Tokai Rika: Mechatronic Pivot Near Oguchi Hub as 18 bps Margin Compression Signals Mechanical Asset Obsolescence

Date : 2026-06-11

Reading : 139

Tokai Rika’s FY2026 disclosures reveal a dual-track reality: while pricing power over OEM clients delivered a 78.1% operating profit beat against initial guidance, underlying metrics expose operational friction. An 18 bps margin compression and a $21.5 million impairment charge in its Japan operations highlight the structural obsolescence of mechanical hardware. For institutional capital, the firm’s aggressive R&D pivot towards mechatronic interfaces and the liquidation of $171.2 million in legacy cross-shareholdings signify an urgent, zero-sum transition to defend its Tier-1 moat amid the software-defined vehicle era.

Figure Tokai Rika Co Ltd: 2025-2026 Strategic Profile & Operational Analysis

Segmental Incremental Margins & Capital Allocation

Segmental Incremental Margins & Capital Allocation

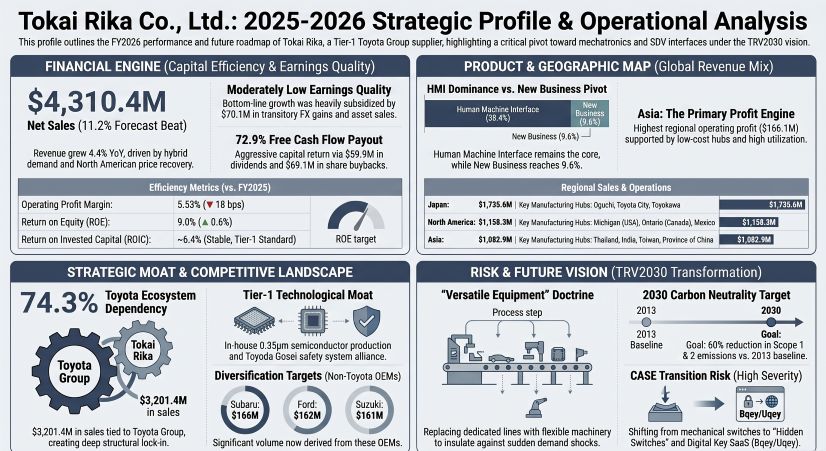

A forensic examination of Tokai Rika’s FY2026 financials indicates a structurally highly capitalized balance sheet, albeit with bottom-line expansion subsidized by transitory non-operating tailwinds. Despite Net Sales expanding 4.4% YoY to $4,310.4 million, core Operating Profit (OP) remained virtually flat at $238.2 million (+1.0%), leading to an operating margin compression from 5.71% to 5.53%.

* P&L & Free Cash Flow Conversion: Operating Cash Flow increased by 11.6% to $292.5 million. FCF achieved a 100% YoY expansion to $176.9 million, granting the firm liquidity to execute a shareholder-accretive return policy. Total capital returned ($129.0 million, via $59.9 million in dividends and $69.1 million in buybacks) consumed 72.9% of generated FCF.

* Structural Efficiency & Internal Capital Allocation:

* ROIC vs. Cost of Capital: Estimated ROIC stands at ~6.4% (NOPAT: ~$164.4 million; Invested Capital: $2,564.6 million). While Return on Equity (ROE) expanded to 9.0%, the relatively narrow ROIC spread underscores the drag of domestic fixed costs.

* Cash Conversion Cycle (CCC): Stabilized at ~72.8 days (DSO: 54.2, DIO: 54.8, DPO: 36.2). Elevated Days Inventory Outstanding is an intentional structural buffer to stockpile electronic components against systemic supply chain fragility.

* R&D Reinvestment: $230.1 million (5.34% of Net Sales) allocated heavily into the Japan segment ($224.1 million) to commercialize CASE-compliant tech, specifically the Hidden Switch platform, Shift-by-Wire systems, and proprietary 0.35μm semiconductors.

