Hindustan Zinc: Aggressive Capacity Expansion Near Rajasthan's Debari Complex as 54% EBITDA Margin Signals Extreme Free Cash Conversion

Date : 2026-06-09

Reading : 145

Hindustan Zinc’s FY2026 filings reveal an enterprise structurally engineered to outmaneuver global base-metal cyclicality through an integrated zero-cost silver by-product moat. By shifting 53% of its thermal load to domestic Indian coal and deploying AI-driven autonomous loaders across the Rajasthan Proterozoic belt, the firm compressed its zinc cost of production to a five-year low of $959/tonne. For institutional allocators, the defining dynamic is how a $1.95 billion capex cycle shields the asset from impending European CBAM tariffs, simultaneously funding massive parent-entity liquidity extractions without compromising its pristine net-cash standing.

Forensic Financials & Segmental Margin Architecture

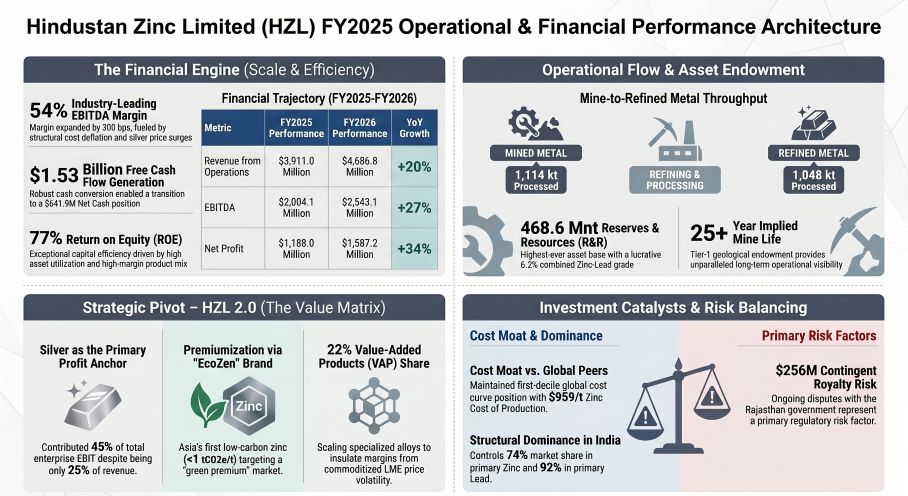

Hindustan Zinc (NSE: HINDZINC) operates at the absolute bottom of the global cost curve (first decile for smelting, first quartile for mining). The FY2026 income statement confirms robust operating leverage, driven heavily by cross-commodity subsidization from its precious metals portfolio.

Figure Hindustan Zinc Limited (HZL) FY2025 Operational & Financial Performance Architecture

Quantitative Financial Inventory (FY2026 vs FY2025):

Quantitative Financial Inventory (FY2026 vs FY2025):

* Top-Line Revenue: $4,686.8 million (up 20% YoY from $3,911.0 million).

* EBITDA: $2,543.1 million (up 27% YoY), translating to a ~300 bps margin expansion to 54%.

* Net Profit: $1,587.2 million (up 34% YoY).

* Pre-Growth Free Cash Flow (FCF): $1,530.4 million prior to green investments.

* Net Cash Position: $641.9 million, reversing a FY2025 net debt position of $140.45 million. Total gross cash equivalents rest at $1.58 billion.

DuPont Mechanics & The Silver Asymmetry:

The firm generated a staggering 77% Return on Equity (ROE) and 67% Return on Capital Employed (ROCE) against an estimated WACC of 14.0%. This extreme capital efficiency is anchored by its silver segment. While silver volumes contracted 9% YoY to 627 MT, surging LBMA spot prices elevated segmental revenue to $1,129.2 million. Crucially, silver now contributes ~45% of total enterprise EBIT ($961.3 million), acting as a massive zero-cost financial buffer.

Unit Economics & Cost Deflation:

Operating leverage was enhanced via AI-integrated chemical dosing (cutting consumable norms by 4%) and the deployment of the NYSE: CAT R2900 XE diesel-electric hybrid loader at the Rajpura Dariba Mine, which compressed fuel consumption by 24%.

Supply Chain Audit & Geo-Economic Moat

The physicality of NSE: HINDZINC is defined by unparalleled geographic density in the mineral-rich state of Rajasthan, eradicating inbound freight friction. The firm reported its highest-ever Ore Reserves and Mineral Resources (R&R) base of 468.6 million tonnes at a lucrative 6.2% base metal grade, underwriting an implied mine life exceeding 25 years.

