Photocure: OPEX Equipment Pivot Near Princeton U.S. Base as 8.3% Core Revenue Growth Signals Self-Sustaining Operating Leverage

Date : 2026-06-11

Reading : 98

By substituting hospital CAPEX constraints with an OPEX-driven mobile tower model, Photocure (OSL: PHO) achieved a 22% surge in U.S. active accounts in 2025. With its composition-of-matter patents expired, the firm’s reliance on third-party OEMs like Karl Storz presents acute hardware bottleneck risks. However, a slated H2 2026 FDA Class II down-classification will drastically lower entry barriers for competing imaging towers. For institutional LPs, the transition from milestone-dependency to a self-funding $3.05M operating cash flow profile signals a highly de-risked, capital-light commercial phase.

Figure Photocure ASA 2025: Transitioning to a Self-Sustaining Commercial Engine

Price-Mix Variance & Margin Translation

Price-Mix Variance & Margin Translation

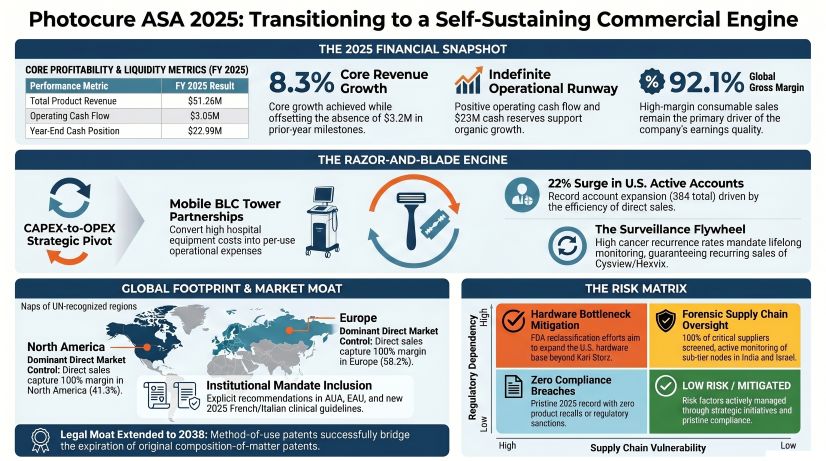

Photocure is executing a textbook structural transition from a milestone-subsidized biotech to a pure-play, commercially self-sustaining pharmaceutical entity. Stripping out the non-recurring $3.24M milestone injection from Asieris recognized in 2024, the underlying commercial franchise generated distinct positive operating leverage in FY 2025.

Quantitative Inventory (FY 2025 vs. FY 2024):

* Total Revenue: $51.26M vs. $50.57M (Core product sales +8.3% YoY adjusted for zero 2025 milestones).

* Hexvix/Cysview Franchise: $51.02M (99.5% of total revenue).

* Regional Top-Line: Europe: $29.82M (+8% YoY); North America: $21.17M (+9% YoY).

* Gross Margin: 92.1% (vs. 94.1% in 2024).

* EBITDA: $2.76M (Burdened by $1.67M in non-recurring M&A exploratory expenses).

* Operating Cash Flow (OCF): $3.05M.

* Internal Capital Allocation: $2.86M allocated to discretionary share buybacks; $3.91M allocated to Ipsen earnout liabilities (remaining non-current liability: $9.63M).

* Balance Sheet Liquidity: Cash and short-term deposits stood at $22.99M, providing an indefinite operational runway without the need for external equity financing.

* Unit Economics & Price-Mix Analysis: The company is asserting definitive pricing power. While global in-market unit volumes grew by 5% YoY, top-line revenue expanded by 8-9% regionally. This delta explicitly highlights aggressive Average Selling Price (ASP) hikes executed across both the U.S. and European segments to combat macroeconomic inflation. R&D capital intensity remains virtually nonexistent at 0.08% of revenue, as Phase III pipeline costs (Cevira) are fully outsourced to out-licensing partner Asieris, preparing for a $13M milestone catalyst in Q1 2026 upon Chinese and European regulatory progress.

CMO Dependency & Geopolitical Node Audits

Photocure operates an extreme asset-light, 100% outsourced operational footprint. While this shields the balance sheet from manufacturing CAPEX, it introduces specialized third-party dependencies requiring rigorous mapping.

* Geographic Corporate Footprint: Management operates from the BREEAM-certified "Very Good" Global Headquarters in Oslo, Norway, alongside primary commercial hubs in Princeton, New Jersey, and Germany.

* Tier-1 CMO Network: Finished and semi-finished manufacturing is concentrated strictly within Western Europe across critical facilities in Italy, Spain, the Netherlands, and Austria.

* Sub-Tier Vulnerability & Resource Constraints: A 2025 supply chain audit mapping 22 subcontractors flagged specific medium-risk nodes. Three upstream nodes in India supply raw materials to the primary Spanish aggregator, presenting structural labor risk. Additionally, one node near Tel Aviv, Israel, introduces potential geopolitical and water-scarcity disruptions. The firm currently utilizes standard UN Global Compact adherence to manage these sub-tier ESG exposures, reporting zero compliance breaches in 2025.

* The Hardware Ecosystem (The Physical Bottleneck): The firm’s highest vulnerability is U.S. hardware compatibility. Currently, Karl Storz holds a monopoly on FDA-approved equipment for the Cysview agent. To bypass hospital hardware purchasing freezes, Photocure aggressively pivoted to an OPEX model with ForTec Medical, deploying 24 mobile BLC Saphira towers in the U.S. (driving 11% of the U.S. business). In Europe, hardware agnosticism is accelerating via 60 high-definition Visera Elite III system placements with Olympus, and a targeted 2027 global launch of next-generation 4K flexible scopes co-developed with Richard Wolf.

