Norsk Titanium: Strategic Repositioning at Plattsburgh Hub as Exaggerated Working Capital Burn Signals Critical 2026 Liquidity Juncture

Date : 2026-06-11

Reading : 166

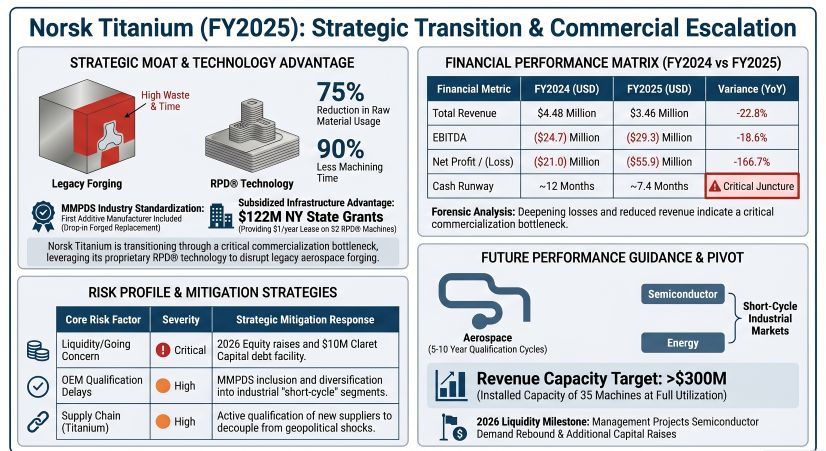

Norsk Titanium’s FY2025 $55.92 million net loss and implied 7.4-month cash runway reveal a severe operational bottleneck in converting its MMPDS-certified additive manufacturing moat into serialized cash flow. As Boeing’s internal restructuring stalls long-term aerospace qualification cycles, the company is leveraging its New York subsidized footprint to aggressively pivot toward short-cycle defense and semiconductor markets. For institutional LPs, the 50% gross inventory surge set against a 22.8% revenue contraction signals an urgent necessity for 2026 capital market intervention to prevent the materialization of explicitly stated going-concern risks.

Figure Norsk Titanium FY2025: Strategic Transition & Commercial Escalation

Forensic Financial Analysis & Margin Decomposition

Forensic Financial Analysis & Margin Decomposition

The FY2025 income statement and balance sheet of Euronext: NTI reflect severe margin compression distorted by macroeconomic turbulence and an internal failure to synchronize production output with contracted revenue realization. Operations are highly consolidated around its proprietary Rapid Plasma Deposition (RPD®) technology.

Quantitative Inventory & Margin Dynamics:

* Top-Line Contraction: Total Revenue fell 22.8% YoY to $3.46 million (FY24: $4.48 million). Total Income, inclusive of a flat $0.60 million in government grants, settled at $4.06 million (-20.0% YoY).

* Revenue Bifurcation: Income is strictly divided between Development Programs ($1.77 million / 51.1%) and the Sale of Printed Parts ($1.69 million / 48.9%). Geographically, the USA/Canada matrix dominates at 87.2% ($3.02 million), while European revenue collapsed by 76.9% to $0.44 million.

* Customer Concentration: Extreme counterparty risk remains, with three clients accounting for 63% of total revenue (34%, 19%, and 10%).

* EBITDA & Net Income Collapse: EBITDA losses widened to $(29.3) million (EBITDA margin of -846.8%). Net Profit deteriorated by 166.7% to a $(55.92) million loss, heavily distorted by $24.8 million in unrealized foreign exchange losses.

* Unit Economics & Gross Margin Proxy: Despite revenue contraction, the cost of raw materials and consumables climbed 19.3% to $8.61 million, driving the gross margin proxy to an unsustainable -148.8%.

* Liquidity & FCF Conversion: The company executed a $(31.18) million Free Cash Flow (FCF) burn, comprised of $(30.16) million in operating outflows and minimal CapEx of $(1.02) million. While the Current Ratio sits at an artificially liquid 5.40x, this is sustained exclusively by $25.12 million in external financing, including a $5 million drawdown from a $10 million Claret Capital Partners term loan.

