D-Link Corporation: Supply Chain Decentralization Near India and Vietnam as Margin Compression Signals European Market Decay

Date : 2026-06-11

Reading : 207

D-Link’s FY2025 financial disclosures expose a classic value-trap profile: a highly liquid, un-levered balance sheet masking severe operational hemorrhage. As global telecommunications procurement fractures along geopolitical lines, the firm’s defensive pivot to a decentralized manufacturing footprint across India and Vietnam has safeguarded market access but structurally degraded gross margins to 24.6%. For institutional LPs, the critical focal point is the European subsidiary’s $15.55 million standalone investment loss, which triggered forced debt-to-equity conversions. This reveals how systemic price-war exposure continues to dilute the firm’s transition toward higher-margin AI cloud services.

Figure D-Link FY2025 Strategic Performance Review: Navigating Structural Friction & AloT Transformation

FY2025 Segmental Volatility and Operating De-leverage

FY2025 Segmental Volatility and Operating De-leverage

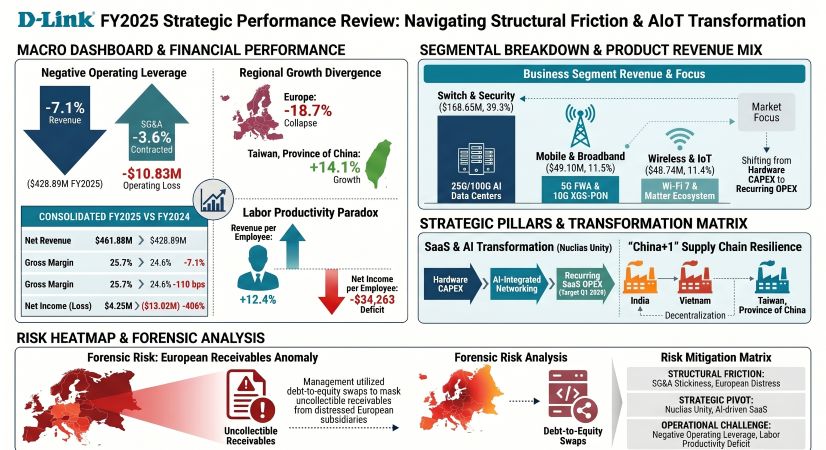

A forensic extraction of D-Link’s (TWSE: 2332) FY2025 financials reveals severe negative operating leverage. While consolidated top-line revenue contracted by 7.1%, management failed to rationalize fixed overhead proportionately. The resulting 110-bps gross margin contraction (from 25.7% to 24.6%) directly drove a 69% expansion in operating losses.

Consolidated Capital Inventory & Margin Dilution:

* Top-Line Contraction: Consolidated revenue fell to $428.89 million, triggering an 11% year-over-year (YoY) drop in gross profit to $105.50 million.

* Operating & Net Deficits: Operating losses widened to -$10.83 million. Net income collapsed by 406% YoY, swinging to a -$13.02 million loss (EPS: -$0.029). Operating cash flow turned negative, burning -$6.79 million.

* Capital Structure (Defensive Base): Total assets sit at $507.71 million against minimal liabilities of $162.68 million. The debt-to-asset ratio is exceptionally conservative at 32.0%, supported by a current ratio of 2.45x and an ending cash balance of $101.75 million. Due to accumulated deficits, the Board instituted a strict zero-dividend policy.

Segmental & Geographic Dispersion:

* Switch and Security (39.32% of Rev): Generated $168.65 million. The strategic pivot focuses heavily on the DQS-5000 25G/100G micro data center switches to capture generative AI infrastructure demand.

* Mobile/Broadband & Wireless/IoT (22.81% of Rev): Contributed $49.10 million and $48.74 million, respectively, driven by 5G Fixed Wireless Access (FWA) CPEs and Wi-Fi 7 (BE3600/BE9500) routers.

* Geographic Divergence: The Americas (+17.4% to $32.32 million) and Domestic Taiwan, Province of China (+14.1% to $23.90 million) exhibited counter-cyclical growth. Conversely, Europe suffered an 18.7% revenue collapse to $86.16 million. Asia/Others contracted 6.8% to $286.50 million.

