Tata Chemicals: Value-over-Volume Pivot Near Cuddalore Tier-1 Facility as 74-bps Margin Compression Signals Aggressive Price-Mix Deflation

Date : 2026-06-09

Reading : 191

Despite a $196.8 million statutory net loss triggered by North American goodwill impairments, NSE: TATACHEM generated $145.6 million in operating cash flow during FY26. This stark divergence highlights a robust defense of India-based market share against a 3.8-million-tonne Chinese supply overhang. For institutional LPs, the underlying narrative is not operational failure, but rather a deliberate balance sheet cleansing. By stretching accounts payable to 81 days and defending positive free cash flow, management is self-funding a critical capital pivot toward European pharmaceutical-grade extraction and localized battery-material supply chains.

Figure Tata Chemicals Limited FY2026: Strategic Diagnostic & Institutional Performance Blueprint

Financial Architecture & Segmental Incremental Margins

Financial Architecture & Segmental Incremental Margins

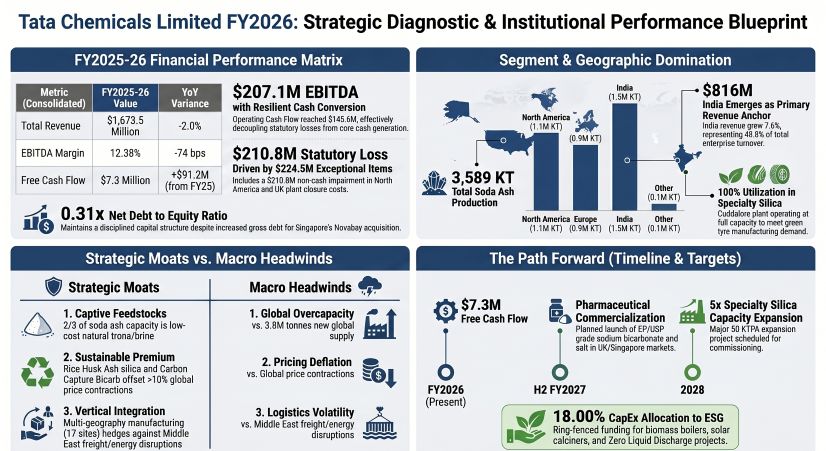

A forensic analysis of the FY26 consolidated financials reveals a structurally resilient cash-generation engine masked by macroeconomic accounting distortions. The 74-bps EBITDA margin compression is a direct output of severe price-mix variance, where a >10% global pricing deflation in basic alkalis outpaced input cost optimizations.

Quantitative Inventory & Capital Diagnostics (FY26 vs FY25)

* Top-Line & Yields: Consolidated revenue stood at $1,673.5 million (-2.0% YoY), with EBITDA printing at $207.1 million (-7.6% YoY). The Asset Turnover ratio dipped marginally to 0.37x due to heavy capitalization of ongoing expansion projects.

* Operating Leverage Breakdown: Basic Chemistry revenue contracted to $1,322.0 million, severely impacted by a $224.5 million exceptional charge (predominantly a $210.8 million non-cash goodwill impairment at the US TCNA subsidiary). Conversely, Specialty Products acted as a margin stabilizer, generating $353.0 million in revenue with a 5.5% segment margin.

* Free Cash Flow (FCF) Conversion: The enterprise reversed a prior-year deficit, delivering $7.3 million in positive FCF after executing a $138.3 million Capital Expenditure program. Operating Cash Flow hit $145.6 million, validating earnings quality over statutory metrics.

* Internal Capital Allocation & Solvency: Net Debt to Equity remains structurally sound at 0.31x, though Net Debt/EBITDA temporarily spiked to 3.8x due to the denominator effect of compressed earnings. Gross debt expanded to $918.1 million to fund high-margin geographic expansion, notably the Singapore Novabay acquisition.

Unit Economics & Geographic Arbitrage

India remains the absolute anchor, accounting for 48.8% of global revenue ($816.0 million, +7.6% YoY) fueled by aggressive domestic demand in solar glass and EV battery components. In contrast, US export volumes collapsed by 16% as heavily discounted Chinese natural soda ash flooded Southeast Asian and Latin American markets.

