PCC SE: Downstream Pivot Near Płock and Brzeg Dolny as -$224.7M Net Loss Signals Systemic Base Chemical Rejection

Date : 2026-06-13

Reading : 159

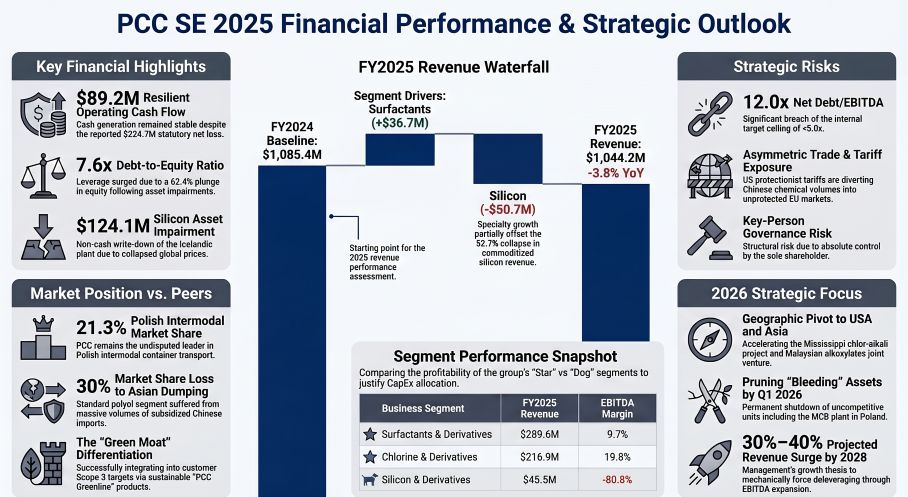

PCC SE’s FY2025 results expose a critical dichotomy in European manufacturing. While aggressive US tariffs diverted Chinese dumping into the EU, forcing a $124.1 million write-down of PCC’s Icelandic silicon facility and collapsing net income to -$224.7 million, operating cash flow remained incredibly resilient at $89.2 million. For institutional debt holders, the narrative is clear: the company is aggressively abandoning commoditized base chemicals. Capital allocation is pivoting toward high-margin, defensive surfactants in Poland and Mississippi, signaling a forced geographic and downstream retreat from Europe’s structurally uncompetitive industrial landscape.

Figure PCC SE 2025 Financial Performance & Strategic Outlook

Forensic Financials & Operational Leverage Dislocation

Forensic Financials & Operational Leverage Dislocation

Beyond the headline net loss, a forensic analysis of the FY2025 income statement reveals an aggressive internal restructuring. Top-line revenue eroded 3.8% to $1,044.2 million, but cash generation was insulated by a $24.3 million working capital release (inventory destocking tied to idling the Iceland plant) and a hard pivot toward specialty segments. Return on Capital Employed (ROCE) collapsed to -9.6% driven by $225.8 million in total D&A, but segmental unit economics paint a highly polarized picture of pricing power:

* Surfactants & Derivatives (The Star): Revenue surged 14.5% to $289.6 million. Maintained a 9.7% EBITDA margin ($27.9 million). Pricing power is heavily insulated by direct B2B integration into recession-proof cosmetics and detergents, leveraging PCC Greenline® formulations.

* Chlorine & Derivatives (The Cash Cow): Revenue fell 8.5% to $216.9 million, yet delivered a dominant 19.8% EBITDA margin ($43.0 million). Profitability was defended by the installation of two new flexible electrolyzers in Brzeg Dolny, executing intra-day electricity spot price arbitrage.

* Logistics (The Physical Moat): Revenue grew 2.0% to $178.3 million with a 15.3% EBITDA margin. Secured a 21.3% market share in Polish intermodal transport, isolated from Asian export dumping.

* Silicon & Derivatives (The Bleeding Core): Revenue imploded 52.7% to $45.5 million. EBITDA margin cratered to -80.8% (-$36.7 million), triggering the $124.1 million impairment of the Icelandic facility.

* Capital Structure Deterioration: FY2025 CapEx accelerated 37.4% to $196.5 million, entirely debt-funded. Consequently, Net Debt surged 13.9% to $1,107.3 million, driving the Net Debt/EBITDA ratio to a distressed 12.0x (violating the <5.0x internal target and breaching two external credit covenants). Equity was decimated to $145.7 million, pushing the Debt-to-Equity ratio to ~7.6x.

The Brzeg Dolny Ecosystem & Intermodal Moat

PCC SE is actively re-engineering its physical footprint to mitigate severe geopolitical vulnerabilities—specifically the March 2026 Iran war escalation and localized Polish-Ukrainian border chaos. The company’s survival relies on heavy backward integration and subsidized hard assets.

* European Defensive Infrastructure: The Brzeg Dolny chemical park operates as a closed-loop ecosystem, utilizing captive combined heat and power (CHP) to shield against grid volatility. Downstream, the newly commissioned 35,000–40,000-ton ethoxylates plant in Płock immediately captured market share. To bypass European freight bottlenecks, the company is deploying $79.1 million (subsidized ~50% by the EU) into a 5th intermodal terminal in Ropczyce, Podkarpackie, set to begin construction in 2026.

* Transatlantic & Asian Flight: To escape the European commodity trap, capital is migrating. The company ramped up a 70,000-ton alkoxylates joint venture in Kuala Lumpur, Malaysia, and is pushing a greenfield chlor-alkali facility in Mississippi, USA (though the Final Investment Decision remains delayed past Q4 2025 due to FEED contractor bottlenecks).