Forensic Red Flags (Accounting Anomalies):

* European Receivables Capitalization: In Q1/Q2 2025, accounts receivable from the European subsidiary overdue by >3 months were temporarily classified as "loans to others." By Q3, this accounting treatment failed, forcing the Board to swap the uncollectible debt into equity, burying a severe cash-collection failure inside the balance sheet.

* Tax Asymmetry: The firm recognized an income tax expense of $6.90 million despite a consolidated pre-tax net loss of -$6.11 million, indicating an inability to utilize Deferred Tax Assets (DTAs) across jurisdictional boundaries.

* FX Volatility: The company absorbed a negative -$3.97 million swing in foreign exchange losses due to the appreciation of the TWD against the USD.

Supply Chain Audit & Geo-Economic Moat

To insulate its operations from shifting U.S. tariff policies and semiconductor supply chain blockades, TWSE: 2332 is heavily modifying its physical production architecture.

* The "China+1" Physical Footprint: The firm is actively bypassing centralized dependence on mainland China by deploying turnkey assembly capabilities across Taiwan, Province of China, India, and Vietnam. This satisfies stringent "Made in Local" telecom procurement mandates but structurally sacrifices hyper-scale cost efficiencies, pressuring gross margins.

* Subsidiary Manufacturing Hub: Upstream hardware production is largely localized through Cameo Communications, Inc. (41.58% stake, $4.41 million investment). Cameo operates the core Surface-Mount Technology (SMT) and Dual In-Line Package (DIP) assembly lines for legacy and advanced optical network switches.

* Procurement Concentration: Forensic data contradicts management’s claim of a fully diversified vendor base. Exactly 36% of all raw material purchases ($114.26 million out of a $322.37 million total) are highly concentrated among just three anonymous suppliers (Company I: 14%, Company J: 12%, Company AD: 10%), creating a tangible midstream supply bottleneck.

HDIN Institutional Perspective: The SaaS Transition vs. Hardware Deflation

While the corporate narrative champions a margin-accretive shift to Software-as-a-Service (SaaS) via the Q1 2026 launch of the Nuclias Unity converged cloud platform, forensic modeling of the firm’s FY2025 cost structure suggests a traditional hardware entity struggling with severe deflationary unit economics.

The Execution Credibility Gap: Management aggressively slashed headcount by 17.4% (from 460 to 380, and down to 354 by Q1 2026). This artificially inflated top-line productivity (Revenue per Employee increased 12.4% to $1.128 million). However, the actual SG&A expenditure proved highly inelastic, contracting a mere 3.6% YoY. Consequently, bottom-line labor productivity cratered from a profit of +$9,239 per capita in FY2024 to a deficit of -$34,263 in FY2025.

The Verdict: The capital reallocation toward AI-driven Nuclias Unity, D-View8, and mydlink recurring-revenue ecosystems is structurally correct. Consolidated R&D dropped 22% to $19.01 million as legacy hardware R&D was deliberately starved. Yet, until TWSE: 2332 can aggressively deflate its sticky European administrative overhead and prove enterprise subscription conversion rates, institutional investors should anticipate prolonged margin suppression driven by Chinese retail hardware commoditization.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure D-Link FY2025 Strategic Performance Review: Navigating Structural Friction & AloT Transformation

FY2025 Segmental Volatility and Operating De-leverageA forensic extraction of D-Link’s (TWSE: 2332) FY2025 financials reveals severe negative operating leverage. While consolidated top-line revenue contracted by 7.1%, management failed to rationalize fixed overhead proportionately. The resulting 110-bps gross margin contraction (from 25.7% to 24.6%) directly drove a 69% expansion in operating losses.

Consolidated Capital Inventory & Margin Dilution:

* Top-Line Contraction: Consolidated revenue fell to $428.89 million, triggering an 11% year-over-year (YoY) drop in gross profit to $105.50 million.

* Operating & Net Deficits: Operating losses widened to -$10.83 million. Net income collapsed by 406% YoY, swinging to a -$13.02 million loss (EPS: -$0.029). Operating cash flow turned negative, burning -$6.79 million.