Geo-Economic Moat & Supply Chain Infrastructure Audit

The physical architecture of Tata Chemicals relies heavily on capturing localized raw material monopolies while migrating away from geopolitically sensitive energy imports. The firm operates 17 active manufacturing hubs, structurally divided by feedstock type.

Physicality & Logistics Hotspots

* The Wyoming & Kenya Trona/Brine Moat: Over two-thirds of the firm's 3.9 million MT soda ash capacity is anchored in natural deposits. The Green River Basin (USA) and Lake Magadi (Kenya) provide a massive cost advantage over synthetic Solvay competitors. However, operations at Lake Magadi are actively de-risking their Heavy Fuel Oil (HFO) reliance—vulnerable to Red Sea/Middle East transit disruptions—by commissioning a 50 KTPA solar-powered electric calciner.

* India Tier-1 Facilities: The Mithapur integrated complex (Gujarat) achieved a 1 Million Metric Tonne production milestone, leveraging captive solar salt and limestone. Meanwhile, the Cuddalore Tier-1 facility (Tamil Nadu) is operating Highly Dispersible Silica (HDS) lines at 100% capacity utilization, initiating a localized $138.3 million CapEx pivot to scale a 3.5 KTPA microsphere silica line to 50 KTPA by 2028.

* European & Asian Pharmaceutical Cutover: The closure of the unviable Lostock plant in the UK (incurring $7.5 million in exceptional closure costs) facilitated a strategic transition. The Middlewich facility is now aggressively commercializing "Medi-Salt," directly complementing the 60 KTPA cGMP automated pharmaceutical-grade capacity acquired via Novabay Pte. Ltd. in Singapore.

HDIN Institutional Perspective: Buy the Cash Flow, Price the Friction

The Street may penalize NSE: TATACHEM for its -7.68% reported Return on Net Worth (ROE), interpreting the $210.8 million North American impairment as a systemic degradation of terminal value. HDIN Research challenges this consensus. The statutory loss is a lagging indicator of FY25/FY26 Chinese dumping. The forward indicator is the firm's aggressive $10.9 million R&D-to-moat translation—specifically the commercialization of Rice Husk Ash (RHA) silica and indigenous sodium-ion battery technology validated at the Pune and Bengaluru R&D centers.

However, two unpriced downside risks demand institutional hedging:

1. Environmental ARO Tail-Risk: While the balance sheet provisions $40.39 million for Asset Retirement Obligations (ARO), a material regulatory friction point materialized on May 25, 2026, when the High Court of Gujarat rejected the firm's land rights claim regarding legacy wastewater discharge at Mithapur. This introduces an unquantified contingent liability that could disrupt future margin profiles.

2. Human Capital Operational Friction: Despite AI-driven automation efforts, the operational execution remains dangerously leveraged on contractual labor (89.1% of the blue-collar workforce). The recording of two worker fatalities in FY26, juxtaposed against an otherwise low TRIFR of 0.77, signals critical contractor-level vulnerabilities within the high-heat manufacturing supply chain.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant)

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Tata Chemicals Limited FY2026: Strategic Diagnostic & Institutional Performance Blueprint

Financial Architecture & Segmental Incremental MarginsA forensic analysis of the FY26 consolidated financials reveals a structurally resilient cash-generation engine masked by macroeconomic accounting distortions. The 74-bps EBITDA margin compression is a direct output of severe price-mix variance, where a >10% global pricing deflation in basic alkalis outpaced input cost optimizations.

Quantitative Inventory & Capital Diagnostics (FY26 vs FY25)

* Top-Line & Yields: Consolidated revenue stood at $1,673.5 million (-2.0% YoY), with EBITDA printing at $207.1 million (-7.6% YoY). The Asset Turnover ratio dipped marginally to 0.37x due to heavy capitalization of ongoing expansion projects.

* Operating Leverage Breakdown: Basic Chemistry revenue contracted to $1,322.0 million, severely impacted by a $224.5 million exceptional charge (predominantly a $210.8 million non-cash goodwill impairment at the US TCNA subsidiary). Conversely, Specialty Products acted as a margin stabilizer, generating $353.0 million in revenue with a 5.5% segment margin.