* Earnings Quality Audit & Compliance Constraints: The 13.1% Net Profit growth ($197.0 million) masks underlying structural weakness. Pre-tax profitability was significantly inflated by $70.1 million in transitory items: a $30.7 million foreign exchange gain and $39.4 million from liquidating legacy cross-shareholdings (including positions in TYO: 6902 Denso and TYO: 7270 Subaru). Additionally, an independent auditor flagged a material weakness regarding a five-year retroactive restatement over tax-effect accounting, signaling ineffective internal controls. The firm also booked a $21.5 million impairment primarily targeting machinery and building assets in Japan, validating the rapid stranding of mechanical switchgear assets.

Keiretsu Captivity and Hyper-Localized Manufacturing Agility

Tokai Rika operates a highly insulated, "build-where-we-sell" manufacturing matrix designed to mitigate cross-border tariff risks, yet it remains heavily shackled to a single automotive ecosystem.

* Customer Concentration & Pricing Leverage: The firm fundamentally operates as a keiretsu-aligned extension, generating 74.3% of its global sales ($3,201.4 million) from the TYO: 7203 Toyota Group. Despite this captive dynamic, Tokai Rika demonstrated absolute contractual leverage in FY2026, passing through raw material inflation downstream to over-deliver on initial OP forecasts by $104.5 million. Diversification efforts with NYSE: F Ford ($162.5 million) and TYO: 7269 Suzuki ($161.3 million) remain structurally insufficient to cushion a primary OEM demand shock.

* Geographic Production Economics:

* Japan (Headquarters): Spanning the Oguchi, Toyota City, and Toyokawa hubs, this segment generated $1,735.6 million in external sales but suffered a widening operating loss of -$9.5 million due to R&D overhead and legacy capacity realignment.

* North America: The TRAM/TAC Manufacturing/TRMI (Michigan, USA) and Tokai Rika Mexico facilities generated $1,158.3 million in sales and $55.2 million in OP. This region led the successful cost-pass-through execution.

* Asia (The Cash Engine): Operating out of hubs including Rika Kogyo Co., Ltd. (Taoyuan City, Taiwan, Province of China), alongside mainland China and Thailand nodes, Asia generated $1,082.9 million in external sales and an outsized $166.1 million in OP, capitalizing on lower labor costs and high plant utilization.

* Manufacturing Agility (Versatile Equipment): To prevent future $21.5 million asset impairments, the firm is dismantling dedicated mechanical assembly lines. The integration of "versatile equipment" ensures that high-mix, variable-volume mechatronic components can be scaled on standardized transport processes without incurring stranded asset risks.

HDIN Institutional Perspective

While the Street may applaud the 13.1% bottom-line expansion and aggressive capital returns, our forensic analysis challenges the sustainability of Tokai Rika's core valuation. The $70.1 million in FX and hidden-asset liquidation gains effectively subsidized a bleeding domestic manufacturing base. The company possesses immense pricing power and deep ecosystem captivity within Toyota, but its ultimate equity narrative hinges entirely on the commercial scaling of high-margin mechatronics (like the Hidden Switch and UWB radar) and SaaS fleet platforms (Bqey / Uqey). Until these software-defined products eclipse the $1,255.4 million tied to legacy mechanical shift levers and seatbelts, the firm remains vulnerable to margin degradation from internal fixed costs and structural asset obsolescence.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Tokai Rika Co Ltd: 2025-2026 Strategic Profile & Operational Analysis

Segmental Incremental Margins & Capital AllocationA forensic examination of Tokai Rika’s FY2026 financials indicates a structurally highly capitalized balance sheet, albeit with bottom-line expansion subsidized by transitory non-operating tailwinds. Despite Net Sales expanding 4.4% YoY to $4,310.4 million, core Operating Profit (OP) remained virtually flat at $238.2 million (+1.0%), leading to an operating margin compression from 5.71% to 5.53%.

* P&L & Free Cash Flow Conversion: Operating Cash Flow increased by 11.6% to $292.5 million. FCF achieved a 100% YoY expansion to $176.9 million, granting the firm liquidity to execute a shareholder-accretive return policy. Total capital returned ($129.0 million, via $59.9 million in dividends and $69.1 million in buybacks) consumed 72.9% of generated FCF.