* Capital Structure (Defensive Base): Total assets sit at $507.71 million against minimal liabilities of $162.68 million. The debt-to-asset ratio is exceptionally conservative at 32.0%, supported by a current ratio of 2.45x and an ending cash balance of $101.75 million. Due to accumulated deficits, the Board instituted a strict zero-dividend policy.

Segmental & Geographic Dispersion:

* Switch and Security (39.32% of Rev): Generated $168.65 million. The strategic pivot focuses heavily on the DQS-5000 25G/100G micro data center switches to capture generative AI infrastructure demand.

* Mobile/Broadband & Wireless/IoT (22.81% of Rev): Contributed $49.10 million and $48.74 million, respectively, driven by 5G Fixed Wireless Access (FWA) CPEs and Wi-Fi 7 (BE3600/BE9500) routers.

* Geographic Divergence: The Americas (+17.4% to $32.32 million) and Domestic Taiwan, Province of China (+14.1% to $23.90 million) exhibited counter-cyclical growth. Conversely, Europe suffered an 18.7% revenue collapse to $86.16 million. Asia/Others contracted 6.8% to $286.50 million.

Forensic Red Flags (Accounting Anomalies):

* European Receivables Capitalization: In Q1/Q2 2025, accounts receivable from the European subsidiary overdue by >3 months were temporarily classified as "loans to others." By Q3, this accounting treatment failed, forcing the Board to swap the uncollectible debt into equity, burying a severe cash-collection failure inside the balance sheet.

* Tax Asymmetry: The firm recognized an income tax expense of $6.90 million despite a consolidated pre-tax net loss of -$6.11 million, indicating an inability to utilize Deferred Tax Assets (DTAs) across jurisdictional boundaries.

* FX Volatility: The company absorbed a negative -$3.97 million swing in foreign exchange losses due to the appreciation of the TWD against the USD.

Supply Chain Audit & Geo-Economic Moat

To insulate its operations from shifting U.S. tariff policies and semiconductor supply chain blockades, TWSE: 2332 is heavily modifying its physical production architecture.

* The "China+1" Physical Footprint: The firm is actively bypassing centralized dependence on mainland China by deploying turnkey assembly capabilities across Taiwan, Province of China, India, and Vietnam. This satisfies stringent "Made in Local" telecom procurement mandates but structurally sacrifices hyper-scale cost efficiencies, pressuring gross margins.

* Subsidiary Manufacturing Hub: Upstream hardware production is largely localized through Cameo Communications, Inc. (41.58% stake, $4.41 million investment). Cameo operates the core Surface-Mount Technology (SMT) and Dual In-Line Package (DIP) assembly lines for legacy and advanced optical network switches.

* Procurement Concentration: Forensic data contradicts management’s claim of a fully diversified vendor base. Exactly 36% of all raw material purchases ($114.26 million out of a $322.37 million total) are highly concentrated among just three anonymous suppliers (Company I: 14%, Company J: 12%, Company AD: 10%), creating a tangible midstream supply bottleneck.

HDIN Institutional Perspective: The SaaS Transition vs. Hardware Deflation

While the corporate narrative champions a margin-accretive shift to Software-as-a-Service (SaaS) via the Q1 2026 launch of the Nuclias Unity converged cloud platform, forensic modeling of the firm’s FY2025 cost structure suggests a traditional hardware entity struggling with severe deflationary unit economics.

The Execution Credibility Gap: Management aggressively slashed headcount by 17.4% (from 460 to 380, and down to 354 by Q1 2026). This artificially inflated top-line productivity (Revenue per Employee increased 12.4% to $1.128 million). However, the actual SG&A expenditure proved highly inelastic, contracting a mere 3.6% YoY. Consequently, bottom-line labor productivity cratered from a profit of +$9,239 per capita in FY2024 to a deficit of -$34,263 in FY2025.

The Verdict: The capital reallocation toward AI-driven Nuclias Unity, D-View8, and mydlink recurring-revenue ecosystems is structurally correct. Consolidated R&D dropped 22% to $19.01 million as legacy hardware R&D was deliberately starved. Yet, until TWSE: 2332 can aggressively deflate its sticky European administrative overhead and prove enterprise subscription conversion rates, institutional investors should anticipate prolonged margin suppression driven by Chinese retail hardware commoditization.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."