Toyota Boshoku: BEV Resource Reallocation Near Americas and Greater China Hubs as $504.78 Million Capex Signals Structural Margin Recovery

Date : 2026-06-11

Reading : 198

Toyota Boshoku's FY2026 disclosures expose a highly localized capital strategy responding to severe climate transition risks. Facing margin compression from carbon pricing and material inflation, the Keiretsu-aligned Tier-1 supplier is actively shifting from legacy hardware to Software-Defined Vehicle (SDV) architectures. While a massive $183.29 million restructuring provision depresses stated operating profit, the underlying 4.2% top-line recovery confirms demand resilience. For institutional LPs, the firm's $504.78 million capital expenditure and localized procurement model signal a strategic willingness to trade near-term asset turnover for a fortified, decarbonized moat.

Figure Toyota Boshoku Strategic Diagnostic: FY2026 Performance & 2030 Mobility Transformation

Forensic Financials & Segmental Inventory

Forensic Financials & Segmental Inventory

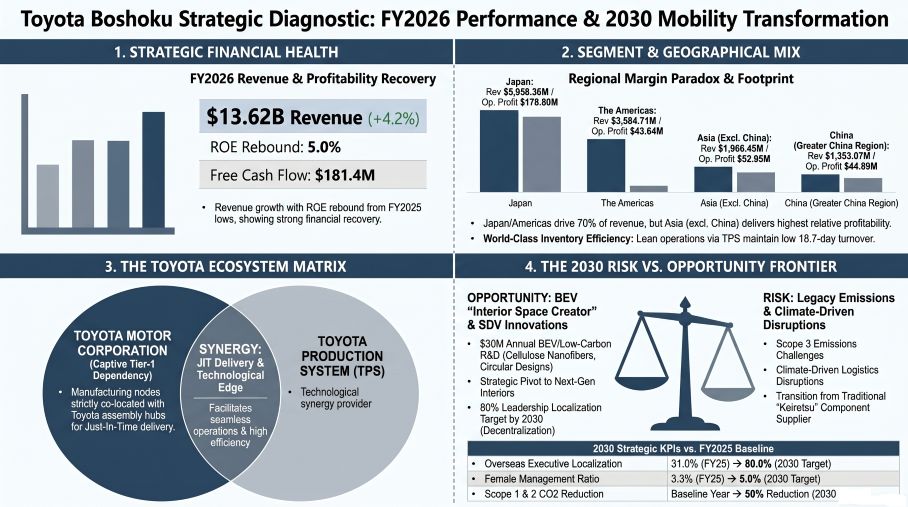

A forensic analysis of the FY2025 and FY2026 IFRS financial statements reveals significant "below-the-line" noise that distorts the underlying operational run-rate. The firm operates an inherently asset-heavy model, with Property, Plant, and Equipment (PP&E) continuously consuming ~29% of total assets ($2,309.20 million in FY2026).

* Top-Line & Operating Leverage: Revenue expanded 4.2% YoY in FY2026 to $13,619.60 million. Operating Profit (OP) recovered to $413.98 million (3.04% margin), up from the FY2025 trough of $314.88 million (2.41% margin). COGS remains critically high at 89.8% ($12,232.90 million), leaving a narrow gross margin heavily exposed to raw material volatility. SG&A demonstrates hyper-lean overhead at just 7.44% ($1,013.11 million), driven by the Toyota Production System (TPS).

* Segmental OP Disconnect: Japan dominates the top line ($5,958.36 million) generating $178.80 million in OP. However, Asia (excluding China) generated the highest relative profitability outside the home market, posting $52.95 million in OP on just $1,906.45 million in revenue. The Americas footprint contributed $3,594.71 million in revenue and $43.64 million in OP.

* Earnings Quality Distortions: The FY2026 reported OP is heavily penalized by a $183.29 million Business Restructuring Loss, overshadowing a $26.40 million asset impairment hit. Conversely, net income was marginally propped up by $5.01 million in government subsidies and $13.97 million from fixed asset sales.

