid at $0.82.

Table Quantitative Inventory & Capital Structure Audit

*Note: Universal’s FY25 bottom-line contraction was distorted by a $14.1 million non-cash pension settlement and $10.6 million in restructuring costs tied to European sheet tobacco consolidation.*

The "Dual-Engine" Capex vs. Pure-Play Logistics

Universal is aggressively funding its non-tobacco diversification. FY27 Capex is capped at $55-$65 million, heavily targeted at its Lancaster, Pennsylvania facility expansion, FruitSmart in Washington State, and Silva International in Illinois. However, this shift is currently a margin drain; the Ingredients segment suffered an $8.6 million inventory write-down at Shank's and a massive $41.1 million non-cash goodwill impairment in FY26. Conversely, Pyxus's $38.4 million planned FY27 Capex is strictly reactionary logistics, targeted at building and refurbishing warehouses in South America and Africa to physically house the sector's uncommitted crop oversupply (industry-wide uncommitted inventory jumped from 22 million to 169 million kilos).

Supply Chain Audit & Geo-Economic Arbitrage Moats

The physical arbitrage model of these intermediaries involves sourcing in highly volatile agricultural markets and capturing value in developed manufacturing hubs.

* Destination Consolidation: Both companies face extreme monopsony risk. Universal generates 60% of its revenue from six buyers, led by Philip Morris International ($620M), Imperial Brands ($400M), and JTI ($250M). Pyxus derives at least 30% of its revenue from PMI, JTI, and the state-owned China National Tobacco Corporation (CNTC). Primary destination hubs include China, the United States, and European storage facilities in Belgium.

* Geographic Sourcing Exclusivity: Pyxus is heavily exposed to localized inflation and currency devaluation in Argentina, Malawi, and Zimbabwe, drawing 58.1% of its leaf from Africa and South America. Universal holds a unique structural moat as the sole global supplier with meaningful dark air-cured production across the Dominican Republic, Ecuador, Hungary, Italy, Mexico, Paraguay, and the Philippines.

* The Agronomic Tech Moat: Multinational manufacturers strictly require GAP/ESG-compliant leaf. Universal’s MobiLeaf and Pyxus’s SENTRI digital track-and-trace platforms act as regulatory barriers to entry, locking undercapitalized regional competitors out of the compliant leaf supply chain.

HDIN Institutional Perspective

1. The DSO and Liquidity Illusion

While Pyxus reports a GAAP Days Sales Outstanding (DSO) of 36.2 days, a forensic review of the footnotes reveals heavy reliance on Variable Interest Entities (VIEs) and securitization facilities. Pyxus removed $341.7 million in receivables off-balance-sheet at FY26 year-end. Universal similarly initiated a factoring program, selling $208.7 million. Adjusted for this financial engineering, both companies operate with structurally elongated Cash Conversion Cycles characteristic of defensive capital-intensive intermediaries. Pyxus’s tight 1.20x interest coverage ratio, combined with a "Cash Dominion" covenant trigger on its $150M ABL Facility, leaves it highly vulnerable to variable interest rate shocks (a 1% hike equates to an $11.3 million expense increase).

2. The Inventory Obsolescence Blind Spot

We challenge the carrying value of sector inventories amid global oversupply. Universal transparently recorded a $52.0 million inventory write-down in FY26 (primarily dark air-cured tobacco) after remediating a Material Weakness in physical inventory counts. Pyxus obscures its exact write-down figures within its broader Cost of Goods Sold. With the WHO FCTC pushing crop diversification mandates and the U.S. FDA proposing a strict 0.7 mg/g nicotine cap, the risk of holding "uncommitted" stock is severe. Universal’s $222.3 million uncommitted stockpile presents higher absolute valuation risk, but Pyxus’s lack of explicit COGS disaggregation presents a structural audit blind spot the Street hasn't adequately priced.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Global Tobacco Intermediaries: 2025-2026 Strategic Benchmarking Report

Forensic Financials & Segmental DislocationA Forensic Analysis of the FY2025/FY2026 filings reveals a structural anomaly across the sector: revenue growth is a poor proxy for operational volume. Pass-through pricing dynamics mean top-line fluctuations mechanically reflect green tobacco commodity costs rather than throughput. In FY2026, Pyxus processed 381.7 million kilos (a mere 0.4% YoY decline), yet product revenues fell 4.3% due to a 3.8% drop in the average price per kilo ($5.86), while its gross profit per kilo remained remarkably rigid at $0.82.