HDIN Institutional Perspective

While Photocure emphasizes its "asset-light" manufacturing model, the 100% reliance on third-party hardware manufacturers exposes a severe single-point-of-failure. The firm's $51.02M diagnostic consumable franchise has historically been held hostage by Karl Storz’s equipment lifecycle in the U.S. market. However, the Street is fundamentally underpricing the structural margin expansion imminent from two primary regulatory catalysts: the proposed August 2026 CMS reimbursement decoupling and the pending FDA Class II equipment downgrade scheduled for H2 2026.

We view the FDA down-classification as the definitive value driver. This regulatory arbitrage will break the Karl Storz monopoly, effectively commoditizing the hardware "razor" and accelerating high-margin "blade" consumption across alternative OEMs. Coupled with an impenetrable method-of-use patent thicket locking down exclusivity until December 2036 and January 2038, the company has transformed its economic moat from chemical composition to institutional workflow integration.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant)*:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Photocure ASA 2025: Transitioning to a Self-Sustaining Commercial Engine

Price-Mix Variance & Margin TranslationPhotocure is executing a textbook structural transition from a milestone-subsidized biotech to a pure-play, commercially self-sustaining pharmaceutical entity. Stripping out the non-recurring $3.24M milestone injection from Asieris recognized in 2024, the underlying commercial franchise generated distinct positive operating leverage in FY 2025.

Quantitative Inventory (FY 2025 vs. FY 2024):

* Total Revenue: $51.26M vs. $50.57M (Core product sales +8.3% YoY adjusted for zero 2025 milestones).

* Hexvix/Cysview Franchise: $51.02M (99.5% of total revenue).

* Regional Top-Line: Europe: $29.82M (+8% YoY); North America: $21.17M (+9% YoY).

* Gross Margin: 92.1% (vs. 94.1% in 2024).

* EBITDA: $2.76M (Burdened by $1.67M in non-recurring M&A exploratory expenses).

* Operating Cash Flow (OCF): $3.05M.

* Internal Capital Allocation: $2.86M allocated to discretionary share buybacks; $3.91M allocated to Ipsen earnout liabilities (remaining non-current liability: $9.63M).

* Balance Sheet Liquidity: Cash and short-term deposits stood at $22.99M, providing an indefinite operational runway without the need for external equity financing.

* Unit Economics & Price-Mix Analysis: The company is asserting definitive pricing power. While global in-market unit volumes grew by 5% YoY, top-line revenue expanded by 8-9% regionally. This delta explicitly highlights aggressive Average Selling Price (ASP) hikes executed across both the U.S. and European segments to combat macroeconomic inflation. R&D capital intensity remains virtually nonexistent at 0.08% of revenue, as Phase III pipeline costs (Cevira) are fully outsourced to out-licensing partner Asieris, preparing for a $13M milestone catalyst in Q1 2026 upon Chinese and European regulatory progress.

CMO Dependency & Geopolitical Node Audits

Photocure operates an extreme asset-light, 100% outsourced operational footprint. While this shields the balance sheet from manufacturing CAPEX, it introduces specialized third-party dependencies requiring rigorous mapping.

* Geographic Corporate Footprint: Management operates from the BREEAM-certified "Very Good" Global Headquarters in Oslo, Norway, alongside primary commercial hubs in Princeton, New Jersey, and Germany.

* Tier-1 CMO Network: Finished and semi-finished manufacturing is concentrated strictly within Western Europe across critical facilities in Italy, Spain, the Netherlands, and Austria.

* Sub-Tier Vulnerability & Resource Constraints: A 2025 supply chain audit mapping 22 subcontractors flagged specific medium-risk nodes. Three upstream nodes in India supply raw materials to the primary Spanish aggregator, presenting structural labor risk. Additionally, one node near Tel Aviv, Israel, introduces potential geopolitical and water-scarcity disruptions. The firm currently utilizes standard UN Global Compact adherence to manage these sub-tier ESG exposures, reporting zero compliance breaches in 2025.

* The Hardware Ecosystem (The Physical Bottleneck): The firm’s highest vulnerability is U.S. hardware compatibility. Currently, Karl Storz holds a monopoly on FDA-approved equipment for the Cysview agent. To bypass hospital hardware purchasing freezes, Photocure aggressively pivoted to an OPEX model with ForTec Medical, deploying 24 mobile BLC Saphira towers in the U.S. (driving 11% of the U.S. business). In Europe, hardware agnosticism is accelerating via 60 high-definition Visera Elite III system placements with Olympus, and a targeted 2027 global launch of next-generation 4K flexible scopes co-developed with Richard Wolf.

HDIN Institutional Perspective

While Photocure emphasizes its "asset-light" manufacturing model, the 100% reliance on third-party hardware manufacturers exposes a severe single-point-of-failure. The firm's $51.02M diagnostic consumable franchise has historically been held hostage by Karl Storz’s equipment lifecycle in the U.S. market. However, the Street is fundamentally underpricing the structural margin expansion imminent from two primary regulatory catalysts: the proposed August 2026 CMS reimbursement decoupling and the pending FDA Class II equipment downgrade scheduled for H2 2026.

We view the FDA down-classification as the definitive value driver. This regulatory arbitrage will break the Karl Storz monopoly, effectively commoditizing the hardware "razor" and accelerating high-margin "blade" consumption across alternative OEMs. Coupled with an impenetrable method-of-use patent thicket locking down exclusivity until December 2036 and January 2038, the company has transformed its economic moat from chemical composition to institutional workflow integration.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant)*:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."