* Capital Returns & FCF Conversion: Despite the margin squeeze, Free Cash Flow (FCF) converted strongly, scaling from $43.98 million in FY2025 to $181.46 million in FY2026, supported by $504.78 million in operating cash flow. Management defended equity yields by maintaining a $0.57 absolute dividend, resulting in a 43.9% payout ratio and exceeding their initial 3.3% Return on Equity (ROE) target to reach 5.0%.

* Currency & Intangible Overhang: Net equity growth is currently inflated by a massive $102.72 million foreign exchange translation adjustment (OCI) due to the weak Yen, while direct derivative FX hedging sits at an immaterial $0.63 million. Additionally, Goodwill and Intangibles spiked 53.3% to $196.76 million following strategic venture injections into startups like Synspective and WALL.

Supply Chain Audit & Localized Geo-Economic Moat

To insulate its Just-In-Time (JIT) architecture from physical climate threats (4℃ scenario severe weather) and geopolitical logistics severances, Toyota Boshoku executes a rigid "local production for local consumption" footprint. The strategy mathematically limits cross-border Scope 3 transportation emissions while defending the 18.7-day inventory turnover cycle.

* Manufacturing Physicality: The domestic core relies on Toyota Boshoku Tohoku and Tokai Kasei Kogyo. The Americas footprint is structurally tethered to NYSE: TM assembly lines via Toyota Boshoku Indiana (LLC) and Toyota Boshoku Western Kentucky (LLC). The Greater China network utilizes localized joint ventures, heavily relying on Tianjin Intex Auto Parts and Guangzhou Sakura Auto Parts, while EMEA is anchored by tier-1 facilities in Turkey, Poland, and South Africa via Toyota Boshoku Europe.

* Carbon Liability & Procurement Squeeze: The firm is actively mitigating a massive 12,500,541 t-CO2e Scope 3 emissions overhang. Anticipating aggressive carbon pricing, management injected $6.69 million into an Internal Carbon Pricing (ICP) mechanism and deployed $20.73 million to optimize localized logistics routes.

* Proprietary R&D Transition: To address EV range sensitivity, R&D capital ($304.35 million in FY2026) is explicitly decoupling from internal combustion components. The firm allocated $18.05 million strictly to BEV/SDV product planning, alongside $12.03 million engineered in partnership with NEDO to commercialize Cellulose Nanofiber (CNF)—a decarbonized, plant-derived material critical for their "Parts to Parts" circular recycling mandate.

HDIN Institutional Perspective

While management's 2030 Vision promotes a high-margin "Interior Space Creator" narrative, the 53.3% spike in capitalized Goodwill combined with a $183.29 million restructuring provision suggests a highly friction-laden transition that the Street hasn't fully priced in. Toyota Boshoku is aggressively acquiring software-adjacent equity and reskilling traditional mechanical engineers to capture SDV market share. However, because the firm lacks independent, open-market pricing power and operates within a Keiretsu "Value Analysis" cost-down environment, we assess that the $504.78 million in elevated capex will likely defend their captive tier-one status rather than structurally expand operating margins beyond the historical 3.5% ceiling.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

Figure Toyota Boshoku Strategic Diagnostic: FY2026 Performance & 2030 Mobility Transformation

Forensic Financials & Segmental InventoryA forensic analysis of the FY2025 and FY2026 IFRS financial statements reveals significant "below-the-line" noise that distorts the underlying operational run-rate. The firm operates an inherently asset-heavy model, with Property, Plant, and Equipment (PP&E) continuously consuming ~29% of total assets ($2,309.20 million in FY2026).

* Top-Line & Operating Leverage: Revenue expanded 4.2% YoY in FY2026 to $13,619.60 million. Operating Profit (OP) recovered to $413.98 million (3.04% margin), up from the FY2025 trough of $314.88 million (2.41% margin). COGS remains critically high at 89.8% ($12,232.90 million), leaving a narrow gross margin heavily exposed to raw material volatility. SG&A demonstrates hyper-lean overhead at just 7.44% ($1,013.11 million), driven by the Toyota Production System (TPS).

