Aethlon Medical: Going Concern Designation Near San Diego Headquarters as $7.0M Capital Burn Signals Imminent Australian Clinical Dilution

Date : 2026-06-12

Reading : 97

Aethlon Medical faces an acute liquidity crisis, underscored by a formal "Going Concern" warning and a FY2026 operational cash burn of $7.0 million against just $5.02 million in year-end reserves. For institutional LPs, the structural misalignment is glaring: FY2025 administrative overhead outpaced core R&D expenditure by a 3.2x multiplier. Tethered entirely to sluggish Australian oncology trials and plagued by sole-source supply bottlenecks—specifically pending FDA approval for a secondary GNA lectin vendor—the firm's survival hinges on highly dilutive toxic warrant issuances rather than organic clinical momentum.

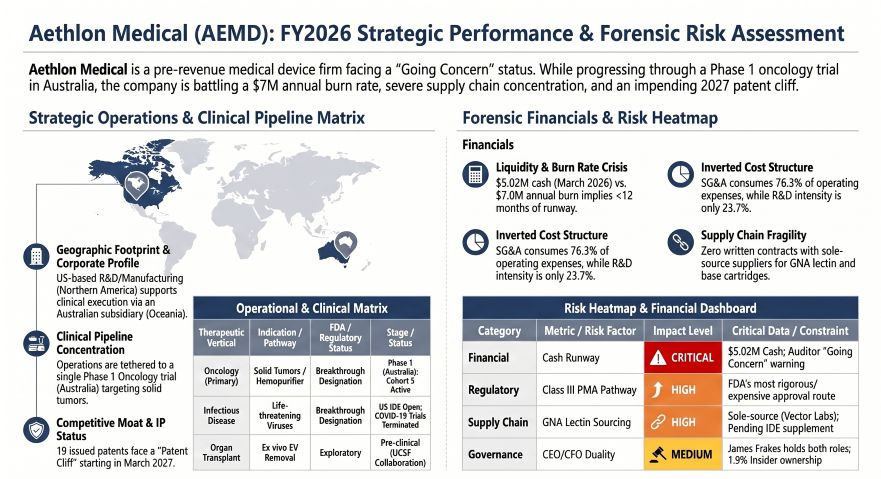

Figure Aethlon Medical (AEMD) FY2026: Strategic Performance & Forensic Risk Assessment

Forensic Financials & Internal Capital Misallocation

Forensic Financials & Internal Capital Misallocation

A forensic analysis of NASDAQ: AEMD reveals an inverted operational cost structure heavily skewed toward administrative bloat and executive severance rather than pipeline advancement. With exactly $0 in commercial revenue generated across FY2025 and FY2026, the company relies entirely on "toxic" capital market extraction to fund operations.

* Liquidity & Cash Burn: FY2026 concluded with $5.02 million in cash and cash equivalents, yielding an implied runway of less than 12 months based on a historical $7.0 million annual burn rate. Post-FY2026 At-The-Market (ATM) net proceeds of $1.85 million in June 2026 provide minimal bridging capital.

* Inverted Operating Leverage: In FY2025, total operating expenses registered at $9.34 million. Genuine R&D accounted for merely $2.21 million (23.7%), artificially subsidized by a $218,000 Australian R&D Tax Incentive in FY2026. Conversely, SG&A consumed $7.13 million (76.3%), a 3.2x multiplier over scientific investment.

* Executive Compensation vs. Shareholder Value: Despite overseeing a 99% destruction of shareholder equity ($100 invested in March 2023 collapsed to $0.72 by March 2026), CEO/CFO James Frakes received $826,922 in total compensation for FY2026. Concurrently, $346,286 in cash severance and COBRA was deployed for terminated C-suite executives, draining critical clinical liquidity. Total insider ownership sits at a negligible 1.9% (29,652 shares).

* Non-Cash Anomalies & Dilutive Mechanisms: The FY2025 net loss of $(13.39) million was severely distorted by a $4.61 million non-cash "Warrant Inducement Expense." To secure $2.31 million in gross proceeds in March 2025, the firm repriced existing warrants to $0.3736 and issued 200% warrant coverage. A subsequent December 2025 PIPE with 5% stakeholder Armistice Capital repriced warrants to $4.03.

* Stranded Tax Assets: Aethlon holds $101 million in federal Net Operating Losses (NOLs). However, persistent toxic warrant inducements perpetually risk triggering IRC Section 382 ownership changes, fundamentally impairing the utilization of these historical tax attributes. A 100% valuation allowance is applied against $36.65 million in gross deferred tax assets.

Supply Chain Audit & San Diego cGMP Dependency

Aethlon’s operational physicality is geographically bifurcated: U.S.-based manufacturing/R&D and Australian clinical execution. The supply chain exhibits severe upstream concentration risk, functioning without formal minimum purchase commitments or supply guarantees.

* Manufacturing Centralization: In May 2024, the FDA approved an Investigational Device Exemption (IDE) supplement, allowing Aethlon to migrate from outsourced California production to in-house cGMP manufacturing at its 2,655 square-foot San Diego headquarters.

* Sole-Source Raw Material Bottleneck: The core proprietary asset, the Hemopurifier, is critically dependent on three exclusive vendors: Medica S.p.A. (base cartridges), Vector Laboratories Inc. (GNA lectin), and Imerys Minerals Ltd. / Janus Scientific Inc. (diatomaceous earth). Aethlon is currently experiencing a critical operational delay while awaiting FDA IDE supplement approval to qualify a secondary GNA lectin supplier.