* Free Cash Flow (FCF) Conversion: The enterprise reversed a prior-year deficit, delivering $7.3 million in positive FCF after executing a $138.3 million Capital Expenditure program. Operating Cash Flow hit $145.6 million, validating earnings quality over statutory metrics.

* Internal Capital Allocation & Solvency: Net Debt to Equity remains structurally sound at 0.31x, though Net Debt/EBITDA temporarily spiked to 3.8x due to the denominator effect of compressed earnings. Gross debt expanded to $918.1 million to fund high-margin geographic expansion, notably the Singapore Novabay acquisition.

Unit Economics & Geographic Arbitrage

India remains the absolute anchor, accounting for 48.8% of global revenue ($816.0 million, +7.6% YoY) fueled by aggressive domestic demand in solar glass and EV battery components. In contrast, US export volumes collapsed by 16% as heavily discounted Chinese natural soda ash flooded Southeast Asian and Latin American markets.

Geo-Economic Moat & Supply Chain Infrastructure Audit

The physical architecture of Tata Chemicals relies heavily on capturing localized raw material monopolies while migrating away from geopolitically sensitive energy imports. The firm operates 17 active manufacturing hubs, structurally divided by feedstock type.

Physicality & Logistics Hotspots

* The Wyoming & Kenya Trona/Brine Moat: Over two-thirds of the firm's 3.9 million MT soda ash capacity is anchored in natural deposits. The Green River Basin (USA) and Lake Magadi (Kenya) provide a massive cost advantage over synthetic Solvay competitors. However, operations at Lake Magadi are actively de-risking their Heavy Fuel Oil (HFO) reliance—vulnerable to Red Sea/Middle East transit disruptions—by commissioning a 50 KTPA solar-powered electric calciner.

* India Tier-1 Facilities: The Mithapur integrated complex (Gujarat) achieved a 1 Million Metric Tonne production milestone, leveraging captive solar salt and limestone. Meanwhile, the Cuddalore Tier-1 facility (Tamil Nadu) is operating Highly Dispersible Silica (HDS) lines at 100% capacity utilization, initiating a localized $138.3 million CapEx pivot to scale a 3.5 KTPA microsphere silica line to 50 KTPA by 2028.

* European & Asian Pharmaceutical Cutover: The closure of the unviable Lostock plant in the UK (incurring $7.5 million in exceptional closure costs) facilitated a strategic transition. The Middlewich facility is now aggressively commercializing "Medi-Salt," directly complementing the 60 KTPA cGMP automated pharmaceutical-grade capacity acquired via Novabay Pte. Ltd. in Singapore.

HDIN Institutional Perspective: Buy the Cash Flow, Price the Friction

The Street may penalize NSE: TATACHEM for its -7.68% reported Return on Net Worth (ROE), interpreting the $210.8 million North American impairment as a systemic degradation of terminal value. HDIN Research challenges this consensus. The statutory loss is a lagging indicator of FY25/FY26 Chinese dumping. The forward indicator is the firm's aggressive $10.9 million R&D-to-moat translation—specifically the commercialization of Rice Husk Ash (RHA) silica and indigenous sodium-ion battery technology validated at the Pune and Bengaluru R&D centers.

However, two unpriced downside risks demand institutional hedging:

1. Environmental ARO Tail-Risk: While the balance sheet provisions $40.39 million for Asset Retirement Obligations (ARO), a material regulatory friction point materialized on May 25, 2026, when the High Court of Gujarat rejected the firm's land rights claim regarding legacy wastewater discharge at Mithapur. This introduces an unquantified contingent liability that could disrupt future margin profiles.

2. Human Capital Operational Friction: Despite AI-driven automation efforts, the operational execution remains dangerously leveraged on contractual labor (89.1% of the blue-collar workforce). The recording of two worker fatalities in FY26, juxtaposed against an otherwise low TRIFR of 0.77, signals critical contractor-level vulnerabilities within the high-heat manufacturing supply chain.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant)

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."