* Segmental OP Disconnect: Japan dominates the top line ($5,958.36 million) generating $178.80 million in OP. However, Asia (excluding China) generated the highest relative profitability outside the home market, posting $52.95 million in OP on just $1,906.45 million in revenue. The Americas footprint contributed $3,594.71 million in revenue and $43.64 million in OP.

* Earnings Quality Distortions: The FY2026 reported OP is heavily penalized by a $183.29 million Business Restructuring Loss, overshadowing a $26.40 million asset impairment hit. Conversely, net income was marginally propped up by $5.01 million in government subsidies and $13.97 million from fixed asset sales.

* Capital Returns & FCF Conversion: Despite the margin squeeze, Free Cash Flow (FCF) converted strongly, scaling from $43.98 million in FY2025 to $181.46 million in FY2026, supported by $504.78 million in operating cash flow. Management defended equity yields by maintaining a $0.57 absolute dividend, resulting in a 43.9% payout ratio and exceeding their initial 3.3% Return on Equity (ROE) target to reach 5.0%.

* Currency & Intangible Overhang: Net equity growth is currently inflated by a massive $102.72 million foreign exchange translation adjustment (OCI) due to the weak Yen, while direct derivative FX hedging sits at an immaterial $0.63 million. Additionally, Goodwill and Intangibles spiked 53.3% to $196.76 million following strategic venture injections into startups like Synspective and WALL.

Supply Chain Audit & Localized Geo-Economic Moat

To insulate its Just-In-Time (JIT) architecture from physical climate threats (4℃ scenario severe weather) and geopolitical logistics severances, Toyota Boshoku executes a rigid "local production for local consumption" footprint. The strategy mathematically limits cross-border Scope 3 transportation emissions while defending the 18.7-day inventory turnover cycle.

* Manufacturing Physicality: The domestic core relies on Toyota Boshoku Tohoku and Tokai Kasei Kogyo. The Americas footprint is structurally tethered to NYSE: TM assembly lines via Toyota Boshoku Indiana (LLC) and Toyota Boshoku Western Kentucky (LLC). The Greater China network utilizes localized joint ventures, heavily relying on Tianjin Intex Auto Parts and Guangzhou Sakura Auto Parts, while EMEA is anchored by tier-1 facilities in Turkey, Poland, and South Africa via Toyota Boshoku Europe.

* Carbon Liability & Procurement Squeeze: The firm is actively mitigating a massive 12,500,541 t-CO2e Scope 3 emissions overhang. Anticipating aggressive carbon pricing, management injected $6.69 million into an Internal Carbon Pricing (ICP) mechanism and deployed $20.73 million to optimize localized logistics routes.

* Proprietary R&D Transition: To address EV range sensitivity, R&D capital ($304.35 million in FY2026) is explicitly decoupling from internal combustion components. The firm allocated $18.05 million strictly to BEV/SDV product planning, alongside $12.03 million engineered in partnership with NEDO to commercialize Cellulose Nanofiber (CNF)—a decarbonized, plant-derived material critical for their "Parts to Parts" circular recycling mandate.

HDIN Institutional Perspective

While management's 2030 Vision promotes a high-margin "Interior Space Creator" narrative, the 53.3% spike in capitalized Goodwill combined with a $183.29 million restructuring provision suggests a highly friction-laden transition that the Street hasn't fully priced in. Toyota Boshoku is aggressively acquiring software-adjacent equity and reskilling traditional mechanical engineers to capture SDV market share. However, because the firm lacks independent, open-market pricing power and operates within a Keiretsu "Value Analysis" cost-down environment, we assess that the $504.78 million in elevated capex will likely defend their captive tier-one status rather than structurally expand operating margins beyond the historical 3.5% ceiling.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*