* Geographic Execution Risk: After strategically abandoning an approved oncology trial at India's Medanta Medicity Hospital, clinical bandwidth is entirely concentrated in Australia across three sites: Royal Adelaide Hospital, Pindara Private Hospital, and GenesisCare North Shore Hospital. As of June 4, 2026, only the first participant of Cohort 3 had received treatment, indicating sluggish patient acquisition.

HDIN Institutional Perspective

While Aethlon aggressively markets its dual FDA "Breakthrough Device" designations as a procedural moat, our independent assessment indicates this status offers zero commercial insulation. The authentic narrative is defined by an impending March 2027 patent cliff clashing directly against the longest, most capital-intensive regulatory pathway in medical devices: the Class III Pre-Market Approval (PMA).

Furthermore, the consolidation of the CEO and CFO roles into a single individual (James B. Frakes)—while simultaneously operating under a formal Going Concern warning—violates baseline governance standards regarding segregation of duties. The complete absence of minimum supply guarantees with critical vendors like Vector Laboratories leaves the firm precisely one logistical delay away from an unmitigated clinical halt. The market has fundamentally mispriced the execution risk here; the clinical timeline mathematically eclipses the remaining cash runway, ensuring subsequent rounds of highly dilutive, punitive financing before any actionable Phase 2 data can materialize.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Aethlon Medical (AEMD) FY2026: Strategic Performance & Forensic Risk Assessment

Forensic Financials & Internal Capital MisallocationA forensic analysis of NASDAQ: AEMD reveals an inverted operational cost structure heavily skewed toward administrative bloat and executive severance rather than pipeline advancement. With exactly $0 in commercial revenue generated across FY2025 and FY2026, the company relies entirely on "toxic" capital market extraction to fund operations.

* Liquidity & Cash Burn: FY2026 concluded with $5.02 million in cash and cash equivalents, yielding an implied runway of less than 12 months based on a historical $7.0 million annual burn rate. Post-FY2026 At-The-Market (ATM) net proceeds of $1.85 million in June 2026 provide minimal bridging capital.

* Inverted Operating Leverage: In FY2025, total operating expenses registered at $9.34 million. Genuine R&D accounted for merely $2.21 million (23.7%), artificially subsidized by a $218,000 Australian R&D Tax Incentive in FY2026. Conversely, SG&A consumed $7.13 million (76.3%), a 3.2x multiplier over scientific investment.

* Executive Compensation vs. Shareholder Value: Despite overseeing a 99% destruction of shareholder equity ($100 invested in March 2023 collapsed to $0.72 by March 2026), CEO/CFO James Frakes received $826,922 in total compensation for FY2026. Concurrently, $346,286 in cash severance and COBRA was deployed for terminated C-suite executives, draining critical clinical liquidity. Total insider ownership sits at a negligible 1.9% (29,652 shares).

* Non-Cash Anomalies & Dilutive Mechanisms: The FY2025 net loss of $(13.39) million was severely distorted by a $4.61 million non-cash "Warrant Inducement Expense." To secure $2.31 million in gross proceeds in March 2025, the firm repriced existing warrants to $0.3736 and issued 200% warrant coverage. A subsequent December 2025 PIPE with 5% stakeholder Armistice Capital repriced warrants to $4.03.

* Stranded Tax Assets: Aethlon holds $101 million in federal Net Operating Losses (NOLs). However, persistent toxic warrant inducements perpetually risk triggering IRC Section 382 ownership changes, fundamentally impairing the utilization of these historical tax attributes. A 100% valuation allowance is applied against $36.65 million in gross deferred tax assets.

Supply Chain Audit & San Diego cGMP Dependency

Aethlon’s operational physicality is geographically bifurcated: U.S.-based manufacturing/R&D and Australian clinical execution. The supply chain exhibits severe upstream concentration risk, functioning without formal minimum purchase commitments or supply guarantees.

* Manufacturing Centralization: In May 2024, the FDA approved an Investigational Device Exemption (IDE) supplement, allowing Aethlon to migrate from outsourced California production to in-house cGMP manufacturing at its 2,655 square-foot San Diego headquarters.

* Sole-Source Raw Material Bottleneck: The core proprietary asset, the Hemopurifier, is critically dependent on three exclusive vendors: Medica S.p.A. (base cartridges), Vector Laboratories Inc. (GNA lectin), and Imerys Minerals Ltd. / Janus Scientific Inc. (diatomaceous earth). Aethlon is currently experiencing a critical operational delay while awaiting FDA IDE supplement approval to qualify a secondary GNA lectin supplier.

* Geographic Execution Risk: After strategically abandoning an approved oncology trial at India's Medanta Medicity Hospital, clinical bandwidth is entirely concentrated in Australia across three sites: Royal Adelaide Hospital, Pindara Private Hospital, and GenesisCare North Shore Hospital. As of June 4, 2026, only the first participant of Cohort 3 had received treatment, indicating sluggish patient acquisition.

HDIN Institutional Perspective

While Aethlon aggressively markets its dual FDA "Breakthrough Device" designations as a procedural moat, our independent assessment indicates this status offers zero commercial insulation. The authentic narrative is defined by an impending March 2027 patent cliff clashing directly against the longest, most capital-intensive regulatory pathway in medical devices: the Class III Pre-Market Approval (PMA).

Furthermore, the consolidation of the CEO and CFO roles into a single individual (James B. Frakes)—while simultaneously operating under a formal Going Concern warning—violates baseline governance standards regarding segregation of duties. The complete absence of minimum supply guarantees with critical vendors like Vector Laboratories leaves the firm precisely one logistical delay away from an unmitigated clinical halt. The market has fundamentally mispriced the execution risk here; the clinical timeline mathematically eclipses the remaining cash runway, ensuring subsequent rounds of highly dilutive, punitive financing before any actionable Phase 2 data can materialize.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."