* Structural Efficiency & Internal Capital Allocation:

* ROIC vs. Cost of Capital: Estimated ROIC stands at ~6.4% (NOPAT: ~$164.4 million; Invested Capital: $2,564.6 million). While Return on Equity (ROE) expanded to 9.0%, the relatively narrow ROIC spread underscores the drag of domestic fixed costs.

* Cash Conversion Cycle (CCC): Stabilized at ~72.8 days (DSO: 54.2, DIO: 54.8, DPO: 36.2). Elevated Days Inventory Outstanding is an intentional structural buffer to stockpile electronic components against systemic supply chain fragility.

* R&D Reinvestment: $230.1 million (5.34% of Net Sales) allocated heavily into the Japan segment ($224.1 million) to commercialize CASE-compliant tech, specifically the Hidden Switch platform, Shift-by-Wire systems, and proprietary 0.35μm semiconductors.

* Earnings Quality Audit & Compliance Constraints: The 13.1% Net Profit growth ($197.0 million) masks underlying structural weakness. Pre-tax profitability was significantly inflated by $70.1 million in transitory items: a $30.7 million foreign exchange gain and $39.4 million from liquidating legacy cross-shareholdings (including positions in TYO: 6902 Denso and TYO: 7270 Subaru). Additionally, an independent auditor flagged a material weakness regarding a five-year retroactive restatement over tax-effect accounting, signaling ineffective internal controls. The firm also booked a $21.5 million impairment primarily targeting machinery and building assets in Japan, validating the rapid stranding of mechanical switchgear assets.

Keiretsu Captivity and Hyper-Localized Manufacturing Agility

Tokai Rika operates a highly insulated, "build-where-we-sell" manufacturing matrix designed to mitigate cross-border tariff risks, yet it remains heavily shackled to a single automotive ecosystem.

* Customer Concentration & Pricing Leverage: The firm fundamentally operates as a keiretsu-aligned extension, generating 74.3% of its global sales ($3,201.4 million) from the TYO: 7203 Toyota Group. Despite this captive dynamic, Tokai Rika demonstrated absolute contractual leverage in FY2026, passing through raw material inflation downstream to over-deliver on initial OP forecasts by $104.5 million. Diversification efforts with NYSE: F Ford ($162.5 million) and TYO: 7269 Suzuki ($161.3 million) remain structurally insufficient to cushion a primary OEM demand shock.

* Geographic Production Economics:

* Japan (Headquarters): Spanning the Oguchi, Toyota City, and Toyokawa hubs, this segment generated $1,735.6 million in external sales but suffered a widening operating loss of -$9.5 million due to R&D overhead and legacy capacity realignment.

* North America: The TRAM/TAC Manufacturing/TRMI (Michigan, USA) and Tokai Rika Mexico facilities generated $1,158.3 million in sales and $55.2 million in OP. This region led the successful cost-pass-through execution.

* Asia (The Cash Engine): Operating out of hubs including Rika Kogyo Co., Ltd. (Taoyuan City, Taiwan, Province of China), alongside mainland China and Thailand nodes, Asia generated $1,082.9 million in external sales and an outsized $166.1 million in OP, capitalizing on lower labor costs and high plant utilization.

* Manufacturing Agility (Versatile Equipment): To prevent future $21.5 million asset impairments, the firm is dismantling dedicated mechanical assembly lines. The integration of "versatile equipment" ensures that high-mix, variable-volume mechatronic components can be scaled on standardized transport processes without incurring stranded asset risks.

HDIN Institutional Perspective

While the Street may applaud the 13.1% bottom-line expansion and aggressive capital returns, our forensic analysis challenges the sustainability of Tokai Rika's core valuation. The $70.1 million in FX and hidden-asset liquidation gains effectively subsidized a bleeding domestic manufacturing base. The company possesses immense pricing power and deep ecosystem captivity within Toyota, but its ultimate equity narrative hinges entirely on the commercial scaling of high-margin mechatronics (like the Hidden Switch and UWB radar) and SaaS fleet platforms (Bqey / Uqey). Until these software-defined products eclipse the $1,255.4 million tied to legacy mechanical shift levers and seatbelts, the firm remains vulnerable to margin degradation from internal fixed costs and structural asset obsolescence.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."