* Asset Quality Breakdown: A forensic scan of working capital reveals a 50.0% YoY surge in Gross Inventory to $9.42 million. Concurrently, provisions for obsolete inventory spiked 7,000% to $0.636 million. Parent company intercompany loan impairments to its US subsidiary reached an accumulated NOK 1.36 billion.

Supply Chain Audit & Transatlantic Geo-Economic Moat

Norsk Titanium’s physicality is defined by an installed capacity of 700 Metric Tons/Year across 35 proprietary MERKE IV® machines, heavily weighted toward a state-subsidized North American footprint.

Facility Footprint & Geographic Capacity:

* Plattsburgh Production Center (PPC) (New York, USA): An 80,000 sq. ft. facility housing 22 RPD machines (440 MT capacity). It is currently approved for Boeing and Airbus commercial aerospace production but operating at low utilization.

* Plattsburgh Defense & Qualification Center (PDQC) (New York, USA): A 67,000 sq. ft. facility housing 10 machines (200 MT capacity), strictly dedicated to US Department of Defense systems and low-rate initial production (LRIP).

* Eggemoen Technology Center (ETC) (Norway): A 25,000 sq. ft. R&D core housing 3 machines (60 MT capacity) and a full-scale metallurgy lab.

Supply Chain Physics & Geopolitical Exposure:

The operational supply chain requires critical inputs: titanium wire, argon gas, and titanium substrates. Management has identified systemic pricing and sourcing risks tied directly to the ongoing conflict in Ukraine and US/EU sanctions against Russia and Belarus. Furthermore, US tariff uncertainties on Chinese-sourced materials present input cost escalations that Norsk Titanium cannot easily pass through to Tier-1 OEMs.

Despite upstream risks, the company’s structural moat relies on its superior physical unit economics. The RPD® process utilizes 75% less raw material, reduces machining time by 90%, slashes energy consumption by 75%, and cuts CO2 emissions by 30% compared to legacy titanium forging. This ESG-compliant efficiency was formally cemented in 2025 when the company became the first additive manufacturer to have its material properties published in the global MMPDS Handbook Vol II, legally authorizing its use by the FAA, EASA, and US DoD.

HDIN Institutional Perspective

While Norsk Titanium asserts that its $122 million utilization of New York State (FSMC) grants has functionally eliminated near-term CapEx constraints, the 50% surge in raw material and Work In Progress (WIP) inventory suggests a toxic "capital trap."

The Street is mispricing the friction of OEM testing cycles. Norsk Titanium is effectively subsidizing Airbus and Boeing qualification delays with its own fragile balance sheet, accumulating $9.42 million in inventory that is rapidly aging toward obsolescence. Furthermore, the off-balance-sheet commitment to hire 231 direct employees in New York by 2029 to maintain its $1-per-year facility lease enforces a rigid operational expenditure floor. The newly appointed CEO's (Fabrizio Ponte) strategy to pivot toward short-cycle semiconductor and industrial markets targeting a 2026 demand rebound is strategically sound; however, we assess that the current $19.25 million cash reserve cannot bridge the gap. Institutional investors must price in highly dilutive equity raises or debt restructurings prior to the expiration of the Claret Capital interest-only period in December 2026.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Norsk Titanium FY2025: Strategic Transition & Commercial Escalation

Forensic Financial Analysis & Margin DecompositionThe FY2025 income statement and balance sheet of Euronext: NTI reflect severe margin compression distorted by macroeconomic turbulence and an internal failure to synchronize production output with contracted revenue realization. Operations are highly consolidated around its proprietary Rapid Plasma Deposition (RPD®) technology.

Quantitative Inventory & Margin Dynamics:

* Top-Line Contraction: Total Revenue fell 22.8% YoY to $3.46 million (FY24: $4.48 million). Total Income, inclusive of a flat $0.60 million in government grants, settled at $4.06 million (-20.0% YoY).

* Revenue Bifurcation: Income is strictly divided between Development Programs ($1.77 million / 51.1%) and the Sale of Printed Parts ($1.69 million / 48.9%). Geographically, the USA/Canada matrix dominates at 87.2% ($3.02 million), while European revenue collapsed by 76.9% to $0.44 million.