* Geopolitical Supply Chain Friction: The company maintains a high-risk $12.89 million loan (at 10.0% interest) to its Russian Joint Venture, OOO DME Aerosol. Conversely, it insulates its sustainable ESG moat by sourcing RSPO-certified palm kernel oil from ~300 isolated smallholder farmers in Ghana.

HDIN Institutional Perspective

While management claims the massive $196.5 million CapEx deployment will mechanically repair the distressed 12.0x Net Debt/EBITDA ratio via a projected 30%-40% revenue surge by 2027/2028, we view this as a perilous "Bond Trap." The company is attempting to outgrow a severely over-leveraged capital structure. With equity essentially wiped out by the Iceland and MCB plant impairments, and absolute debt mathematically programmed to rise through 2028, PCC SE is entirely reliant on the German mid-cap retail bond market holding steady. Furthermore, the total lack of KPI-driven variable compensation for the sole shareholder/Chairman creates a principal-principal dynamic: management will ruthlessly pursue long-term asset transformation (like the Q1 2027 Brzeg Dolny alkoxylates launch and PCC Thorion GmbH battery materials) without regard for short-term covenant optics. The strategic pivot is flawless; the liquidity runway to execute it is razor-thin.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure PCC SE 2025 Financial Performance & Strategic Outlook

Forensic Financials & Operational Leverage DislocationBeyond the headline net loss, a forensic analysis of the FY2025 income statement reveals an aggressive internal restructuring. Top-line revenue eroded 3.8% to $1,044.2 million, but cash generation was insulated by a $24.3 million working capital release (inventory destocking tied to idling the Iceland plant) and a hard pivot toward specialty segments. Return on Capital Employed (ROCE) collapsed to -9.6% driven by $225.8 million in total D&A, but segmental unit economics paint a highly polarized picture of pricing power:

* Surfactants & Derivatives (The Star): Revenue surged 14.5% to $289.6 million. Maintained a 9.7% EBITDA margin ($27.9 million). Pricing power is heavily insulated by direct B2B integration into recession-proof cosmetics and detergents, leveraging PCC Greenline® formulations.

* Chlorine & Derivatives (The Cash Cow): Revenue fell 8.5% to $216.9 million, yet delivered a dominant 19.8% EBITDA margin ($43.0 million). Profitability was defended by the installation of two new flexible electrolyzers in Brzeg Dolny, executing intra-day electricity spot price arbitrage.

* Logistics (The Physical Moat): Revenue grew 2.0% to $178.3 million with a 15.3% EBITDA margin. Secured a 21.3% market share in Polish intermodal transport, isolated from Asian export dumping.

* Silicon & Derivatives (The Bleeding Core): Revenue imploded 52.7% to $45.5 million. EBITDA margin cratered to -80.8% (-$36.7 million), triggering the $124.1 million impairment of the Icelandic facility.

* Capital Structure Deterioration: FY2025 CapEx accelerated 37.4% to $196.5 million, entirely debt-funded. Consequently, Net Debt surged 13.9% to $1,107.3 million, driving the Net Debt/EBITDA ratio to a distressed 12.0x (violating the <5.0x internal target and breaching two external credit covenants). Equity was decimated to $145.7 million, pushing the Debt-to-Equity ratio to ~7.6x.

The Brzeg Dolny Ecosystem & Intermodal Moat

PCC SE is actively re-engineering its physical footprint to mitigate severe geopolitical vulnerabilities—specifically the March 2026 Iran war escalation and localized Polish-Ukrainian border chaos. The company’s survival relies on heavy backward integration and subsidized hard assets.

* European Defensive Infrastructure: The Brzeg Dolny chemical park operates as a closed-loop ecosystem, utilizing captive combined heat and power (CHP) to shield against grid volatility. Downstream, the newly commissioned 35,000–40,000-ton ethoxylates plant in Płock immediately captured market share. To bypass European freight bottlenecks, the company is deploying $79.1 million (subsidized ~50% by the EU) into a 5th intermodal terminal in Ropczyce, Podkarpackie, set to begin construction in 2026.

* Transatlantic & Asian Flight: To escape the European commodity trap, capital is migrating. The company ramped up a 70,000-ton alkoxylates joint venture in Kuala Lumpur, Malaysia, and is pushing a greenfield chlor-alkali facility in Mississippi, USA (though the Final Investment Decision remains delayed past Q4 2025 due to FEED contractor bottlenecks).

* Geopolitical Supply Chain Friction: The company maintains a high-risk $12.89 million loan (at 10.0% interest) to its Russian Joint Venture, OOO DME Aerosol. Conversely, it insulates its sustainable ESG moat by sourcing RSPO-certified palm kernel oil from ~300 isolated smallholder farmers in Ghana.

HDIN Institutional Perspective

While management claims the massive $196.5 million CapEx deployment will mechanically repair the distressed 12.0x Net Debt/EBITDA ratio via a projected 30%-40% revenue surge by 2027/2028, we view this as a perilous "Bond Trap." The company is attempting to outgrow a severely over-leveraged capital structure. With equity essentially wiped out by the Iceland and MCB plant impairments, and absolute debt mathematically programmed to rise through 2028, PCC SE is entirely reliant on the German mid-cap retail bond market holding steady. Furthermore, the total lack of KPI-driven variable compensation for the sole shareholder/Chairman creates a principal-principal dynamic: management will ruthlessly pursue long-term asset transformation (like the Q1 2027 Brzeg Dolny alkoxylates launch and PCC Thorion GmbH battery materials) without regard for short-term covenant optics. The strategic pivot is flawless; the liquidity runway to execute it is razor-thin.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."