Table Quantitative Inventory & Capital Structure Audit

| Metric (FY2025/FY2026 Assessed) | Universal Corporation | Pyxus International |

|---|---|---|

| FY25 Core Revenue | $2,947.3M (+7.2% YoY) | $2,481.3M (+22.1% YoY) |

| FY25 Net Income / Conversion | $95.0M (-20.5% YoY) | $8,444 per FTE | $15.2M (+469.5% YoY) | $4,606 per FTE |

| Working Capital (Adjusted DSO) | 96.4 Days (Adjusted for $208.7M Factoring) | 87.9 Days (Adjusted for $341.7M Securitization) |

| FY26 Uncommitted Inventory | $222.3M (27% of tobacco inventory) | $45.2M (8.9% of processed inventory) |

| FY26 Gross Farmer Advances | $196.0M (with $16.0M allowance) | $43.3M net ($119.7M in off-balance-sheet guarantees) |

| Debt & Refinancing Runway | Net Debt/EBITDA: 2.79× | Maturities: 2030/2032 | Net Debt/EBITDA: 4.44× | Maturity Wall: Dec. 31, 2027 |

The "Dual-Engine" Capex vs. Pure-Play Logistics

Universal is aggressively funding its non-tobacco diversification. FY27 Capex is capped at $55-$65 million, heavily targeted at its Lancaster, Pennsylvania facility expansion, FruitSmart in Washington State, and Silva International in Illinois. However, this shift is currently a margin drain; the Ingredients segment suffered an $8.6 million inventory write-down at Shank's and a massive $41.1 million non-cash goodwill impairment in FY26. Conversely, Pyxus's $38.4 million planned FY27 Capex is strictly reactionary logistics, targeted at building and refurbishing warehouses in South America and Africa to physically house the sector's uncommitted crop oversupply (industry-wide uncommitted inventory jumped from 22 million to 169 million kilos).

Supply Chain Audit & Geo-Economic Arbitrage Moats

The physical arbitrage model of these intermediaries involves sourcing in highly volatile agricultural markets and capturing value in developed manufacturing hubs.

* Destination Consolidation: Both companies face extreme monopsony risk. Universal generates 60% of its revenue from six buyers, led by Philip Morris International ($620M), Imperial Brands ($400M), and JTI ($250M). Pyxus derives at least 30% of its revenue from PMI, JTI, and the state-owned China National Tobacco Corporation (CNTC). Primary destination hubs include China, the United States, and European storage facilities in Belgium.

* Geographic Sourcing Exclusivity: Pyxus is heavily exposed to localized inflation and currency devaluation in Argentina, Malawi, and Zimbabwe, drawing 58.1% of its leaf from Africa and South America. Universal holds a unique structural moat as the sole global supplier with meaningful dark air-cured production across the Dominican Republic, Ecuador, Hungary, Italy, Mexico, Paraguay, and the Philippines.

* The Agronomic Tech Moat: Multinational manufacturers strictly require GAP/ESG-compliant leaf. Universal’s MobiLeaf and Pyxus’s SENTRI digital track-and-trace platforms act as regulatory barriers to entry, locking undercapitalized regional competitors out of the compliant leaf supply chain.

HDIN Institutional Perspective

1. The DSO and Liquidity Illusion

While Pyxus reports a GAAP Days Sales Outstanding (DSO) of 36.2 days, a forensic review of the footnotes reveals heavy reliance on Variable Interest Entities (VIEs) and securitization facilities. Pyxus removed $341.7 million in receivables off-balance-sheet at FY26 year-end. Universal similarly initiated a factoring program, selling $208.7 million. Adjusted for this financial engineering, both companies operate with structurally elongated Cash Conversion Cycles characteristic of defensive capital-intensive intermediaries. Pyxus’s tight 1.20x interest coverage ratio, combined with a "Cash Dominion" covenant trigger on its $150M ABL Facility, leaves it highly vulnerable to variable interest rate shocks (a 1% hike equates to an $11.3 million expense increase).

2. The Inventory Obsolescence Blind Spot

We challenge the carrying value of sector inventories amid global oversupply. Universal transparently recorded a $52.0 million inventory write-down in FY26 (primarily dark air-cured tobacco) after remediating a Material Weakness in physical inventory counts. Pyxus obscures its exact write-down figures within its broader Cost of Goods Sold. With the WHO FCTC pushing crop diversification mandates and the U.S. FDA proposing a strict 0.7 mg/g nicotine cap, the risk of holding "uncommitted" stock is severe. Universal’s $222.3 million uncommitted stockpile presents higher absolute valuation risk, but Pyxus’s lack of explicit COGS disaggregation presents a structural audit blind spot the Street hasn't adequately priced.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."