Core Asset Footprint & Logistical Mitigation:

* The Rampura Agucha Mine (RAM): The world’s largest zinc-producing mine (576 kt mined metal) optimized margins via internal underground waste dumping, bypassing surface haulage energy requirements.

* Sindesar Khurd Mine (SKM): The world’s 6th largest silver asset integrated the world’s first tele-remote raise bore operation, sustaining production throughput during hazardous blasting fume clearance protocols.

* Smelting Integration: The Chanderiya Lead Zinc Smelter (CLZS) and Dariba Smelting Complex (DSC) executed high-return brownfield debottlenecking, amplifying hydrometallurgical cellhouse current from 200 kA to 212 kA, releasing an additional 21 ktpa of refined zinc capacity.

* Global Logistics Buffer: To counter US-Iran-Israel Red Sea disruptions, management aggressively scaled gross working capital to $328.4 million, establishing strategic domestic buffer inventories of explosives-grade ammonium nitrate and industrial diesel.

Green Logistics & CBAM Defense:

The firm’s Pantnagar Metal Plant operates on 100% green energy, supporting the commercialization of *EcoZen*—Asia’s first low-carbon zinc brand (<1 tCO2e/tonne). This secures a strategic pricing premium and defends European market share against the EU Carbon Border Adjustment Mechanism (CBAM). Energy transition is physically backed by a 530 MW round-the-clock power delivery agreement with Serentica Renewables, targeting a 70% renewable grid mix by 2028.

RPT Frictions & Off-Balance Sheet Litigations

While physical operations remain optimal, the balance sheet experiences severe structural outflows to its parent entity, Vedanta Limited (NSE: VEDL), which controls a 60.71% stake.

* Top-Line Parent Extraction: In FY2026, the firm paid its parent $134.37 million in "Strategic Services and Brand Fees"—a massive 78% YoY increase resulting from a contract renegotiation that escalated the fee from 2% to 3% of consolidated turnover.

* Capital Distributions: Total FY2026 dividend cash outflow was $484.8 million. The parent extracted $307.53 million, while the Government of India (27.92% stake) received $135.40 million.

* Contingent Liabilities: Off-balance-sheet risks remain heavily concentrated in contested tax positions. The most material is a $1,424.15 million Section 80IA/80IC tax holiday dispute pending before the Rajasthan High Court, alongside a $220.89 million royalty computation demand from the Department of Mines and Geology (DMG).

HDIN Institutional Perspective

While management frames the approved $1.95 billion Phase-1 capex cycle—earmarked for a 250 ktpa Debari smelter and a 10 Mtpa tailings reprocessing plant—as an autonomous growth trajectory, the underlying governance mechanics present a differentiated narrative. The mathematical reality is that NSE: HINDZINC functions as a highly fortified liquidity engine for its parent. The 3% top-line brand fee tax effectively transfers wealth to the promoter before distributable earnings reach the 11.37% public float. Furthermore, the Board's failure to maintain a 50% independent director ratio (incurring BSE/NSE compliance penalties) underscores a structural governance discount. LPs must price in the reality that while the physical geological moat is irreplicable, the enterprise's cash conversion is permanently tethered to the refinancing requirements of its holding company.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Forensic Financials & Segmental Margin Architecture

Hindustan Zinc (NSE: HINDZINC) operates at the absolute bottom of the global cost curve (first decile for smelting, first quartile for mining). The FY2026 income statement confirms robust operating leverage, driven heavily by cross-commodity subsidization from its precious metals portfolio.

Figure Hindustan Zinc Limited (HZL) FY2025 Operational & Financial Performance Architecture

Quantitative Financial Inventory (FY2026 vs FY2025):* Top-Line Revenue: $4,686.8 million (up 20% YoY from $3,911.0 million).

* EBITDA: $2,543.1 million (up 27% YoY), translating to a ~300 bps margin expansion to 54%.

* Net Profit: $1,587.2 million (up 34% YoY).

* Pre-Growth Free Cash Flow (FCF): $1,530.4 million prior to green investments.

* Net Cash Position: $641.9 million, reversing a FY2025 net debt position of $140.45 million. Total gross cash equivalents rest at $1.58 billion.