* Customer Concentration: Extreme counterparty risk remains, with three clients accounting for 63% of total revenue (34%, 19%, and 10%).

* EBITDA & Net Income Collapse: EBITDA losses widened to $(29.3) million (EBITDA margin of -846.8%). Net Profit deteriorated by 166.7% to a $(55.92) million loss, heavily distorted by $24.8 million in unrealized foreign exchange losses.

* Unit Economics & Gross Margin Proxy: Despite revenue contraction, the cost of raw materials and consumables climbed 19.3% to $8.61 million, driving the gross margin proxy to an unsustainable -148.8%.

* Liquidity & FCF Conversion: The company executed a $(31.18) million Free Cash Flow (FCF) burn, comprised of $(30.16) million in operating outflows and minimal CapEx of $(1.02) million. While the Current Ratio sits at an artificially liquid 5.40x, this is sustained exclusively by $25.12 million in external financing, including a $5 million drawdown from a $10 million Claret Capital Partners term loan.

* Asset Quality Breakdown: A forensic scan of working capital reveals a 50.0% YoY surge in Gross Inventory to $9.42 million. Concurrently, provisions for obsolete inventory spiked 7,000% to $0.636 million. Parent company intercompany loan impairments to its US subsidiary reached an accumulated NOK 1.36 billion.

Supply Chain Audit & Transatlantic Geo-Economic Moat

Norsk Titanium’s physicality is defined by an installed capacity of 700 Metric Tons/Year across 35 proprietary MERKE IV® machines, heavily weighted toward a state-subsidized North American footprint.

Facility Footprint & Geographic Capacity:

* Plattsburgh Production Center (PPC) (New York, USA): An 80,000 sq. ft. facility housing 22 RPD machines (440 MT capacity). It is currently approved for Boeing and Airbus commercial aerospace production but operating at low utilization.

* Plattsburgh Defense & Qualification Center (PDQC) (New York, USA): A 67,000 sq. ft. facility housing 10 machines (200 MT capacity), strictly dedicated to US Department of Defense systems and low-rate initial production (LRIP).

* Eggemoen Technology Center (ETC) (Norway): A 25,000 sq. ft. R&D core housing 3 machines (60 MT capacity) and a full-scale metallurgy lab.

Supply Chain Physics & Geopolitical Exposure:

The operational supply chain requires critical inputs: titanium wire, argon gas, and titanium substrates. Management has identified systemic pricing and sourcing risks tied directly to the ongoing conflict in Ukraine and US/EU sanctions against Russia and Belarus. Furthermore, US tariff uncertainties on Chinese-sourced materials present input cost escalations that Norsk Titanium cannot easily pass through to Tier-1 OEMs.

Despite upstream risks, the company’s structural moat relies on its superior physical unit economics. The RPD® process utilizes 75% less raw material, reduces machining time by 90%, slashes energy consumption by 75%, and cuts CO2 emissions by 30% compared to legacy titanium forging. This ESG-compliant efficiency was formally cemented in 2025 when the company became the first additive manufacturer to have its material properties published in the global MMPDS Handbook Vol II, legally authorizing its use by the FAA, EASA, and US DoD.

HDIN Institutional Perspective

While Norsk Titanium asserts that its $122 million utilization of New York State (FSMC) grants has functionally eliminated near-term CapEx constraints, the 50% surge in raw material and Work In Progress (WIP) inventory suggests a toxic "capital trap."

The Street is mispricing the friction of OEM testing cycles. Norsk Titanium is effectively subsidizing Airbus and Boeing qualification delays with its own fragile balance sheet, accumulating $9.42 million in inventory that is rapidly aging toward obsolescence. Furthermore, the off-balance-sheet commitment to hire 231 direct employees in New York by 2029 to maintain its $1-per-year facility lease enforces a rigid operational expenditure floor. The newly appointed CEO's (Fabrizio Ponte) strategy to pivot toward short-cycle semiconductor and industrial markets targeting a 2026 demand rebound is strategically sound; however, we assess that the current $19.25 million cash reserve cannot bridge the gap. Institutional investors must price in highly dilutive equity raises or debt restructurings prior to the expiration of the Claret Capital interest-only period in December 2026.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."