DuPont Mechanics & The Silver Asymmetry:

The firm generated a staggering 77% Return on Equity (ROE) and 67% Return on Capital Employed (ROCE) against an estimated WACC of 14.0%. This extreme capital efficiency is anchored by its silver segment. While silver volumes contracted 9% YoY to 627 MT, surging LBMA spot prices elevated segmental revenue to $1,129.2 million. Crucially, silver now contributes ~45% of total enterprise EBIT ($961.3 million), acting as a massive zero-cost financial buffer.

Unit Economics & Cost Deflation:

Operating leverage was enhanced via AI-integrated chemical dosing (cutting consumable norms by 4%) and the deployment of the NYSE: CAT R2900 XE diesel-electric hybrid loader at the Rajpura Dariba Mine, which compressed fuel consumption by 24%.

Supply Chain Audit & Geo-Economic Moat

The physicality of NSE: HINDZINC is defined by unparalleled geographic density in the mineral-rich state of Rajasthan, eradicating inbound freight friction. The firm reported its highest-ever Ore Reserves and Mineral Resources (R&R) base of 468.6 million tonnes at a lucrative 6.2% base metal grade, underwriting an implied mine life exceeding 25 years.

Core Asset Footprint & Logistical Mitigation:

* The Rampura Agucha Mine (RAM): The world’s largest zinc-producing mine (576 kt mined metal) optimized margins via internal underground waste dumping, bypassing surface haulage energy requirements.

* Sindesar Khurd Mine (SKM): The world’s 6th largest silver asset integrated the world’s first tele-remote raise bore operation, sustaining production throughput during hazardous blasting fume clearance protocols.

* Smelting Integration: The Chanderiya Lead Zinc Smelter (CLZS) and Dariba Smelting Complex (DSC) executed high-return brownfield debottlenecking, amplifying hydrometallurgical cellhouse current from 200 kA to 212 kA, releasing an additional 21 ktpa of refined zinc capacity.

* Global Logistics Buffer: To counter US-Iran-Israel Red Sea disruptions, management aggressively scaled gross working capital to $328.4 million, establishing strategic domestic buffer inventories of explosives-grade ammonium nitrate and industrial diesel.

Green Logistics & CBAM Defense:

The firm’s Pantnagar Metal Plant operates on 100% green energy, supporting the commercialization of *EcoZen*—Asia’s first low-carbon zinc brand (<1 tCO2e/tonne). This secures a strategic pricing premium and defends European market share against the EU Carbon Border Adjustment Mechanism (CBAM). Energy transition is physically backed by a 530 MW round-the-clock power delivery agreement with Serentica Renewables, targeting a 70% renewable grid mix by 2028.

RPT Frictions & Off-Balance Sheet Litigations

While physical operations remain optimal, the balance sheet experiences severe structural outflows to its parent entity, Vedanta Limited (NSE: VEDL), which controls a 60.71% stake.

* Top-Line Parent Extraction: In FY2026, the firm paid its parent $134.37 million in "Strategic Services and Brand Fees"—a massive 78% YoY increase resulting from a contract renegotiation that escalated the fee from 2% to 3% of consolidated turnover.

* Capital Distributions: Total FY2026 dividend cash outflow was $484.8 million. The parent extracted $307.53 million, while the Government of India (27.92% stake) received $135.40 million.

* Contingent Liabilities: Off-balance-sheet risks remain heavily concentrated in contested tax positions. The most material is a $1,424.15 million Section 80IA/80IC tax holiday dispute pending before the Rajasthan High Court, alongside a $220.89 million royalty computation demand from the Department of Mines and Geology (DMG).

HDIN Institutional Perspective

While management frames the approved $1.95 billion Phase-1 capex cycle—earmarked for a 250 ktpa Debari smelter and a 10 Mtpa tailings reprocessing plant—as an autonomous growth trajectory, the underlying governance mechanics present a differentiated narrative. The mathematical reality is that NSE: HINDZINC functions as a highly fortified liquidity engine for its parent. The 3% top-line brand fee tax effectively transfers wealth to the promoter before distributable earnings reach the 11.37% public float. Furthermore, the Board's failure to maintain a 50% independent director ratio (incurring BSE/NSE compliance penalties) underscores a structural governance discount. LPs must price in the reality that while the physical geological moat is irreplicable, the enterprise's cash conversion is permanently tethered to the refinancing requirements of its holding company.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."